Dettwyler is set to retire at age 92 after a long career helping clinical laboratories with their coding and billing systems

When William Dettwyler, MT, began working in a clinical laboratory, Harry Truman was president of the United States and scientists had not yet discovered the structure of DNA. Now, as he approaches his 92nd birthday in March, he is finally ready to retire from a career that has spanned more than seven decades, from bench work as a medical laboratory technician (MLT) to assisting labs with their medical coding and medical billing challenges.

Along the way, one of his coding innovations helped the State of Oregon save substantial sums in its Medicaid program. He also helped many medical laboratories increase reimbursement by correcting their coding mistakes. This from someone who left school after eighth grade to help on his family’s farm in rural Oregon.

In an exclusive interview with Dark Daily, Dettwyler discusses his long career and offered pointers for labs on improving their coding and reimbursement procedures.

Back in the 1980s, when he began his consulting work for labs, “they were very poor at billing,” he recalled. “Hospital billing staff didn’t understand lab coding. Reference laboratories didn’t do a good job of picking the right codes or even billing all the codes. Up until around the 1970s, hospitals didn’t even have to bill individual lab procedures with CPT codes. They billed with a revenue center code for all their lab services.”

These days “people are much more sophisticated,” he notes. “There are fewer coding problems compared to what it was in the 1980s and 1990s up to the 2010s.” However, he says he still has a handful of clients who call on his expertise.

“It was not unusual to go to a large university medical center and in three days tell the CFO on my exit review that the following year their lab would bring in about a half million more in revenue, just from my coding review. But I did not reveal to them that I had only gone to the eighth grade in a little one room school and was the lone graduate in my eighth-grade class,” wrote William Dettwyler, MT (above), owner of Codus Medicus in Salem, Ore., in an article he penned for Medical Laboratory Observer. For 75 years Dettwyler worked in the clinical laboratory industry. For much of that time he helped labs all over America improve their coding and reimbursement systems. (Photo copyright: LinkedIn.)

How It All Began

Dettwyler got his first taste of lab work in the early 1950s as a teenager washing glassware for a medical laboratory technician at a local medical practice. A few years later he completed an MLT program at Oregon Institute of Technology in Klamath Falls and landed his first lab tech job at a clinic in Portland.

His entry to consulting came in the early 1970s while he was working for a medical group in Salem. “I was helping the accounting personnel with their billing and noticed that Medicaid was not paying for a common test for syphilis that I was performing,” he recalled. “I contacted Medicaid, and they told me they didn’t understand laboratory procedures.”

After that, “they started to call me frequently with laboratory questions,” he said. “It wasn’t long before they asked me to help them on a part-time basis.” He also assisted with questions related to radiology.

By 1976, Dettwyler was devoting 35 hours a week to assisting the state Medicaid agency while still working as a lab tech.

Simple Hack Ends Overpayments

One of his career highlights came around 1981, when he discovered that the agency was overpaying for some pathology and radiology procedures by as much as 200%.

“Pathologists and radiologists are paid based on whether they are performing the complete procedure—the technical component and the professional component—or just the professional component, where they interpret the results,” he explained.

When billing for just the professional component, the physicians would add two digits to the standard code, so it might come in as 88305-26. However, the state’s computer system could only accommodate a five-digit code, so the state was paying as if the providers had done everything.

“The computer techs said the software couldn’t handle a seven-digit number in a five-digit box, so I devised a way for the computer to read the equivalent of seven digits,” he recalled.

His solution was to modify the codes so that the last digit was an alphabetic character. Instead of billing for code 88305-26, the physicians would bill for 8830F, and the state would pay them correctly.

Around that time, Dettwyler also began assisting a Medicare office in Portland. This forced him to cut back on his work as a lab tech. But he still worked around 60 hours a week.

“For most of my life, I’ve worked three jobs,” he said. “Work is my hobby.” He also had a large family to support—by 1976, he and his wife had 10 kids.

Transition to Lab Consulting

In 1986, the state was facing a budget shortfall and cut its Medicaid consultants, so Dettwyler decided to seek consulting work with labs while continuing to work at the bench.

“I really liked the coding because I had very little competition,” he said. “But I wanted to keep working in the laboratory mainly to understand the problems.”

While working for the state, Dettwyler attended coding seminars and workshops. He noticed that labs were losing revenue due to poor billing practices. “They didn’t understand all the coding complexities, so they really hungered for this kind of assistance.”

But first, he had to find clients. So he partnered with another lab tech who was offering similar consulting services.

