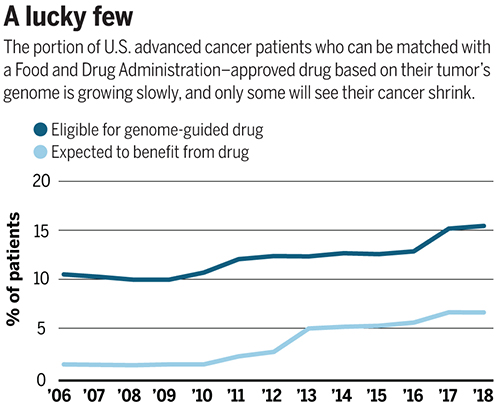

Number of patients eligible for genome-driven oncology therapy is increasing, but the percentage who reportedly benefit from the therapy remains at less than 5%

Advances in precision medicine in oncology (precision oncology) are fueling the need for clinical laboratory companion diagnostic tests that help physicians choose the best treatment protocols. In fact, this is a fast-growing area of clinical diagnostics for the nation’s anatomic pathologists. However, some experts in the field of genome-based cancer treatments disagree over whether such treatments offer more hype than hope.

Prasad and his colleagues evaluated 31 US Food and Drug

Administration (FDA) approved drugs, which were “genome-targeted” or

“genome-informed” for 38 indications between 2006 and 2018. The researchers

sought to answer the question, “How many US patients with cancer are eligible

for and benefit annually from genome-targeted therapies approved by the US Food

and Drug Administration?”

They found that in 2018 only 8.33% of 609,640 patients with

metastatic cancer were eligible for genome-targeted therapy—though this was an

increase from 5.09% in 2006.

Even more telling from Prasad’s view, his research team concluded

that only 4.9% had benefited from such treatments. Prasad’s study found the

percentage of patients estimated to have benefited from genome-informed therapy

rose from 1.3% in 2006 to 6.62% in 2018.

“Although the number of patients eligible for genome-driven treatment has increased over time, these drugs have helped a minority of patients with advanced cancer,” the researchers concluded. “To accelerate progress in precision oncology, novel trial designs of genomic therapies should be developed, and broad portfolios of drug development, including immunotherapeutic and cytotoxic approaches, should be pursued.”

The graph above is based on data from a study published in Science titled, “Estimation of the Percentage of US Patients With Cancer Who Benefit from Genome-Driven Oncology,” co-authored by Vinay Prasad, MD, MPH, et al. (Image copyright: Science.)

A Value versus Volume Argument?

Hyman, who leads a team of oncologists that conduct dozens

of clinical trials and molecularly selected “basket studies” each year,

countered Prasad’s assertions by noting the increase in the number of patients

who qualify for precision oncology treatments.

As reported in Science, Hyman said during his AACR

presentation that Sloan Kettering matched 15% of the 25,000 patients’ tumors it

tested with FDA-approved drugs and 10% with drugs in clinical trials.

“I think this is certainly not hype,” he said during the

conference.

Hyman added that another 10% to 15% of patient tumors have a

DNA change that matches a potential drug tested in animals. He expects “basket”

trials to further increase the patient pool by identifying drugs that can work

for multiple tumor types.

The US National Institute of Health (NIH) describes “basket studies” as “a new sort of clinical studies to identify patients with the same kind of mutations and treat them with the same drug, irrespective of their specific cancer type. In basket studies, depending on the mutation types, patients are classified into ‘baskets.’ Targeted therapies that block that mutation are then identified and assigned to baskets where patients are treated accordingly.”

Are Expectations of Precision Medicine Exaggerated?

A profile in MIT Technology Review, titled, “The Skeptic: What Precision Medicine Revolution?,” describes Prasad’s reputation as a “professional scold” noting the 36-year-old professor’s “sharp critiques of contemporary biomedical research, including personalized medicine.” Nevertheless, Prasad is not alone in arguing that precision oncology’s promise is often exaggerated.

“Like most ‘moonshot’ medical research initiatives,

precision medicine is likely to fall short of expectations,” Joyner wrote.

