Data-driven proof supports decision-making that optimizes efficiency and boosts bottom lines in the face of shrinking margins and increased competition

Molecular and esoteric

testing developers continue to make advanced assays and diagnostic

technologies available to medical

laboratories. However, some laboratory senior management and stakeholders

may be reluctant to invest in them even though the market for such testing is

poised for significant growth.

That’s because lab shareholders might view these tests/services

as high-risk and it might not be immediately clear how—with proper

implementation—these services have the potential to improve lab financials and provide

higher-margin services to offset the shrinking margins of common high-volume

tests.

That’s where analytics can help lab managers, who’ve been tasked

with expanding their lab’s menu to include esoteric or molecular testing, justify

the expansion of services or answer questions regarding the lab’s financial

viability to do so.

Being able to answer those questions—such as whether to perform

anatomic

pathology, cytology,

and other advanced testing in-house or outsource, particularly in terms that c-suite

members, shareholders, and other lab decision makers will understand—is

critical to managing expectations and ensuring successful installation of the

new testing.

The approach Michigan-based Spectrum Health took to implement

analytics in their decision-making chain may be instructive.

Spectrum’s experience—through a partnership with LTS Health based in Chicago, IL., and by making use of PinpointBPS, a laboratory performance management system—showcases how laboratories can leverage analytics to not only increase key lab metrics, but do so with minimal risk. All while generating data that will inform critical members of the decision-making chain.

Data Modelling as

Tool for Laboratory Growth

Global Market Insights predicts an 8.5% compound

annual growth rate (CAGR) in molecular diagnostics alone between 2018 to

2024. Clinical laboratories that see automation and staffing as their primary

means for increasing throughput, reducing turnaround times, and optimizing lab

operations, will find Spectrum’s results useful.

Spectrum Health wanted to improve staff performance and

morale while also insourcing specialist testing without adding to the cost base

in their Advanced

Technology Laboratories (ATLs). These labs include—molecular diagnostics, flow cytometry, and cytogenetics—and require

a significant skilled staff investment. As such, Spectrum had questions about latent

capacity and potential costs in relation to their ability to expand service

offerings while maintaining optimal service levels.

They initially implemented PinpointBPS to reinforce the

ideas under consideration:

Optimizing staff schedules to match typical

order flows; and,

Implementation of automated liquid handlers.

Using

analytics, the lab staff was able to both simulate the proposed changes and

obtain quantitative data on how these changes would impact lab financials,

staff efficiency, latent lab capacity, and other key metrics. They could

accomplish all of this without making a single change to existing operations,

staff levels, or lab technologies.

Using analytics and data modelling, Spectrum discovered that

implementing a new staffing model would allow them to achieve several key

objectives—including:

Accounting for workload increases related to next-generation

sequencing (NGS)—using their existing staff.

More importantly, they were able to do so without the

significant hardware investment which they were previously considering.

“Analytics help to highlight areas of improvement through data comparisons and provide an empirical source of truth for determining the best course of action to reach laboratory goals and achieve sustainable, dependable results,” Kim Collison (above), Directory of Laboratory Services at Spectrum Health in Grand Rapids, Mich., told Dark Daily. “These systems also create a monitoring system to further iterate on or adjust improvements. This is accomplished while also gathering data ideal for presenting to the c-suite, shareholders, and other key members of the decision-making chain.” (Photo copyright: LTS Health.)

Much like modeling or

visualization might help to display complex medical data to aid diagnosis,

these systems can model and simulate data related to laboratory operations, integrate

with laboratory

information management systems (LIMS), and simulate

ideas to create quantified data about a range of important aspects including:

Assessment of staffing needs;

Highlighting potential workflow bottlenecks;

Determining latent laboratory capacity; and,

Assessing the value of advanced technology

laboratory investments.