Business picked up after Dettwyler contributed an article to the trade publication Medical Laboratory Observer about his process, which he calls “procedure code verification and post payment analysis.”

“That went like gangbusters,” he said. “We started getting calls from all over the country.”

Dettwyler later split from his partner and went to work on his own.

“I would sit down with the person who was responsible for coding, usually the lab or radiology manager,” he explained. “We would go over the chargemaster and cover every procedure to make sure the code and units were correct. When I was done, I would give them a report of what codes we changed and why we changed them.”

Beginning in 1989, he signed on as a contractor for another consultancy, Health Systems Concepts on the East Coast, where he remained until 2019.

Advice to the Current Generation

What is Dettwyler’s advice for someone who wants to follow in his footsteps and assist labs with their coding? “I wouldn’t recommend it now,” he said. “There’s less need for that kind of assistance than in the past.”

However, he does find that labs still run into problems. The greatest need, he says, is in molecular diagnostics, due to the complexity of the procedures.

In addition, labs are sometimes confused by coding for therapeutic drug monitoring, in which a doctor is gauging a patient’s reaction to a therapy versus screening for substance abuse. “Those issues are often misunderstood,” he said.

Microbiology also poses coding challenges, he noted, because of the steps required to identify the pathogen and determine antibiotic susceptibility. “It requires quite a bit of additional coding,” he said. “Some labs don’t understand that they can’t just bill a code for culture and sensitivity. They have to bill for the individual portions.”

Labs that work with reference labs also have to be careful to verify codes for specific procedures. “I’ll review the codes used by reference labs and, surprisingly, they’re not always correct. Reference labs sometimes get it wrong.”

If someone does want to become a coding expert, Dettwyler suggests that “they should first have experience as a lab tech, especially in microbiology, because of the additional coding. And they should try to work with somebody who is already doing it. Then, they should work with the billing department to learn how it operates.”

He also advises clinical laboratory managers to follow the latest developments in the field by reading lab publications such as The Dark Report. “You have to do that to keep current,” he said.

Despite never completing high school, Dettwyler eventually received his GED and an associate degree. “But the degrees didn’t really help me,” he said. “Much of it was on-the-job training and keeping my eyes open and listening.”

Clinical laboratories are being squeezed on both sides as rising healthcare costs affect their patients while increasing health plan costs impact their employees’ health coverage

When UnitedHealthcare CEO Brian Thompson was murdered on Dec. 4, the nation’s attention focused on the negative impact ever-increasing costs of healthcare coverage is having on the average American. Clinical laboratories and anatomic pathology groups experience this trend firsthand as annual increases in the cost of health plans affect their employees.

To understand just how raw the public is feeling about health insurance, consider that in a recent Emerson College poll, 41% of respondents ages 18-29 stated that Thompson’s murder was “completely” or “somewhat” acceptable.

While the majority of the country believes that such violence is not an acceptable way to solve one’s problems, the message is clear that Americans’ waning trust in health insurance companies has reached unhealthy levels.

“Health insurance costs are far outpacing inflation, leaving more consumers on the hook each year for thousands of dollars in out-of-pocket expenses. At the same time, some insurers are rejecting nearly one in five claims. That double whammy is leaving Americans paying more for coverage yet sometimes feeling like they’re getting less in return,” CBS News reported.

Twenty-five years of increases from the insurance industry make it clear why the relationships between healthcare consumers and insurance companies has soured.

“Employers are shelling out the equivalent of buying an economy car for every worker every year to pay for family coverage,” said Kaiser Family Foundation President and CEO Drew Altman (above) in a news release. “In the tight labor market in recent years, they have not been able to continue offloading costs onto workers who are already struggling with healthcare bills.” Clinical laboratories and pathology groups are among those employers struggling to provide affordable health coverage for their employees. (Photo copyright. Kaiser Family Foundation.)

People Are Frustrated

The cost of living in America has risen dramatically in the past decade. So much so that people are increasingly becoming frustrated and lashing out against companies that appear to be making record profits while their customers struggle to pay for their products and services.

A recent Kaiser Family Foundation (KFF) Health Tracking Poll found that “About one in five adults (19%) say they have difficulty affording their bills each month and about four in 10 (37%) say they are just able to afford their bills each month, while a little over four in 10 (44%) say they are both able to pay their bills and have some money left over.”