“Medical problems and their underlying biology are not linear engineering

exercises and solving them is more than a matter of vision, money, and will.”

“Although some niche applications have been found for

precision medicine—and gene therapy is now becoming a reality for a few rare

diseases—the effects on public health are miniscule while the costs are astronomical,”

they wrote.

Hope for Precision Medicine Remains High

However, optimism over precision oncology among some industry leaders has not waned. Cindy Perettie, CEO of molecular information company Foundation Medicine of Cambridge, Mass., argues genome-directed treatments have reached an “inflection point.”

“Personalized cancer treatment is a possibility for more patients than ever thanks to the advent of targeted therapies,” she told Genetic Engineering and Biotechnology News. “With a growing number of new treatments—including two pan-tumor approvals—the need for broad molecular diagnostic tools to match patients with these therapies has never been greater. We continue to advance our understanding of cancer as a disease of the genome—one in which treatment decisions can be informed by insight into the genomic changes that contribute to each patient’s unique cancer.”

Prasad acknowledges genome-driven therapies are beneficial for some cancers. However, he told MIT Technology Review the data doesn’t support the “rhetoric that we’re reaching exponential growth, or that is taking off, or there’s an inflection point” signaling rapid new advancements.

“Right now, we are investing heavily in immunotherapy and heavily in genomic therapy, but in other categories of drugs, such as cytotoxic drugs, we have stopped investigating in them,” he told Medscape Medical News. “But it’s foolish to do this—we need to have the vision to look beyond the fads we live by in cancer medicine and do things in a broader way,” he added.

“So, I support broader funding because you have to sustain

efforts even when things are not in vogue if you want to make progress,” Prasad

concluded.

Is precision oncology a fad? Dark Daily has covered the advancements in precision medicine extensively over the past decade, and with the launch of our new Precision Medicine Institute website, we plan to continue reporting on further advancements in personalized medicine.

Time will tell if precision oncology can fulfill its

promise. If it does, anatomic pathologists will play an important role in

pinpointing patients most likely to benefit from genome-driven treatments.

One thing that the debate between proponents of precision

medicine in oncology and their critics makes clear is that more and better

clinical studies are needed to document the true effectiveness of target

therapies for oncology patients. Such evidence will only reinforce the

essential role that anatomic pathologists play in diagnosis, guiding

therapeutic decisions, and monitoring the progress of cancer patients.

Combining consumers’ health data, including clinical laboratory test results, to genetic data for predispositions to chronic diseases could be key to developing targeted drugs and precision medicine treatments

Genetic testing company 23andMe is beta testing a method for combining customers’ private health data—including clinical laboratory test results and prescription drug usage—with their genetic data to create the largest database of its kind.

Such information—stored securely but accessible to 23andMe for sale to pharmaceutical companies for drug research and to diagnostics developers—would place 23andMe in a market position even Apple Health cannot claim.

Additionally, given the importance of clinical lab test data—which makes up more than 70% of a patient’s medical records—it’s reasonable to assume that innovative medical laboratories might consider 23andMe’s move a competitive threat to their own efforts to capitalize on combining lab test results with patients’ medical histories, drug profiles, and demographic data.

23andMe plans to use third-party medical network Human API to collect and manage the data. Involvement in the beta test is voluntary and currently only some of the genetic company’s customers are being invited to participate, CNBC reported.

Apple Healthcare, 23andMe, and Predicting Disease

The announcement did not go unnoticed by Apple, which has its own stake in the health data market. Apple Healthcare’s product line includes:

Mobile device apps for using at point-of-care in hospitals;

iPhone apps that let customers store and share their medical and pharmaceutical histories and be in contact with providers;

ResearchKit, which lets researchers build specialized apps for their medical research;

CareKit, which lets developers build specialized monitoring apps for patients with chronic conditions; and

Apple Watch, which doubles as a medical device for heart monitoring.

What Apple does not have is genetic data, which is an issue.

An Apple Insider post notes, “As structured, 23andMe’s system has advantages over Apple’s system including not just genetic data, but insights into risks for chronic disease.”