“Everyone is vying for capital dollars,” Linda Flynn, Executive

Consultant at LS Flynn and Associates told Dark Daily. “Good data collected and

organized through data analytics can generate trust and understanding to help

position your proposals to c-suite members for greater success.”

Opportunity to Gain

Critical Knowledge for Your Clinical Laboratories

The webinar will include essential information for clinical laboratories

looking to increase certainty in the decision-making process using facts and

data and provide a solid understanding

for engagement in investment opportunities, c-suite members, and other senior

management and decision makers.

Attendees will also learn from a case study on how Spectrum

Health implemented PinpointBPS to develop an actionable, effective plan to

improve their operations, reduce turnaround times, and improve the value of

their laboratory operations based on facts and data generated within the lab.

Laboratory management, administrative directors, staff, and business

and financial managers of laboratories will want to attend this webinar and the

following Q/A session to obtain information on the impact BI analytics could

hold for their laboratories and how to best implement these new systems for optimal

results.

(To register for this

critical March 27th webinar, click here. Or, copy and paste this URL into your browser: https://www.darkdaily.com/product/webinar-using-data-analytics-to-optimize-your-investment/.)

Experts are skeptical of the value of public price lists based on hospital chargemasters due to complexity and poor reflection of actual costs

In another big step toward helping consumers view prices of medical procedures when selecting providers, the Centers for Medicare and Medicaid Services (CMS) passed the IPPS/LTCH PPS final rule, which requires hospitals to post a full list of hospital pricing information on their websites starting January 1, 2019.

Clinical laboratories, anatomic pathologists, and other diagnosticians doing business with their local health networks will now find their prices for tests and procedures listed on the hospitals’ chargemasters available to the public.

To meet rule requirements, pricing information posted by hospitals

must be:

• Published online in a publicly accessible place;

• Machine-readable;

• Downloadable to a spreadsheet; and,

• Updated at least once per year.

Outside of these requirements, the guidelines are vague. However,

based on coverage of initial pricing lists, additional revisions are expected.

A fact sheet discussing the major provisions of the final rule (CMS-1694-F), can be downloaded from the Federal Register.

Are the Price Lists

Accurate?

One of the biggest issues cited by the media relates to the

accuracy of pricing information. As most hospitals are posting data directly

from their chargemaster listings, the numbers listed for the public are likely

to differ from the actual prices billed. Final charges depend on each patient’s

insurance plan and the network status of the healthcare facility rendering the services.

While hospitals are now required to post their price lists in a machine-readable format, MedCity Newsreports that many facilities use medical codes and terminology in price lists that the average consumer might not understand.

To further compound the issue, many items are listed

individually. This requires consumers to go through thousands of price listings

and combine the listed prices one by one to get an estimate of total costs for

a procedure.

Brenda L. Reetz, CEO of Green County General Hospital in Indiana also spoke with the NYT, saying, “We’ve posted our prices, as required. But I really don’t think the information is what the consumer is actually wanting to see.”

“While many hospitals have said chargemaster information can be confusing for consumers, let me be clear, hospitals don’t have to wait for us to go further in helping their patients understand what care will cost. We look forward to more facilities exceeding our requirements,” Seema Verma (above right), Administrator, Center for Medicare and Medicaid Services (CMS), told Modern Healthcare. (Photo copyright: Fox Business.)

Concerns of Increased

Risk for Both Hospitals and Consumers

“There is no more powerful force than an informed consumer,” said Alex Azar II, Secretary of the US Department of Health and Human Services (HHS) during a speech to the Federation of American Hospitals (FAH). “There is no turning back to an unsustainable system that pays for procedures rather than value. In fact, the only option is to charge forward—for HHS to take bolder action, and for providers and payers to join with us,” he concluded.

But with the higher rates found on most hospital chargemasters,

and the difficulty in finding true costs using the new public pricing lists, some

experts are concerned the lists might cause an adverse reaction.