Simultaneously, according to KFF, “Employees’ share of their [health insurance] premiums are also on the rise, with a worker with family coverage typically paying premiums of $5,700 per year in 2017, the most recent year for that data, up from about $1,600 in 2000. … The average family deductible—the amount paid out-of-pocket before insurance kicks in—has increased from $2,500 in 2013 to $3,700 in 2023.”

This double-whammy in costs has a growing number of American’s worrying about unexpected healthcare bills and the overall cost of keeping their families adequately covered for the future.

“We’ve gotten to a point where healthcare is so inaccessible and unaffordable, people are justified in their frustrations,” said Céline Gounder, MD, a CBS News medical contributor and editor-at-large for public health at KFF Health News.

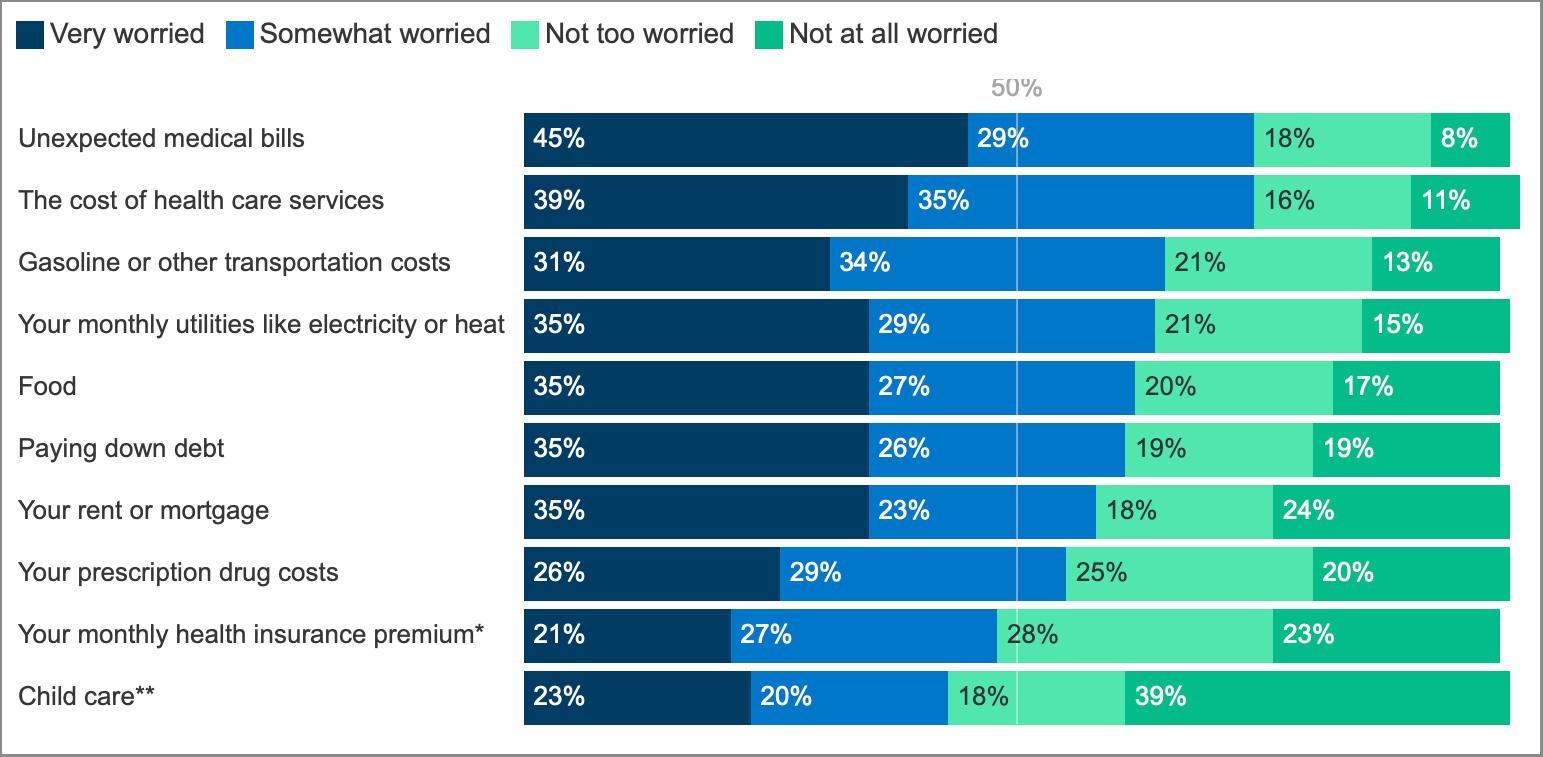

The chart above taken from a KFF Health Tracking Poll (Jan. 30-Feb. 7, 2024) shows participants’ answers when asked, “How worried, if at all, are you about being able to afford each of the following for you and your family?” Results indicate, according to KFF, that three in four people polled are worried about paying future healthcare bills and covering increasing insurance costs. (Graphic copyright: KFF.)

