Of the five trends described in a report published by Kalorama, only two made the list for both years: Consolidation within the IVD industry and growth in molecular point of care

What a difference one year can make in the most significant trends influencing the in vitro diagnostics (IVD) industry, which also influences clinical laboratories, the largest customers of IVD manufacturers. These insights come from comparing the top five IVD trends for 2016 as identified by Kalorama Information from its top five IVD trends that it says dominated during 2015.

Kalorama is a division of MarketResearch.com, a company that publishes market research in the life sciences. In a report titled, “Five IVD Market Trends to Watch for in 2016,” it published its picks for the top five trends in IVD testing for 2016. The five most prominent trends recognized by the healthcare research marketer are as follows:

1. Expect More Acquisitions from Heavyweights: Kalorama’s experts point out that the increasing complexity of in vitro diagnostics is one powerful force encouraging IVD companies to do acquisitions, partnership deals, and distributor agreements as a way to bring together all the technology parts they need to compete. Expect to see plenty more of these types of deals in 2016 as companies scramble to obtain all the technology and resources needed to achieve their goals.

2. Pragmatic Personalized Medicine: Pharmacogenomics (PGx) studies how an individual’s genetic makeup affects how they react to certain medications. Kalorama notes that there are currently more than 50 PGx test products in development or already on the market. Tests for infectious and hereditary diseases should continue to improve, as well as further advancements in oncology. Government projects from 2015, such as the Precision Medicine Initiative Cohort Program should also improve the dynamics of PGx testing.

3. The Service Industry Is Here to Stay: “The test service model has become a major route for highly sophisticated and specialized molecular tests,” wrote the authors of the Kalorama report. “At one time, the most successful molecular test services offered cancer diagnostics using in situ hybridization (ISH), sequencing and polymerase chain reaction (PCR) analysis of biopsied tissue.” The authors went on to say, “The service model for molecular tests has been adopted by private reference labs, large hospitals and company-owned test services. The company-owned test service business model is primarily a phenomenon of the U.S. There is a long history for the commercialization of highly specific assays as test services.”

4. Emerging Disease Threats: International travel, trade, and climate changes are contributing factors in the emergence of diseases in developed countries that were typically found only in the tropics or the developing world. The recent Ebola risk made the American public more aware of a pandemic disease threat. Infectious diseases like malaria, Chagas Disease, and Dengue Fever can now appear anywhere on the planet, infecting humans, animals, and insects. These types of diseases can be difficult to prevent and control, making their existence a public health concern for the world’s population.

5. Near-Patient Molecular: Kalorama predicts that, in 2016 and beyond, development of products in point-of-care (POC) molecular diagnostics will be swift and continuous. Such POC and near-patient molecular test products, particularly for infectious disease, “allow providers to initiate care during the same visit or day,” noted Kalorama in its story. “These announcements build on previous developments in near-patient molecular last year.”

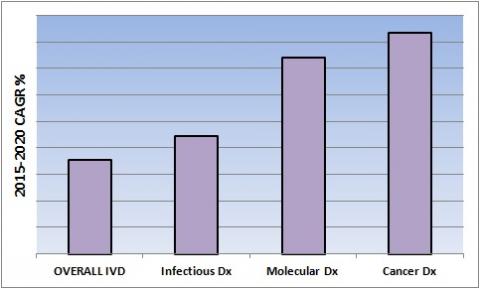

In their report titled “Five IVD Market Trends to Watch for in 2016,” Kalorama Information’s authors use the chart (above) to illustrate the relative growth rates of different sectors of the in vitro diagnostics (IVD) marketplace, as measured by compound annual growth rates (CAGR). Slowest annual growth is in the overall IVD marketplace, while the sectors of infectious disease, molecular diagnostics, and cancer diagnostics are posting substantially greater annual rates of growth. Collectively, these three IVD areas represent approximately 40% of the overall IVD market. (Photo copyright: Kalorama Information.)

In December, 2015, Kalorama Information issued a press release that offered a look-back at its pick for the top five IVD trends for 2015. These trends were:

1. Molecular POC Becomes Reality: Multiple companies, including Alere and Cepheid, have recently introduced analytical instruments that can perform rapid molecular analysis in near-patient settings. Products that advance infectious disease testing into the point-of-care (POC) arena, allow healthcare providers to begin essential treatment during the same visit or day. For example, the Alere i Influenza A & B platform delivers molecular flu results in less than 15 minutes. And, at a mere nine inches tall, Cepheid’s GeneXpert Omni, is the world’s most portable diagnostic system. It provides unprecedented access to accurate and fast diagnosis of tuberculosis, HIV, and Ebola.

2. Cancer, Molecular, and Infectious Disease Drive Sales: The research firm identified “the fastest-growing and most critical areas of clinical diagnostics: cancer diagnostics, molecular assays and systems, and infectious disease tests. Together, these three IVD areas represent approximately 40% of the overall IVD market.” Authors of the report noted that, combined, these IVD segments are outgrowing the overall IVD market by more a compound annual growth rate of 2%. The sub-segments of the cancer and molecular diagnostics markets are doing even better, growing at more than 8% each year.

3. Energetic Competitive Activity: In 2015, there was plenty of activity in the IVD market, including acquisitions, partnership deals, and distribution agreements. Roche Diagnostics, the diagnostic division of Hoffmann-La Roche, remains the world’s largest supplier of clinical diagnostics with sales almost doubling their nearest competitor. Netherlands-based Qiagen (NASDAQ:QGEN), a global provider of sample to insight solutions, has experienced close to a 30% increase in sales since 2010. IVD companies continue to experience robust growth as the larger companies jockey to increase their market share and expand their company’s offerings of IVD products.

4. Liquid Biopsy: Numerous liquid biopsy tests and enterprises progressed in 2015. This reflected the extremely high interest by IVD firms and biotech researchers to develop a way to identify circulating tumor cells (CTCs) in blood, and in using those results for early diagnosis of cancer. Genomic DNA amplified or sequenced from CTCs, circulating tumor cell DNA (cDNA), and circulating cell-free DNA (CFDNA) hold key information relevant for the treatment of cancer patients. This area of technology has some ambiguity, which the report authors characterized “having its ups and downs,” but it is emerging as one of the most “promising and exciting areas of medicine and has already made a huge impact on prenatal care.”

5. Information Technology and Genomics: Data sharing has become a vital and important tool that enables the medical research community to aggregate their knowledge on diseases and actionable findings. With hundreds of genome studies underway, information technology (IT) helps researchers share data to better understand the role of specific gene variants in disease processes. Large databases of lab test results, gene sequencing data, and other types of healthcare statistics are amalgamated to identify useful information that can lead to timely and more accurate diagnoses along with more informed therapeutic decisions.

New IVD Capabilities Will Benefit Clinical Laboratories

Over many years, Kalorama Information has kept a close eye on the in vitro diagnostics industry, so its selection of the top five IVD trends each year is based on credible research and analysis. A comparison of the research company’s choices for the top five IVD trends in 2015 and for 2016 shows how rapidly molecular and genetic technology is developing. Only the trends of ongoing IVD industry consolidation and molecular POC made the list for both 2015 and 2016.

—JP Schlingman

Related Information:

Five IVD Market Trends to Watch for in 2016

3 IVD Trends to Keep an Eye On In 2015

Kalorama Announces Top Five IVD Trends of 2015