“We do not want patients to forgo needed care,” Tom Nickels, Executive Vice President for Government Affairs and Public Policy at the American Hospital Association (AHA), told Newsweek. “Especially if the quoted price is for the total cost of the service and not what the patient will be expected to pay out-of-pocket.”

This is a real risk. Hospitals and other healthcare

providers already are experiencing reduced volumes due to patients opting out

of important procedures because of cost worries. Chargemaster lists that do not

reflect the true impact of insurance, charity programs, and other variables could

exacerbate that problem.

And there is specific risk for clinical laboratories, as

they rarely have a public-facing element within hospitals. Physicians order medical

laboratory tests and patients either do or do not comply. There is no

opportunity for laboratories to explain that prices listed on the hospital site

might not reflect actual out-of-pocket costs. Could this be an opportunity for

enterprising clinical laboratory managers?

Future Transparency

Trends

“I think putting those prices out there—even with the acknowledgment that these aren’t the prices anyone pays unless they’re uninsured—may indeed still provoke conversations with hospital administrators,” Michael Abrams, Managing Partner of Healthcare Consultancy at Numerof and Associates, a strategic management consultant for the global healthcare sector, told MedCity News.

While experts might not find much value in the current

iteration of price lists, and the latest attempt to improve pricing

transparency by CMS, it offers medical laboratories and hospitals an

opportunity to assess current pricing models and decide how to best communicate

value to consumers as pricing transparency continues to mature and the US

shifts to value-based healthcare.

FDA cautions patients to not use data gained from the DTC test to make healthcare decisions on their own

Clinical laboratories continue to be impacted by the growing direct-to-consumer (DTC) testing market, as more walk-in lab customers order at-home tests. Now, the US Food and Drug Administration (FDA) has authorized a DTC test company to provide results of a pharmacogenetic (PGx) test to customers without needing a doctor’s order. This is the first genetic test of its kind to receive such FDA authorization and is in line with the government’s focus on precision medicine.

23andMe gained the authorization through the FDA’s de novo classification process, which the FDA uses to classify new devices that have no existing classification or comparabledevice on the market.

“We’ve continued to innovate through the FDA and pioneer safe, effective pathways for consumers to directly access genetic health information,” said Anne Wojcicki, co-founder and CEO of 23andMe, in a news release. “Pharmacogenetic reports are an important category of information for consumers to get access to, and I believe this authorization opens the door for consumers to work with their health providers to better manage their medications.”

However, some experts caution that informing patients

directly on how they metabolize medications based on genetic testing could

encourage them to bypass physicians and medical laboratories in the decision-making

process.

In a safety communication, the FDA alerted patients and

healthcare providers that “claims for many genetic tests to predict a patient’s

response to specific medications have not been reviewed by the FDA and may not

have the scientific or clinical evidence to support this use for most

medications. Changing drug treatment based on the results from such a genetic

test could lead to inappropriate treatment decisions and potentially serious

health consequences for the patient.”

Tim Stenzel, MD, PhD (above), Director, Office of In Vitro Diagnostics and Radiological Health at the FDA, told FierceBiotech, “This test should be used appropriately because it does not determine whether a medication is appropriate for a patient, does not provide medical advice, and does not diagnose any health conditions. Consumers should not use this test to make treatment decisions on their own.” (Photo copyright: LinkedIn.)

PGx Supports

Precision Medicine

Pharmacogenetics (PGx) is the study of how genetic differences among individuals cause

varied responses to certain drugs. Demand for PGx testing has increased

exponentially as it becomes more valuable to consumers. It could provide a path

to precision medicine treatment plans based on each patient’s genetic traits. And

help determine which drug therapies and dosages may be optimal and which

medicines should be avoided.

“This test is a step forward in

making information about genetic variants available directly to consumers and

better inform their discussions with their healthcare providers,” Stenzel told FierceBiotech. “We know that consumers

are increasingly interested in genetic information to help make decisions about

their healthcare.”