AI and Coverage Denials

Coverage denials is another sore spot for many people, impacting nearly one in five claims in nongroup qualified health plans in 2021, KFF found. This ranged from 2% to 49% depending on the company.

“When you are paying for something, they don’t give it to you, and they keep raising prices … you will be frustrated by that,” Holden Karau, a software engineer and creator of Fight Health Insurance, a free online service that helps people appeal their denials, told CBS News. Karau’s company uses artificial intelligence (AI) to help customers create appeal letters.

But the use of AI in healthcare coverage has also drawn criticism. Insurance companies are increasingly using AI to review claims and issue denials, and the lack of transparency has led to lawsuits. Last year, CBS News covered lawsuits brought by the families of two deceased individuals who accused UnitedHealthcare of “knowingly” using a “faulty” AI algorithm to deny the patients medically necessary treatments.

Karau noted, “With AI tools on the insurance side, they have very little negative consequences for denying procedures,” CBS News reported. “We are seeing really high denial rates triggered by AI. And on the patient and provider side, they don’t have the tools to fight back,” she added.

“Unhappiness with insurers stems from two things: ‘I’m sick and I’m getting hassled,’ and the second is very much cost—‘I’m paying more than I used to, and I’m paying more than my wages went up,’” Rob Andrews, CEO of Health Transformation Alliance, a company that helps healthcare providers and other self-insured companies improve coverage for their employees, told CBS News. “A lot of people think they are getting less,” he added.

Effects on Clinical Laboratories

Even as individuals and families pay more money each year in healthcare premiums, deductibles, and out-of-pocket expenses, clinical laboratories have seen payers cut reimbursement for many lab tests. Thus, labs are dealing with a double-squeeze on their finances. On the income side, reimbursement for tests is under pressure, while on the cost side, the cost of health benefits for employees climbs annually.

Clinical lab and pathology managers will want to stay aware of these trends and take advantage of any opportunity to lower costs and pass on those savings to their patients.

Though the No Surprises Act was enacted to prevent such surprise billing, key aspects of the legislation are apparently not being enforced

Dani Yuengling thought she had properly prepared herself for the financial impact of a breast biopsy. After all, it’s a simple procedure, especially if done by fine needle aspiration (FNA). Then, the 35-year-old received a bill for $18,000! And that was after insurance and though she had received a much lower advanced quote, according to an NPR/Kaiser Health News (NPR/KHN) bill-of-the-month investigation.

So, what happened? And what can anatomic pathology groups and clinical laboratories do to ensure their patients don’t receive similar surprise bills?

Yuengling had lost her mother to breast cancer in 2017. Then, she found a lump in her own breast. Following a mammogram she decided to move forward with the biopsy. Her doctor referred her to Grand Strand Medical Center in Myrtle Beach, S.C.

But she needed to know how much the procedure would cost. Her health plan had a $6,000 deductible. She worried she might have to pay for the entire amount of a very expensive procedure.

However, the hospital’s online “Patient Payment Estimator” informed her that an uninsured patient typically pays about $1,400 for the procedure. Yuengling was relieved. She assumed that with insurance the amount would be even less, and thankfully, clinical laboratory test results of the biopsy found that she did not have breast cancer.

Then came the sticker shock! The bill broke down like this:

$17,979 was the total for her biopsy and everything that came with it.

Her insurer, Cigna, brought the cost down to the in-network negotiated rate of $8,424.14.

Her insurance then paid $3,254.47.

Yuengling was responsible for $5,169.67 which was the balance of her deductible.

So, why was the amount Yuengling owed higher than the bill would have been if she had been uninsured and paid cash for the procedure?

According to the NPR/KHN investigation, this is not an uncommon occurrence. The investigators reported that nearly 30% of American workers have high deductible health plans (HDHPs) and may face larger expenses than what a hospital’s cash price would have been for uninsured individuals.

Dani Yuengling (above) knew she had to take the lump in her breast seriously. Her mother had died of breast cancer. “It was the hardest experience, seeing her suffer,” Yuengling told NPR/KHN. Fortunately, following a biopsy procedure, clinical laboratory testing showed she was cancer free. But the bill for the procedure was shockingly higher than she’d expected based on the hospital’s patient payment estimator. (Photo copyright: Kaiser Health News.)