This is significant. The ability to predict a person’s predisposition to specific chronic diseases, such as cancer, is at the heart of Precision Medicine. Should this capability become not only viable and reliable but affordable as well, 23andMe could have a sizeable advantage in that aspect of the health data market.

Anne Wojcicki (above) is CEO and co-founder of 23andMe. The genetic company is inviting some of its customers to combine their medical information—including clinical laboratory test results and medication histories—with their stored genetic data. Customers would have access to the combined data and be able to share it with providers. In exchange, 23andMe gets to sell it to pharmaceutical companies and diagnostics developers. If successful and popular with the eight to 10-million peoplewho have reportedly purchased its test kits, 23andMe could produce a significant source of revenue. (Photo copyright: Inc.)

Genetic Test Results Combined with Clinical Laboratory

Test Results

23andMe is hopeful that after people receive their genetic test

results, they will then elect to add their clinical laboratory results, medical

histories, and prescription drug information to their accounts as well. 23andMe

claims its goal is to provide customers with easy, integrated access to health

data that is typically scattered across multiple systems, and to assist with

medical research.

“It’s a clever move,” Ruby Gadelrab, former Vice President of Commercial Marketing at 23andMe who now provides consulting services to health tech companies, told CNBC. “For consumers, health data is fragmented, and this is a step towards helping them aggregate more of it.”

CNBC also reported that Gadelrab said such a database

“might help 23andMe provide people with information about their risks for complex,

chronic ailments like diabetes, where it’s helpful for scientists to access a

data-set that incorporates information about individual health habits,

medications, family history and more.”

Of course, it bears saying that the revenue generated from cornering

the market on combined medical, pharmaceutical, and genetic data from upwards

of 10-million customers would be a sizable boon to the genetic test company.

CNBC reported that “the company confirmed that it’s a

beta program that will be gradually rolled out to all users but declined to

comment further on its plans. The service is still being piloted, said a person

familiar with the matter, and the product could change depending on how it’s

received.”

Will 23andMe Have to Take on Apple?

23andMe already earns a large portion of its revenue through

research collaborations with pharmaceutical companies, and it hopes to leverage

those collaborations to produce new drug therapies, CNBC reported.

This new venture, however, brings 23andMe into competition

with Apple on providing a centralized location from where consumers can access

and share their health data. But it also adds something that Apple does not

have—genetic data that can provide insight into consumers’ predispositions to

certain diseases, which also can aid in the development of precision medicine

treatments for those diseases.

Whether Apple Healthcare perceives 23andMe’s encroachment on

the health data market as a threat remains to be seen.

Nevertheless, this is another example of a prominent company

attempting to capitalize on marketable customer information. Adding medical information

to its collected genetic data could position 23andMe to generate significant

revenue by selling the merged data to pharmaceutical companies and diagnostics

developers, while also helping patients easily access and share their data with

healthcare providers.

It’s a smart move, and those clinical laboratory executives

developing ways to produce revenue from their lab organization’s patient lab test

data will want to watch closely as 23andMe navigates this new market.

In response to Harvard’s conclusions, the Joint Commission claimed the study contained “factual errors” and “multiple methodological flaws” in strong rebuttals to findings

Today’s emphasis on value-based healthcare rewards hospitals, physicians, clinical laboratories, and other healthcare service providers for improved patient outcomes. But does hospital accreditation play a role in those improved outcomes? A study published in the British Medical Journal (BMJ) suggests that hospital accreditation may not directly correlate to improved patient care and that one accrediting organization may be just as good as another.

Researchers at Harvard T.H. Chan School of Public Health (Harvard) conducted the study. They looked at healthcare outcomes from 4,400 US hospitals between 2014 and 2017, of which 3,337 were accredited (2,847 by The Joint Commission) and 1,063 received state-based reviews.

The researchers’ objective was “To determine whether

patients admitted to US hospitals that are accredited have better outcomes than

those admitted to hospitals reviewed through state surveys, and whether

accreditation by The Joint Commission (the largest and most well-known

accrediting body with an international presence) confers any additional

benefits for patients compared with other independent accrediting

organizations.”