The genes and their variants examined in the 23andMe PGx

test are:

Innovative hospital and health networks also are starting to

make PGx tests available in primary care settings.

Sanford Imagenetics, part of the Sanford Health system, has produced a $49 laboratory-developed test (LDT) for genetic screening known as the Sanford Chip to help physicians select the most advantageous therapies for their patients. It uses a small amount of blood to identify patients’ risk for certain genetic diseases and determine which medications would be best for them.

Sanford Health, headquartered in Sioux Falls, SD, is one of

the largest health systems in the US with 44 hospitals, 1,400 physicians, and

more than 200 senior care locations in 26 states and nine countries.

Geisinger Health, headquartered in Danville, PA, has initiated a pilot project based on PGx testing. The genetic sequencing data from 2,500 patients will be reviewed to determine if they are taking the best medication for their health conditions. Patients in need of changes to their prescriptions will be contacted by Geisinger pharmacists for recommendations.

As consumer demand for PGx testing increases, DTC customers will

likely continue seeking new information about their genome. Clinical

laboratories could play a role in interpreting that data and assisting

pathologists and other healthcare providers determine the best drug therapies

for optimal health outcomes.

Experts blame insurance regulators for not ensuring the adequacy of healthcare networks that include hospital-based physicians, such as pathologists and radiologists

According to a recent study, clinical laboratories, anatomic pathologists, radiologists, and anesthesiologists top the list of providers who bill patients for the difference between what they charge for their services and a hospital’s contracted reimbursement rates.

This so-called “balance-billing” not only causes hardship for patients and consumers already shouldering a larger portion of their healthcare costs, but poses a public relations concern for service providers across the US healthcare industry as well.

Following public outcry from patients who received care at

what they believed to be in-network medical facilities, only then to be surprised

by bills from their care providers for the remaining balance not covered by

their insurance, the practice of balance billing has drawn increased scrutiny from

state and federal officials.

Medical Laboratory

Charges Top Reason for Surprise Bills

In their report, NORC notes that of those surveyed, 57% (567 individuals) acknowledged receiving a surprise medical bill they thought would be covered by their health insurance.

When asked about the network status of the doctor who

provided care during the episode related to the surprise bill, 79% responded

that charges were not for doctors being out-of-network for their insurance

plan. Medical laboratory-related charges were near the top of reasons patients

received surprise bills, with 51% of individuals receiving bills related to “a

laboratory test, like a blood test.”

Such surprise medical bills received frequent coverage in

2018. This has led many states to enact or discuss legislation to address the

practice and offer cost protections for patients.

Thus far, however, little change to existing regulations and

contract systems has been enacted to protect patients or help laboratories and

other service providers offer alternative payment solutions for patients.

There also are few requirements for insurance providers to verify

that plans include sufficient numbers of in-network service providers when

offering plans to consumers.

“Many news stories on ‘surprise’ billing blame physicians, because the bill is sent from the doctor’s office or billing company. But the insurance industry is the real culprit, in concert with insurance regulators who have not acted to require network adequacy,” R. Bruce Williams, MD (left), President, College of American Pathologists (CAP), and Geraldine B. McGinty, MD (right), Chair of the American College of Radiology Board of Chancellors, wrote in STAT. (Photos copyrights: College of American Pathologists/Geraldine McGinty.)

States Move to Change

Trends While Patients Continue to Experience Bill Shock

States are beginning to address surprise billing concerns ahead of action by insurance regulators and the federal government. In December, the Arizona Department of Insurance issued a news release outlining the agency’s plan to allow for arbitration questions for surprise out-of-network bills.

And, California effectively banned out-of-network billing from groups within in-network facilities in 2017 with Assembly Bill 72. However, the state only finalized reimbursement rates for service providers and patients affected by surprise bills in January of this year according to Capital Public Radio.