Take the Cash Price

In 2021, Bai was part of a John’s Hopkins research team that analyzed US hospital cash prices compared with commercial negotiated rates for specific healthcare services.

“The 70 CMS-specified hospital services represent 74 unique Current Procedural Terminology (CPT) diagnosis related group codes (four services were represented by two codes),” the authors wrote. “Cash prices and payer-specific negotiated prices for the 70 services were obtained from Turquoise Health, a data service company that specializes in collecting pricing information from hospitals.”

They continued, “Cash prices can affect the cost exposure of 26 million uninsured individuals and concern nearly one-third of US workers enrolled in high-deductible health plans, who are often responsible to pay for medical bills without a third-party contribution and thus are interested in having access to low cash prices. In contrast with the commercial price negotiated bilaterally between hospitals and insurers providing insurance plans, the cash price is determined unilaterally by the hospital and might be expected to be higher than negotiated prices.”

However, the team’s research found otherwise. “Across the 70 CMS-specified services … some hospitals set their cash price comparable to or lower than their commercial negotiated price,” they concluded.

Bai advises patients to ask healthcare providers about the cash price before undergoing any procedure no matter what their insurance status is. “It should be a norm,” she told NPR/KHN.

Federal No Surprises Act is not Foolproof

Yuengling was charged an extraordinarily high amount for her procedure compared to other hospitals in her area. Fair Health Consumer estimates the cost of the procedure Yuengling received cost an average of $3,500 at other local hospitals. Uninsured patients likely pay even less.

A spokesperson for Grand Street Medical Center blamed the inaccurate estimate on “a glitch” in the payment estimator system. The hospital has since removed some procedures from the tool until it can be corrected. Yuengling initially disputed the charge with the hospital but in the end decided to pay the full amount she owed.

NPR/KHN recommends that insured patients consult with their health insurance company to get an estimate before any procedure. That is the purpose of the No Surprises Act which was enacted as part of the Consolidated Appropriations Act, 2021 (CAA).

The law requires health insurance companies to provide their members with an estimate of medical costs upon their request. The Act also empowers patients to file federal complaints about their medical bills.

Patients who find themselves in a similar situation to Yuengling may want to consider paying the cash price for the procedure. Although this may not be common practice, Jacqueline Fox, JD, a healthcare attorney and professor of law at the University of South Carolina’s Joseph F. Rice School of Law, told NPR/KHN that there is not a law she is aware of that would prohibit patients from doing so.

Anatomic pathology groups and clinical laboratories should check that their online prices and estimation tools comply with the No Surprises Act to ensure that what happened to Yuengling does not happen with their patients. They also could inform patients on how to pay cash for procedures if insurance rates are too high. Medical professionals and patients can work together to achieve transparency in healthcare pricing.

ICHRAs allow companies to compensate employees for insurance purchased in individual markets and may help clinical laboratories reduce patient bad debt

Both employees and their employers are frustrated with current options for health coverage. Now, a recent report from the HRA Council suggests that more employers are turning to Health Reimbursement Arrangements (HRA) as an alternative to traditional group insurance coverage to cope with the increasing cost of employee health benefits. This will be of interest to clinical laboratories that must collect copays/deductibles from patients. Health insurance arrangements that make it easier for patients to pay help labs reduce patient bad debt.

According to its website, HRA Council is “dedicated to improving and expanding health coverage options for millions of workers by giving employers better ways to offer workers health insurance.”

The non-partisan advocacy organization, which consists of insurers, brokers, employers, and other stakeholders, estimates that only 500,000 workers are currently covered by these plans nationwide. That number of workers represents a 29% increase since 2023, with most of the growth coming from large employers.

Under HRA arrangements, employers provide non-taxed financial assistance to workers who then obtain coverage for themselves and/or their families in the insurance marketplace.

One type of plan, known as the Qualified Small Employer HRA (QSEHRA), was established as part of the 21st Century Cures Act, which Congress passed in 2016. QSEHRAs, however, are available only to businesses with 50 or fewer full-time (or equivalent) employees. Most of the recent growth has come from Individual Coverage HRAs (ICHRA), established under regulations issued by the Trump Administration in 2019.

In contrast to QSEHRAs, ICHRA plans are available to companies of any size, HRA Council notes.