In their published results, the Harvard researchers concluded:

“Patients treated at accredited hospitals had

lower 30-day mortality rates (although not statistically significant lower

rates, based on the prespecified P value threshold) than those at hospitals

that were reviewed by a state survey agency … but nearly identical rates of

mortality for the six surgical conditions;

“Readmissions for the 15 medical conditions at

30 days were significantly lower at accredited hospitals than at state survey …

but did not differ for the surgical conditions;

No statistically significant differences were

seen in 30-day mortality or readmission rates (for both the medical or surgical

conditions) between hospitals accredited by The Joint Commission and those

accredited by other independent organizations.”

Why is this finding important? As the largest independent

accrediting organization, The Joint Commission holds enormous influence over

doctors and other healthcare service providers. The Joint Commission accredits more

than 21,000 US healthcare providers, as well as hospitals throughout the world.

Most states require Joint Commission accreditation for hospitals to receive

Medicare/Medicaid reimbursements.

However, Harvard’s study found hospitals accredited by the

Joint Commission had no better patient outcomes than hospitals reviewed by

state survey agencies. The conclusions published by this research team casts

doubt on the perceived higher value of the Joint Commission’s accreditation

over other accrediting bodies, and on the value of accreditation itself.

“There was no evidence in this study to indicate that

patients choosing a hospital accredited by the Joint Commission confer any

healthcare benefits over choosing a hospital accredited by another independent

accrediting organization,” the researchers concluded in their paper.

Ashish Jha, MD, MPH (above) K. T. Li Professor of Global Health and Health Policy at the Harvard T. H. Chan School of Public, co-authored the Harvard study. He maintains that for accreditation to ensure hospital quality, accreditation standards must be refocused. “First, there must be a clear delineation of high-quality care (good outcomes, good experience) and that must be the guiding principle behind accreditation,” he wrote in JAMA Forum. “Hospitals should be held accountable for those outcomes. Accrediting bodies should focus on those processes and structural factors that have been convincingly shown to be associated with good outcomes.” (Photo copyright: Harvard.)

Not So Fast!

The Joint Commission is an independent, not-for-profit organization

that has accredited hospitals for nearly 70 years. Approximately 81% of

hospitals accredited in the US are accredited by the Joint Commission. So, of

course, the Joint Commission took issue with the Harvard researchers’ findings.

In a formal statement and a response published in BMJ, the Joint Commission cited “factual errors” and “multiple methodological flaws that make the [study] results invalid.”

Nonetheless, the Joint Commission also pointed out that

Joint Commission-accredited hospitals were found by the researchers to demonstrate

lower mortality than state-surveyed hospitals and lower readmission rates for

the medical conditions cited.

“While study authors considered the differences ‘modest,’

applying them to the more than three million patients with medical conditions

addressed in this study indicates that patients treated in Joint

Commission-accredited hospitals experienced 12,000 fewer deaths and 24,000

fewer readmissions,” the formal statement said. “We believe that makes a

difference to patients as much as it does to us.”

Joint Commission Partners with Leapfrog Group

Scrutiny of hospital accrediting bodies is not new. A 2002 article by The Dark Report, Dark Daily’s sister publication, reported on the Joint Commission’s decision to become a “formal partner” in the Leapfrog Group, a non-profit organization founded in 2000 that advocates for improved hospital safety and quality. (See TDR, “Provider Performance Ranking Now Hitting Healthcare System,” January 28, 2002.)

The Joint Commission announced the partnership one day before the Leapfrog Group’s release of data in the journal Quality Management in Healthcare showing “that a hospital’s accreditation status did not correlate to better quality and safety of patient care. The study specifically noted that hospitals with higher-than-average rates of deaths and complications often received favorable scores from the [Joint Commission],” TDR reported.