Many of these state-level regulations do not account for the complexity of creating rules based on emergency or non-emergency care or the insurance providers in question. For example, Assembly Bill 72 does not apply to “Medicare, Medi-Cal, out-of-state plans, self-insured employer plans, or other products regulated by federal law,” according to a news release from the California Society of Anesthesiologists.

Finding Fair

Solutions for Both Patients and Care Providers

Speaking with Kaiser Health News about a report of a man in Texas receiving a $109,000 surprise bill related to treatment after a heart attack, Rep. Lloyd Doggett of Texas said, “This is a nationwide problem, and we need a nationwide solution. We have a system where the patient, the most vulnerable person of all those involved, is caught between the insurer and the healthcare provider … these problems are solvable.”

Modern Healthcarerecently covered how some hospitals are now requiring physicians to go in-network as a provision of their contracts. However, they also note this approach disadvantages physicians and shifts reimbursement negotiation power to insurers. Should hospitals take a similar approach with medical laboratory specialists, it could create similar concerns.

While surprise medical bills create added hardship for

patients and pose reputational and reimbursement concerns for clinical laboratories

and healthcare providers, creating regulations that establish effective

protections while also protecting the financials of service providers continues

to prove difficult.

Speaking with Modern Healthcare, Dan Sacco, Vice President for Strategic Affairs and Payer Relations at Boca Raton Regional Hospital, summarized concerns concisely, saying, “We’re trying to protect [consumers], but we’re also trying to be reasonable business partners as well.”

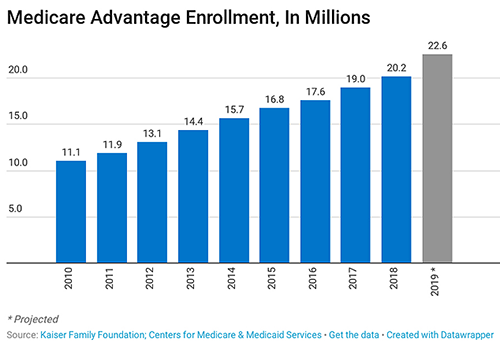

Popularity of Medicare Advantage Plans fuels influx of new companies into the marketplace with anticipated enrollment of more than 22.6 million beneficiaries, or more than one-third of Medicare-eligible consumers

Continuing enrollment growth in Medicare Advantage plans is expected in 2019 and beyond. The projections are for double-digit percentage increases in Medicare Advantage enrollees. This is not auspicious for clinical laboratories and anatomic pathology groups because it means a shrinking proportion of Medicare beneficiaries remain in the Part B program.

Whereas any medical laboratory can provide services for any Medicare Part B beneficiary, that is not true for beneficiaries enrolled in Medicare Advantage plans. That’s because private health insurers operating Medicare Advantage plans typically contract with national lab companies while narrowing their lab networks, thereby limiting access to these patients by independent community laboratories, hospital lab outreach programs, and pathology groups.

Enrollment in Medicare Advantage is expected to reach record totals in 2019. More than 22.6 million new Medicare beneficiaries are anticipated, with 14 new private companies offering plans, Kaiser Health News (KHN) reports. As enrollment shifts from traditional Medicare to Medicare Advantage the health of regional clinical laboratories can suffer, as smaller labs lose access to beneficiaries.

Enrollment in

Medicare Advantage Plans Increases, Despite Cut in Funding

Because Medicare Advantage penetration varies across counties and states, some local laboratories may experience less of an impact from the growing popularity of Medicare Advantage plans than others. According to the Kaiser Family Foundation (KFF), Medicare Advantage plans attract less than 11% of eligible beneficiaries in Arkansas, Vermont and Wyoming. However, more than 41% of Medicare participants in Florida, Hawaii, Minnesota, and Oregon choose Medicare private health plans over Medicare Part B.

Although the Patient Protection and Affordable Care Act (ACA) cut federal funding to Medicare Advantage plans, the 2010 law ultimately did not cause insurers to exit states or leave the business altogether, as was predicted. Instead, enrollment in Medicare Advantage doubled to more than 22.6 million enrollees, growing from a quarter of Medicare beneficiaries to more than a third, between 2010 and 2019, KHN reported.