“It’s a way to offer coverage to more diverse employee groups than ever before and set a budget that controls costs for the companies,” HRA Council Executive Director Robin Paoli told KFF Health News.

“ICHRAs are bringing a fresh new approach for employers who need a new or different solution to enable providing health benefits to their employees,” said Andrew Reeves (above), senior vice president and general manager, Gravie ICHRA, in the HRA Council report. Gravie is one of the health benefits companies allied with HRA Council. “Through the defined contribution approach that ICHRA brings, employers are now able to set their budget and enable employees to make their own individual decisions on the coverage they need for themselves and their families. ICHRAs are delivering an approach to employee benefits that is both stable yet at the same time flexible for the individual,” he added. These types of alternatives to traditional employer-sponsored health plans may also help clinical laboratories and anatomic pathology groups reduce patient bad debt. (Photo copyright: LinkedIn.)

How ICHRA Plans Work

As explained by HRA Council, “an ICHRA allows the employer to allocate to each employee a specific amount of money to spend on ACA [Affordable Care Act]-compliant individual health insurance plans. Employees then purchase their own plans, and the employer reimburses them up to the allocated amount.”

The rule allows employers to define up to 11 classes of workers and offer different benefit packages to each. These benefits can be based on characteristics such as:

geography,

whether the worker is employed full-time, part-time, or seasonally,

whether the worker is paid a salary or hourly wage, and

Employers can choose to offer ICHRAs to some classes and traditional group plans to others. Within each class of employee, employers also can vary compensation based on age—up to a 3-to-1 ratio—since older workers will generally pay higher premiums than younger ones.

For example, the HRA Council explains, “if an employer offers its 26-year-old employee $300 per month, it could only offer the oldest employee up to $900 per month.”

However, some consumer advocates have pointed to potential downsides of these plans, KFF Health News reported.

The rule, they concede, provides guardrails to prevent companies from moving only their sicker employees—the ones most costly to cover—to the individual market. For example, employers must offer the HRAs to entire classes of workers, and the rule prevents them from defining classes that contain only a small number of employees.

However, the authors contend that employers can still target HRAs to classes more likely to be sick while offering group coverage to other classes. In general, they argue, employers with sicker workforces will be most attracted to HRAs. As these workers enter individual insurance markets premiums could rise, particularly “in states that today have individual markets with a relatively low-cost mix of enrollees,” the authors wrote.

Although the rule allows companies to vary compensation based on age, older workers will still pay more for insurance unless the contribution covers the entire cost of the premium. This would likely make the HRAs “less attractive to employers by making it harder for employers to avoid leaving some workers worse off,” the authors noted.

The Brookings authors also observed that workers who accept the contributions are ineligible for premium tax credits enabled by the Affordable Care Act.

KFF Health News noted other potential downsides as well. “Plans sold on the individual market often have smaller provider networks and higher deductibles than employer-sponsored coverage. Premiums are often higher than for comparable group coverage.”

In addition, ICHRAs can create administrative headaches that have prompted some employers to return to group plans. “Instead of a company paying one group health plan premium, dozens of individual health insurers may need to be paid,” KFF Health News reported. “And employees who’ve never shopped for a plan before need help figuring out what coverage works for them and signing up.”

One Employer’s Example

KFF Health News highlighted one organization that appears to be happy with its newly adopted ICHRA: Lycoming College in Williamsport, Penn. The school, which provides health benefits for 400 faculty, staff, and family members, saved $1.4 million in healthcare costs in the first year after implementing the plan. “Employees saved an average of $1,200 each in premiums,” KFF noted.

Prior to the transition, one employee with a family of five paid $411 per month for a plan that had a $5,600 annual deductible. Under the ICHRA, he pays $790 per month with no deductible.

“It’s nice to have the choice to balance the high deductible versus the higher premium,” he told KFF Health News. Before, “it was tough to budget for that deductible.”

Which is where the benefit to clinical laboratories comes back in. Making it easier and affordable for patients to pay their co-pays and deductibles also means more patients showing up at labs for doctor ordered tests and blood draws.

Study findings highlight financial impact underinsured have on healthcare providers, including clinical laboratories and pathology groups

Commonwealth Fund’s 2024 Biennial Health Survey released in November shows that not only are Americans underinsured, but many are swimming in medical debt. This is not good news for clinical laboratories. Simply put, labs must collect deductibles, copays, and out of pocket amounts from insured patients. If the patient is underinsured, that means the lab probably has to collect more—even 100%—of total charges directly from the patient.

