Jan 22, 2018 | Laboratory Hiring & Human Resources, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology, Laboratory Testing, Management & Operations

Meanwhile, some insurance payers are dropping coverage for certain medical treatments they consider “unnecessary,” leaving hospitals and their medical laboratories to wonder if they will be reimbursed for the tests they perform

Hospital-based medical laboratories and anatomic pathologists are well aware that the emergency department (ED) in their hospital is their single largest customer and that reporting test results within required turn-around times (TATs) is a non-stop battle. Thus, it will not be a surprise to learn that EDs provide nearly half of all hospital-related medical care in the US. That’s what a study by the University of Maryland School of Medicine (UMSOM) reports.

The UMSOM researchers claim their study, which was published in the International Journal for Health Services (IJHS), is the first ever to quantify the contribution EDs make to US healthcare. According to an UMSOM news release, they determined that 47.7% of all hospital-associated medical care between 1996 and 2010 was delivered by EDs.

Results Show EDs Critical to Healthcare Delivery

This a remarkable revelation. “I was stunned by the results,” David Marcozzi, MD, Associate Professor and Assistant Chief Medical Officer for Acute Care, UMSOM Department of Emergency Medicine, told Becker’s Hospital Review. Marcozzi led the study, which involved researchers from Thomas Jefferson University and other academic institutions.

“This research underscores the fact that emergency departments are critical to our nation’s healthcare delivery system,” he continued. “Patients seek care in emergency departments for many reasons. The data might suggest that emergency care provides the type of care that individuals actually want or need.”

As Becker’s Hospital Review explained, there were about 130-million visits to hospital EDs as compared to 101-million outpatient visits, and 39-million inpatient visits during 2010, the most recent year analyzed by UMSOM.

Quantifying the EDs Contribution to Healthcare

The researchers studied the role EDs play in caring for Americans, as compared to hospital outpatient and inpatient sectors. They were motivated, in part, by the apparent extra attention healthcare decision-makers pay to inpatient services and costs. As an emergency medicine and population health specialist, Marcozzi (who also works in the UM Medical Center Emergency Department) challenged that focal point.

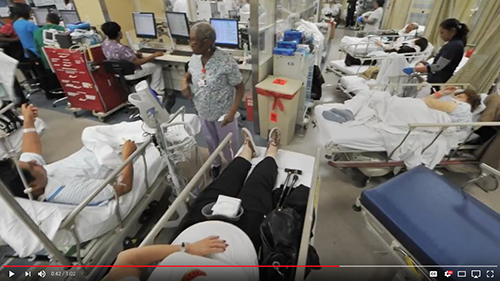

In the first study to quantify the contribution of emergency department care to overall US healthcare, researchers at the University of Maryland School of Medicine (UMSOM) have found that nearly half of all US hospital-associated medical care is delivered by emergency departments. In this video, David Marcozzi, MD, MHS-CL, FACEP, talks about why this is happening and what the ramifications are for healthcare delivery in the US. Click on image above to view video. (Video and caption copyright: University of Maryland School of Medicine.)

The researchers cited National Center for Health Statistics data suggesting just 12% of ED encounters led to hospitalizations. This seems to counter claims of up to 50% of all healthcare being delivered in EDs. However, the researchers note that EDs also serve the uninsured and poor, many of whom are not admitted to the hospital.

“Traditional approaches to assessing the health of populations focus on the use of primary care and the delivery of care through patient-centered [medical] homes, managed care resources, and accountable care organizations. The use of EDs has not been given much consideration in these models,” the authors wrote in their paper.

ED Visits Jump Nearly 44% over 14 Years

Researchers analyzed ED patient, outpatient, and inpatient data from these sources:

- National Hospital Ambulatory Medical Care Survey

- National Hospital Discharge Survey

- Electronic data files (sources of patient demographics and medical information) from commercial organizations, state data systems, hospitals, and hospital associations

They discovered that 3.5-billion healthcare encounters occurred over the 14-year period studied (1996 to 2010), representing a 43.7% increase in ED visits during that time.

During that period, ED utilization resulted in:

- 1.6-billion ED visits or 47.7%

- 1.3-billion outpatient visits or 37.6%

- 5.2-million hospital admissions or 14.8%

The UMSOM study also found EDs were increasingly being used by African Americans in the south and west and by Medicaid beneficiaries, Fierce Healthcare reported.

“When considering the isolated ED case mix, Medicaid as a course of payment showed a major increase in its contribution, shifting from 19.4% to 27.5% of all emergency care,” the researchers noted.

What’s needed, according to the study authors, are solutions to address non-urgent conditions often seen in EDs. However, they acknowledge, that the topic has drawn controversy.

Insurers Respond to Trend by Dropping Coverage of ‘Unnecessary’ ED Treatments

Some insurance companies on the hook for increasing ED costs have devised a novel approach to the increased cost—stop paying for it.