Bonus payments from the federal government to Medicare

Advantage plans that have quality ratings of four or more stars (on a one to five

scale) helped fuel the growth. Plans without ratings also are eligible for

bonus payments, which must be used to reduce cost-sharing or premiums or to

provide extra benefits.

Since 2010, enrollment in Medicare Advantage has doubled to more than 22.6 million enrollees, growing from a quarter of Medicare enrollees to more than one-third. This trend is not favorable to many clinical laboratories, as the private health insurers who operate Medicare Advantage plans often contract with the billion-dollar lab companies and exclude regional and independent medical laboratories as network providers. (Photo copyright: Kaiser Family Foundation, Centers for Medicare and Medicaid Services.)

“The Affordable Care Act did not kill Medicare Advantage, and the program looks poised to continue to grow quite rapidly,” Bill Frack, Managing Director with healthcare advisor L.E.K. Consulting, told KHN.

In total, 2,734 Medicare Advantage plans will be available nationwide to consumers in 2019, an 18% increase from 2018 (417 more plans). That’s the largest number available since 2009, KFF announced late last year in a report on the program’s growth. These numbers exclude employer or union-sponsored group plans and Special Needs Plans, which are only available to select populations.

The average Medicare beneficiary has access to 24 Medicare

Advantage plans in 2019, an increase from 21 last year and 19 from 2016-2017.

Profits Increase

While Premiums Decline

Medicare Advantage plans are attractive to seniors because

premiums, deductibles, and cost sharing typically are lower than government-run

Medicare Part B and because many plans include additional benefits such as vision,

dental, and prescription drug coverage and fitness programs.

In a press release, the Centers for Medicare and Medicaid Services (CMS) noted that the Medicare Advantage average monthly premium has continued to steadily decline, recording an estimated 6% drop in 2019 to $28, from an average of $29.81 in 2018. Nearly 83% of Medicare Advantage enrollees remaining in their current plan will have the same or lower premium in 2019. Approximately 46% of enrollees in their current plan will have a zero premium.

“The steps that the Trump Administration has taken to improve and drive competition in Medicare Advantage means more savings, more benefits and lower costs for seniors, CMS Administrator Seema Verma said in the press release. “[With the] popularity of programs, such as Medicare Advantage, and with the various new supplemental benefits and policy changes that have been adopted, we expect plan choices to be even more robust moving forward.” [Photo copyright: Centers for Medicare and Medicaid Services.)

Declining premiums, however, have not meant reduced profits

for Medicare Advantage plan administrators. Healthcare Finance recently reported

that UnitedHealth Group’s third-quarter earnings from operations grew $502

million, or 12.3%, year-over-year to $4.6 billion, with growth in the insurer’s

Medicare Advantage business claiming most of the credit for the higher numbers.

UnitedHealthcare’s Medicare Advantage plans served 525,000

more consumers year-over-year, with the purchase of a physician-owned Medicare

Advantage organization in Louisiana accounting for 65,000 of the total.

“These results reflect our businesses delivering increased value at an accelerating pace to society and the millions of people we serve—one person at a time,” David S. Wichmann, CEO of UnitedHealth Group, told Healthcare Finance.

While Medicare Advantage plan growth may be good news for insurers,

the outlook for anatomic pathology groups and medical laboratories is less

rosy. The proportion of Medicare beneficiaries enrolled in the Part B program

shrinks steadily. Meanwhile, payers’ increased reliance on narrow networks as a

way to rein in rising costs excludes many regional laboratories. Ultimately,

these developments threaten many in the clinical laboratory industry, not just

smaller laboratories, and underline the need for pathologists and clinical

laboratory managers to add recognized value to the medical testing services

they provide in their communities.