The study conducted between March and June of 2024 collected data from 8,201 respondents ages 18-64, and despite two of every three respondents carrying health insurance through their employers, one of every four is underinsured, according to a Commonwealth Fund news release.

A further 44% of respondents have medical debt, with one of every four calling their out-of-pocket payments “nearly unaffordable,” the news release notes. Additionally, one out of five had a gap in coverage during the year.

“Congress, employers, insurers, and healthcare providers all play a role in lowering costs and making care more affordable, so families can avoid debt and get the care they need to stay healthy,” said Sara R. Collins, PhD, lead study author and Commonwealth Fund Senior Scholar and Vice President for Health Care Coverage and Access and Tracking Health System Performance, in the news release.

Astute laboratory managers will look beyond the study’s face value and consider the profound impact such findings could have on their own labs.

“While having health insurance is always better than not having it, the findings challenge the implicit assumption that health insurance in the United States buys affordable access to care,” the Commonwealth Fund said of its 2023 study. This sentiment rings true in the Funds’ latest findings as well.

“The Affordable Care Act has covered 23 million people and cut the uninsured rate in half. But high costs are a serious problem for many Americans, regardless of the kind of insurance they have,” said Sara R. Collins, PhD (above), lead study author and Commonwealth Fund Senior Scholar and Vice President for Health Care Coverage and Access and Tracking Health System Performance, in a news release. Clinical laboratories and anatomic pathology groups are greatly affected by underinsured patients. (Photo copyright: Commonwealth Fund.)

Labs Often Must Collect Payments Upfront

Many patients are in high deductible health plans and may forgo or delay ordered lab tests. Labs collect patient deductibles, copays, and out-of-pocket expenses directly from patients. However, underinsured patients may be required to pay for 100% of the services they receive, requiring the lab to collect these payments upfront.

Underinsured patients already facing a mountain of debt may struggle to pay for lab services. The debt many owe is substantial. “Nearly half (48%) of all adults with medical debt owe $2,000 or more; one of five (21%) carry a staggering $5,000 or more in debt,” Commonwealth Fund noted in its study.

Thus, collecting money owed is proving to be a problem for healthcare providers. Patient collection rates are plummeting to 48%, with “providers writing off more bad debt from patients with insurance,” TechTarget reported.

“Lower patient collection rates left providers facing bad debt. The analysis showed that 1.54% was the bad debt write-offs as a percentage of total claim charges in 2023. Researchers note that the percentage may be small, but the total cash amount equated to over $17.4 billion last year,” TechTarget added.

Having some rather than no insurance is not the safety net for patients previously thought. When it comes to the insured, their debt “accounts for 53% of the estimated $17.4 billion that hospitals, health systems, and medical practices wrote off as bad debts in 2023,” Business Wire noted, citing data from Kodiak Solutions’ quarterly revenue cycle benchmarking report.

Delaying Critical Lab Tests

The challenges the insured face with debt impacts labs in the long run. A staggering 57% of survey respondents reported passing on needed care because they could not afford it, and of those, 41% said their health concerns worsened when they denied themselves that care, Commonwealth Fund noted.

Increasingly poor health means patients might struggle to collect sufficient income to pay for their now added expenses, further causing them to struggle to pay for anything insurance might not cover, such as doctor ordered lab tests.

The affect this has on hospitals and medical laboratories casts light on the healthcare marketplace as a whole. It’s a trend that needs to be further studied.

“Most hospital bad debt is associated with insured patients, and nearly one in three hospitals report over $10M in bad debt,” are two of the top five financial healthcare statistics reported by Definitive Healthcare in a 2023 report.

“Expanding patient collection strategies may be key to maximizing revenue and avoiding losses,” TechTarget suggested.

Possible Solutions

The Commonwealth Fund study made clear that employer-covered healthcare does not guarantee affordable care or that ample care will be provided. Possible solutions from the study called on policymakers to “expand coverage and lower costs for consumers.” It added that “extending enhanced premium tax credits and strengthening protections against medical debt could make coverage more protective and affordable.”

Until a solution can be found, it’s wise to stay abreast of this trend and how it can impact the bottom line of clinical laboratories and anatomic pathology groups nationwide.