However, as Robert Michel, TDR’s Editor-in-Chief and Publisher, noted in the article, “The [Joint Commission’s] willingness to partner with the Leapfrog Group is a significant event. The timing of the [Joint Commission’s] announcement, one day before Leapfrog made its hospital data available to the public, demonstrates that it will become more responsive to the quality concerns of employers.

“For laboratory executives and pathologists,” Michel

continued, “this is a signal event in determining how the healthcare system

will evolve in the next few years. I believe it is the first of what will become

a major effort to identify, measure, and report on the quality performance of

all categories of healthcare providers.”

Michel made his comments in 2002. Today, hospital and

individual health provider reimbursements are increasingly based on those very

performance and quality-of-outcome reports.

Healthcare systems now publish data on healthcare providers so

patients can make informed decisions. It is consistent with the trend to rank

providers by patient outcomes and similar metrics, which TDR predicted

nearly two decades ago.

Moreover, the growing availability of the outcomes data from

hospitals, physicians, and other types of providers is a signal to both

clinical laboratories and individual pathologists that public scorecards on the

quality, outcomes, and costs of their labs or their professional pathology

services are coming.

However, since major change in the healthcare system takes

years to achieve, public scorecards for labs and pathologists are probably

still years away as well.

Through partnerships with CVS, Utah Health, and Kaiser Permanente the new UPSFF drone service could deliver savings to healthcare consumers and reduced TATs for clinical laboratories

United Parcel Service (UPS) successfully delivered by air medical prescriptions from a CVS pharmacy to customers’ residences in Cary N.C. This was the next step in the package delivery company’s plan to become a major player in the use of drones in healthcare and it has major implications for clinical laboratories and pathology groups.

Earlier this year, Dark Daily’s sister publication, The Dark Report (TDR), covered UPS’ launch of a drone delivery service on the WakeMed Health and Hospitals medical campus in Raleigh, N.C. The implementation followed a two-year test period during which UPS used drones manufactured by Matternet, a company in Menlo Park, Calif., to fly clinical laboratory specimens from a medical complex of physicians’ offices to the health system’s clinical laboratory more than 100 times. (See TDR, “WakeMed Uses Drone to Deliver Patient Specimens,” April 8, 2019.)

At the 24th Annual Executive War College on Lab and Pathology Management in April, Chairman and CEO David Abney (above) explained why UPS is investing in drone technology for clinical laboratory health network delivery. “Healthcare is a strategic imperative for us,” Abney said. “We deliver a lot of important things, but lab [shipments] are critical, and they’re very much a part of patient care.” (Photo copyright: Dark Daily.)

In October, UPS signed a letter of intent with CVS Health to “explore drone deliveries, expanding UPS’ sights from hospital campuses to the homes of CVS customers as it builds out its drone delivery subsidiary,” Modern Healthcare reported.

In November, UPS succeeded in these goals with UPS Flight Forward, Inc. (UPSFF), UPS’ new drone delivery service which, according to its website, is the first “drone airline” to receive full Part 135 certification (Package Delivery by Drone) from the Federal Aviation Administration (FAA).

“This drone delivery, the first of its kind in the industry, demonstrates what’s possible for our customers who can’t easily make it into our stores,” said Kevin Hourican, EVP, CVS Health and President of CVS Pharmacy, in a UPS press release. “CVS is exploring many types of delivery options for urban, suburban, and rural markets. We see big potential in drone delivery in rural communities where life-saving medications are needed and consumers at times cannot conveniently access one of our stores.”

Drones Deliver Clinical Lab Specimens and Pharmaceuticals

Since March, UPSFF has completed more than 1,500 drone

flights (with 8,000 clinical laboratory samples) at WakeMed in Raleigh, N.C.

UPS’ drone delivery decreased delivery time of clinical laboratory specimens

between WakeMed’s physician office building to the hospital-based lab from 19

minutes to three minutes, according to UPS data reported in October by an Advisory

Board daily briefing.

WakeMed is seeking to “provide advantages in patient care

that cannot be obtained in any other way” Michael

Weinstein, MD, PhD, Director of Pathology Laboratories at WakeMed, told TDR.