Despite the widespread adoption of electronic health record (EHR) systems and billions in government incentives, lack of interoperability still blocks potential benefits of digital health records, causing frustration among physicians, medical labs, and patients

Clinical laboratories and anatomic pathology groups understand the complexity of today’s electronic health record (EHR) systems. The ability to easily and securely transmit pathology test results and other diagnostic information among multiple providers was the entire point of shifting the nation’s healthcare industry from paper-based to digital health records. However, despite recent advances, true interoperability between disparate health networks remains elusive.

One major reason for the current situation is that multi-hospital health systems and health networks still use EHR systems from different vendors. This fact is well-known to the nation’s medical laboratories because they must spend money and resources to maintain electronic lab test ordering and resulting interfaces with all of these different EHRs.

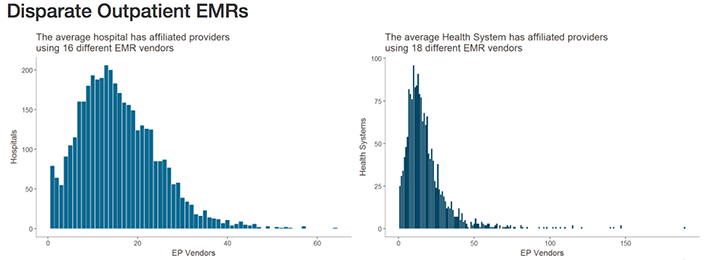

Healthcare IT News highlighted the scale of this problem in recent coverage. Citing data from the Healthcare Information and Management Systems Society (HIMSS) Logic database, they note that—when taking into account affiliated providers—the typical health network engages with as many as 18 different electronic medical record (EMR) vendors. Similarly, hospitals may be engaging with as many as 16 different EMR vendors.

The graphics above illustrates why interoperability is the most important hurdle facing healthcare today. Although the shift to digital is well underway, medical laboratories, physicians, and patients still struggle to communicate data between providers and access it in a universal or centralized manner. (Images copyright: Healthcare IT News.)

The lack of interoperability forces healthcare and diagnostics facilities to develop workarounds for locating, transmitting, receiving, and analyzing data. This simply compounds the problem.

Pressure from Technology Giants Fuels Push for Interoperability

According to HITECH Answers, the Centers for Medicare and Medicaid Services (CMS) has paid out more than $38-billion in EHR Incentive Program payments since April 2018.

Experts, however, point out that government incentives are only one part of the pressure vendors are seeing to improve interoperability.

“There needs to be a regulatory push here to play referee and determine what standards will be necessary,” Blain Newton, Executive Vice President, HIMSS Analytics, told Healthcare IT News. “But the [EHR] vendors are going to have to do it because of consumer demand, as things like Apple Health Records gain traction.”

Another solution, according to TechTarget, involves developing application programming interfaces (APIs) that allow tech companies and EHR vendors to achieve better interoperability by linking information in a structured manner, facilitating secure data transmission, and powering the next generation of apps that will bring interoperability ever closer to a reality.

TechTarget reported on how University of Utah Hospital’s five hospital/12 community clinic health network, and Intermountain Healthcare, also in Utah, successfully used APIs to develop customized interfaces and apps to improve accessibility and interoperability with their Epic and Cerner EHR systems.

Diagnostic Opportunities for Clinical Laboratories

As consumers gain increased access to their data and healthcare providers harness the current generation of third-party tools to streamline EHR use, vendors will continue to feel pressure to make interoperability a native feature of their EHR systems and reduce the need to rely on HIT teams for customization.

For pathology groups, medical laboratories, and other diagnosticians who interact with EHR systems daily, the impact of interoperability is clear. With the help of tech companies, and a shift in focus from government incentives programs, improved interoperability might soon offer innovative new uses for PHI in diagnosing and treating disease, while further improving the efficiency of clinical laboratories that face tightening budgets, reduced reimbursements, and greater competition.