Though the cost of clinical laboratory testing is not highlighted in KFF’s annual survey, it is a component in how much employers pay for healthcare plans for their employees

Employers now pay higher health insurance premiums than ever for family coverage. However, because of the current tight labor market, they are generally absorbing much of that increase rather than passing the higher costs on to their workers. That’s one key takeaway from KFF’s 26th annual Employer Health Benefits Survey, which the non-profit published on Oct. 9, 2024. While the report does not comment specifically about the cost of clinical laboratory testing or genetic testing and how they may contribute to rising insurance costs, it stands to reason they are part of growing healthcare costs for corporate health benefits.

The KFF survey found that premiums for family coverage increased 7% in 2024, reaching an average of $25,572. That follows a 7% increase in 2023. “Over the past five years—a period of high inflation (23%) and wage growth (28%)—the cumulative increase in premiums has been similar (24%),” KFF stated in a press release.

However, the amount paid by workers has gone up by less than $300 since 2019. It now stands at an average of $6,296, a total increase of 5% over five years. On average, workers covered 25% of family premium costs in 2024, down from 29% in 2023. Workers with single coverage paid an average of $1,368—16% of the annual premium cost—compared with 17% in 2023.

“Employers are shelling out the equivalent of buying an economy car for every worker every year to pay for family coverage,” KFF President and CEO Drew Altman, PhD (above), said in a press release. “In the tight labor market in recent years, they have not been able to continue offloading costs onto workers who are already struggling with healthcare bills.” Rising costs of clinical laboratory testing is always part of the mix contributing to increased worker insurance premiums for employers. (Photo copyright: KFF.)

HDHP/SO plans, as defined by KFF, “have a deductible of at least $1,000 for single coverage and $2,000 for family coverage and are offered with an HRA [Health Reimbursement Arrangement] or are HSA [health savings account]-qualified.” Point-of-service plans “have lower cost sharing for in-network provider services and do not require a primary care gatekeeper to screen for specialist and hospital visits,” the report states.

Cost Sharing via Deductibles

Average deductible amounts—which KFF identified as another form of cost-sharing—varied depending on the type of plan, employer size, and whether the worker had family or single coverage.

For workers with single coverage, average deductibles across all plan types rose from $1,655 in 2019 to $1,787 in 2024, a total five-year increase of about 8%. The average in 2023 was $1,735. These numbers were for in-network providers.

The report noted that some family plans calculate deductibles using an aggregate structure, “in which all family members’ out-of-pocket expenses count toward the deductible,” whereas others use a separate per-person structure. The report includes breakdowns of average deductibles across all types.

Who Offers the Best Benefits?

In general, the KFF report found that large companies—defined as those with 200 or more workers—tend to offer more generous health benefits than smaller ones. Virtually all large companies (98%) offered health benefits, while slightly more than half of small companies (53%) do so.

Among companies that do offer health benefits, the average deductible at a small firm was $2,575 compared to $1,538 at large firms. Among workers with family coverage, the average contribution toward overall premium costs was $7,947 (33%) at small firms compared to $5,697 (23%) at large firms. Among workers with single coverage, the numbers were $1,429 (16%) at small firms compared to $1,204 (14%) at large firms.

The report also found variations in overall premiums and health benefits across nine different industries. For example, healthcare firms paid the highest premiums for family coverage—an average of $26,864—followed by transportation/communications/utilities at $26,601. Companies in agriculture, mining, and construction paid the lowest premiums, an average of $22,654.

There were wide variations by industry in terms of how many firms offer any health benefits. Among state and local government entities, 83% offered health benefits, followed by transportation/communications/utilities (69%), manufacturing (65%), wholesale (62%), healthcare (58%), and finance (56%). Just 40% of retail businesses and 49% of agriculture/mining/construction businesses offered health benefits.

Health Screening Coverage

The KFF report did not include data about insurance coverage for clinical laboratory services. However, one section did address employer willingness to provide opportunities for health screening.

Among large businesses, 56% offered health risk assessments, in which individuals answer questions about their medical history, lifestyle, and other areas relevant to their health risks. A smaller number (44%) offer biometric screening, which “could include meeting a target body mass index (BMI) or cholesterol level, but not goals related to smoking,” the report said. Only 9% of small businesses offered biometric screening, the report found.

KFF conducted its survey between January and July 2024 among a random selection of public and private employers with at least three workers. The survey excluded federal government entities but included state and local government. A total of 2,142 employers responded.

Inflation during this current administration definitely hit consumers in the health insurance premium pocketbook. At the same time providers raised their own prices making it more expensive for people with HDHPs to come up with the cash required by their annual deductible. While clinical laboratory and genetic testing are not highlighted in KFF’s survey, they certainly play a role in increasing costs to healthcare consumers and are worth considering.