With the signing of the UPS (NYSE:UPS)-UPSFF (UPS Flight

Forward)-CVS (NYSE:CVS.N) agreement in October—and initial first flights which

took place on November 1 between a CVS pharmacy and customers’ residences in

Cary, NC—UPS completed the “the first revenue-generating drone delivery of a

medical prescription from a CVS pharmacy directly to a consumer’s home,” the

UPS press release states.

“When we launched UPS Flight Forward, we said we would move quickly to scale this business … and that’s exactly what we are doing,” Scott Price (above), UPS Chief Strategy and Transformation Officer, told Supply Chain Dive. “We started with a hospital campus environment and are now expanding scale and use-cases,” he added. Clinical laboratories can probably look forward to similar UPS drone delivery services in all 50 states and Washington, DC. (Photo copyright: UPS.)

Other Healthcare Organizations on Board

WakeMed and CVS are not alone in UPS drone deployment for

healthcare deliveries. Advisory Board reported that UPSFF also partnered

with other healthcare systems to provide drone flights for on-campus delivery of

pharmaceuticals and medical supplies, including:

AmerisourceBergen:

to move pharmaceuticals, supplies, and records to “qualifying” medical

campuses;

Kaiser

Permanente: to send medical supplies between buildings at different campus

sites; and

University

of Utah Health’s hospital campuses: to transport biological samples,

documents, supplies, and medical instruments between their facilities.

Drone delivery of clinical laboratory specimens is swiftly become a global reality that labs should watch closely. Past Dark Daily e-briefings reported on drone deliveries being conducted in Virginia, North Carolina, Australia, Switzerland, and Rwanda.

Pathologists and medical laboratory managers need to stay

abreast of these developments, as widespread drone delivery of clinical laboratory

specimens may happen on a surprisingly fast timeline. Drone delivery already

has TAT improvement implications and could be a way for labs to differentiate

their businesses and enhance workflow.

Clinical laboratory leaders are aware that reference pricing is a tool employers and health insurer can use to reduce the wide variation different providers charge for the same clinical service. In 2016 our sister publication, The Dark Report, devoted an entire issue to the subject of reference pricing. (See TDR, “The Newest Threat to Lab Revenues: Reference Pricing in Healthcare,” September 6, 2016.)

The Dark Report wrote about the reference pricing pilot conducted by Safeway, the grocery chain, in collaboration with Anthem, Inc. (NYSE:ANTM), the large health insurance company. The reference pricing program had these elements:

When Safeway employees and their beneficiaries chose a lab that priced its tests below the 60th percentile, the patient qualified for the health plan’s benefits. But if the patient chose a lab with test prices above the 60th percentile, that patient was responsible for the full cost of the test.

Safeway employees and their beneficiaries were given a real-time price checking tool that they could access by web browser and smart phone. This app, developed by Castlight Health, Inc., of San Francisco, showed the prices each lab in the Safeway/Anthem network charged for the same lab test, along with the percentile price of that test.

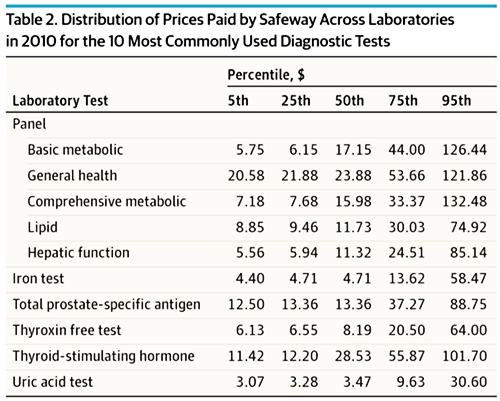

As reported in JAMA Internal Medicine, Safeway introduced reference pricing into its health insurance design for 15,000 employees in 2011. Three years later, the company and its employees were spending 32% less for clinical laboratory tests and saved $2.57 million during the years 2011 to 2013.

The reference pricing program at Safeway, which focused

primarily on clinical laboratory testing, succeeded because of the large

variability in how different labs price the same tests. For example, as TDR

reported:

For a basic metabolic panel, which was the most

commonly prescribed test, prices among different labs ranged from $5.75 to

$126.44; and

Prices for a lipid panel ranged from $8.85 to

$74.92.