A Dark Daily e-briefing recently covered one such “solution” involving letters sent to Anthem Blue Cross and Blue Shield (BCBS) of Georgia members informing them that ED services deemed “unnecessary” by BCBS would no longer be paid. (See Dark Daily, “Anthem Blue Cross Blue Shield of Georgia Drops Coverage for Non-Emergency ER Visits; Medical Laboratories Could See Drop in ER Clinical Lab Test Orders,” July 14, 2017.)

These new guidelines, which created quite a stir in Georgia before they went into effect July 1, 2017, are mirrored at BCBS affiliates in New York, Missouri, and Kentucky, noted sources in the Dark Daily report.

Non-avoidable Healthcare Events and ‘Connecting the Care’

In apparent response to this trend, a study published in the International Journal for Quality in Health Care, found that just 3.3% of ED visits are actually “avoidable.”

“Despite a relentless campaign by the insurance industry to mislead policymakers and the public into believing that many ER visits are avoidable, the facts say otherwise,” stated Becky Parker, MD, President of the American College of Emergency Physicians (ACEP), in a news release.

UMSOM’s Marcozzi says the aim should be to “connect the care” delivered in EDs with other care offered by the healthcare system.

“Restricting EDs to patients classified as having critical illness does not seem a feasible or humanitarian option, as many individuals would not be able to find care elsewhere. In addition, many people do not have the knowledge to determine which symptoms indicate an emergency,” the researchers note.

Clinical Laboratories Can Download the UMSOM Full Study for Future Reference

At this point, it’s not clear how increasing ED costs and decreasing insurance payments will impact medical laboratories and anatomic pathology groups. Nevertheless, the UMSOM study is a good resource. ED volume and test orders will likely increase as more people go to EDs for treatment.

As a special to Dark Daily readers, Sage Publications is granting full access to UMSOM’s study through March 31, 2018. After that date, only the abstract will be available to non-IJHS subscribers. Click here to reach the full study article or place this URL into your browser: http://journals.sagepub.com/stoken/default+domain/JG8RNXfhAf7fuhFRIUIV/full.

—Donna Marie Pocius

Related Information:

Trends in the Contribution of Emergency Departments to the Provision of Hospital-Associated Health Care in the USA

University of Maryland School of Medicine Study Finds That Nearly Half of U.S. Hospital-Associated Medical Care Comes from Emergency Rooms

Nearly 50% of US Medical Care Occurs in EDs

ERs Provide Nearly Half Medical Care in U.S., Study Finds

Avoid Emergency Department Visits: A Starting Point

Only 3.3% of ER Visits Are Avoidable

Anthem Blue Cross Blue Shield of Georgia Drops Coverage for Non-Emergency ER Visits; Medical Laboratories Could See Drop in ER Clinical Lab Test Orders

Jan 11, 2018 | Laboratory Hiring & Human Resources, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology, Laboratory Testing, Management & Operations

At institutions such as University of Texas Medical Branch, Galveston, and Vanderbilt University Medical Center, pathologists are using diagnostic management teams to improve patient outcomes while lowering the medical costs

Diagnostic Management Teams are a hot concept within the medical laboratory profession. In fact, a new annual DMT conference in Galveston, Texas, is the fastest-growing event in the clinical laboratory industry. This year’s Diagnostic Management Team Conference will take place on February 6-7, 2018, and is produced by the Department of Pathology at the University of Texas Medical Branch (UTMB) in Galveston.

In simplest terms, a diagnostic management team (DMT) is described by pathologist Michael Laposata, MD, PhD, as “involving a group of experts who meet daily and focus on the correct selection of laboratory tests and the interpretation of complex test results in a specific clinical field. Typically, DMTs are led by pathologists focusing on the diagnosis of a specific group of diseases, along with physicians and other lab experts involved in the disease or health condition that is the focus of the DMT.”

How Pathologists Use Diagnostic Management Teams

“What differentiates a DMT are two changes from the classic diagnostic pathway,” continued Laposata. “First, the ordering physician gets assistance in selecting the correct tests. This can be done in several ways, such as creating expert-driven algorithms that are updated regularly to manage utilization of laboratory tests and dramatically minimize overuse and underuse. Use of such algorithms with reflex testing makes it easy for treating healthcare providers to order the right tests and only the right tests.

“The second key difference in this new diagnostic pathway is that, within the DMT’s specific clinical context, an expert-driven, patient-specific interpretation of the test results in a specific clinical context is generated by the members of the DMT,” he said. “This requires the knowledge of a true expert—not someone who may have a general idea about the meaning of a particular laboratory test result—and the participation of someone to help that expert search the medical record for relevant data to be included in the interpretation.