The graphic above, taken from the Safeway/Anthem observational study of “changes in laboratory pricing and selection by employees … before and after a reference pricing policy for laboratory services,” illustrates the wide range of prices Safeway paid for the 10 most common clinical laboratory tests. (Graphic copyright: American Medical Association/JAMA Internal Medicine.)

Typically, a reference pricing arrangement is done to lower

costs, decrease disparities in pricing for similar medical services, and make

health plans more attractive to employers. This is why state health plans are

looking at implementing reference price reimbursement models as a way to reduce

healthcare costs for state employees and other beneficiaries.

North Carolina Providers Respond Negatively to State Reference

Pricing Plan

North Carolina’s State Health Plan encountered resistance

from the state’s medical community when it attempted to implement a similar

reference-price reimbursement model.

The state’s health plan covers more than 727,000

beneficiaries, including teachers, state employees, retired employees, and

their dependents. It is overseen by the State Treasurer and administered by BlueCross

BlueShield of North Carolina (Blue Cross NC).

In October 2018, North Carolina’s state health plan board of

trustees unanimously approved the Clear

Pricing Project, a reference-pricing program championed by State Treasurer Dale Folwell. A 2019 Blue

Cross NC State Health Plan Network Master Reimbursement Exhibit document

states, beginning in 2020, most hospitals would get 160% of the Medicare rate

for inpatient services and 230% for outpatient services; rural providers would

get more.

Pricing for medical lab and pathology services also was set

at 160% of the Medicare rate. The document states, “Except for services

identified by Medicare as CLIA Excluded or CLIA Waiver,

In-Office Laboratory Service fees will be limited to those services for which

you have provided Blue Cross and Blue Shield of North Carolina with evidence of

CLIA

certification.”

North Carolina’s healthcare providers had no choice but to

agree to the pricing to be included in the state’s provider network, but they

were not happy about the arrangement.

NCHA Warns Hundreds of Providers Could Be Pushed Out of

Network

Hospitals countered with a public relations and lobbying

campaign through the North Carolina Healthcare

Association (NCHA). Soon after Folwell’s announcement, the NCHA issued a

statement claiming that his plan “could force hundreds of providers out of

the State Health Plan network or out of business.” The NCHA estimated the

potential losses to hospitals and health systems at “upwards of $400 million.”

In the statement, NCHA President Steve

Lawler said, “We believe the treasurer is not being transparent about what

this proposal will do to state health plan members and their families.”

As an alternative, the NCHA proposed that the state examine

value-based approaches such as “case management, outcomes-based payment models,

and member education as ways to manage costs.”

The organization established a web page explaining its opposition

to the state’s plan and pushed for legislation that would delay its

implementation. House

Bill 184, which sought to delay implementation of the state’s healthcare

reimbursement plan, passed the state House of Representatives in April, before

stalling in the Senate in May, North

Carolina Health News reported.

Many providers simply refused to sign the necessary

contracts, Modern

Healthcare reported, even after Folwell agreed to increase the average

rate to 196%. In August, he relented and announced that for 2020, the provider

network will consist of the North Carolina State Health Plan Network—28,000

providers that had signed on to the Clear Pricing Project—plus the Blue Options

PPO Network, which includes providers that had not agreed to the new pricing.

That makes for a total of more than 68,000 providers, states

a news

release from the treasurer’s office. After the change was announced,

providers in the State Health Plan Network were permitted to revert to the Blue

Options PPO Network rates.

States may approach implementing reference pricing in

different ways, which will likely lead to a distinct disparity in outcomes. Nevertheless,

whatever approach is used, medical laboratories and pathology groups will want

to understand how reference pricing works and how it may be implemented in

their states.

Armed with that understanding, they may want to pursue a

proactive strategy of aligning the prices of their lab tests to be at the 50th percentile

or lower to avoid being the highest-priced labs in their communities and

regions.