DMTs Typically Organized to Support Specific Diseases or Health Conditions

He pointed out that the DMT has a rather simple organization. There is a front-end and a back-end. The front-end starts when “physicians order tests by requesting evaluation of an abnormal screening test or clinical sign or symptom,” explained Laposata. “Upon receiving that request, the expert physician and colleagues in the DMT then synthesize the clinical and laboratory data and provide a narrative interpretation based upon medical evidence. This happens not only when specifically requested by the referring physician, but also for every case handled by the DMT.”

Diagnostic Management Teams are making significant contributions at the University of Texas Medical Branch (UTMB), Galveston. Pictured above, the members of UTMB’s coagulation DMT are (L-R): Jack Alperin, MD; Michael Laposata, MD; Aristides Koutrouvelis, MD; Camila Simoes, MD; Chad Botz, MD; Aaron Wyble, MD: and Jacob Wooldridge, MD. (Photo copyright: University of Texas Medical Branch, Galveston.)

The back-end of the process involves the DMT conducting an “expert-driven, patient-specific interpretation of the test results in a specific clinical context.” Here is where the participating clinical experts—supplemented by staff who conduct an informed search of the medical record to identify and collect data relevant to the diagnosis—sift through this much richer quantity of information to develop the diagnosis.

Overworked Physicians Value the Expertise, Diagnostic Accuracy of DMTs

Laposata points out that individual physicians who already may be overworked in their daily routines generally welcome the help of DMT experts who are up-to-date on the current literature, and who have decades of experience in these diseases and health conditions. He likes to point out that, in coagulation alone, a physician could have as many as 60 to 90 tests that can be ordered. He also notes that typical primary care physicians, for example, are generally not experts in selecting the best coagulation test to order for every group of symptoms, nor do they know how to order the most appropriate reflexive test to continue the diagnostic pathway.

Knowing how to interpret the results of the 60 to 90 different coagulation tests is equally challenging to most physicians.

Over the course of his career, Laposata has signed out more than 50,000 cases in the field of coagulation. “Every positive case that identified a diagnosis resulted in an earlier and more accurate diagnosis,” stated Laposata. “Every case negative for coagulopathy allowed the treating healthcare provider to focus on a diagnosis other than one related to bleeding and thrombosis.”

Using Clinical Laboratory Data to Improve Patient Outcomes, Reduce Costs

There are other reasons why a growing number of medical lab administrators and clinical pathologists believe that DMTs are the right solution at the right time. One reason is the steady reduction in reimbursement from Medicare and private payers. Another is the trend to measure and publish the quality metrics of hospitals and individual physicians.

There are ever more quality metrics that include diagnostic accuracy and total cost per healthcare encounter. Diagnostic Management Teams are proven to improve diagnostic accuracy and ensure the patient gets the right therapy faster. Both of these benefits contribute to substantial reductions in the cost per healthcare encounter.

Pathologists and clinical laboratory professionals interested in learning more about diagnostic management teams have two opportunities.

At the Galveston Island Convention Center on Feb. 6 -7, 2018, the second annual Diagnostic Management Team Conference will take place. Last year, several hundred-people attended. Information can be found at: http://www.dmtconference.com/.

Special Webinar on Diagnostic Management Teams on January 17

For those interested in learning via webinar, Dark Daily is presenting Laposata and his colleagues in a special session on Wednesday, Jan. 17 at 1:00 PM EASTERN. It is titled, “Using Diagnostic Management Teams to Add Value with Clinical Laboratory Tests and Pathologists’ Expertise.”

During this valuable webinar, you’ll hear from three experts. First to speak will be Michael Laposata, MD, PhD. He will provide you with a detailed overview of DMTs, including:

- How to assemble the right team;

- How to engage with referring physicians; and,

- How to work through individual cases.

Laposata will introduce you to the structure and organization of effective diagnostic management teams, organized around a specific disease or health condition and made up of pathologists, other lab scientists, and physicians who are expert in their particular clinical field. The objective of the DMT is to meet daily with the goal of coming up with faster, more accurate diagnoses in support of a patient’s care team.

Experience from a Diagnostic Management Team Focused on the Liver

Next to speak will be Heather Stevenson-Lerner, MD, PhD, a liver and transplantation pathologist and Assistant Professor, Department of Pathology, UTMB. She will discuss a DMT organized around diseases of the liver. This is a useful, step-by-step description of an effective DMT, illustrated with case studies that demonstrate how diagnostic management teams can make a positive and substantial contribution to improving individual patient outcomes.

The webinar’s third presenter is Christopher Zahner, MD, a resident pathologist at UTMB. He will share how to pull together all the information needed to support DMT interpretations. From the electronic health record (EHR) system to other overlooked sources of useful data, Zahner will explain the most productive ways to assemble any information that will be useful to the diagnostic management team and that will make a positive difference in patient care.

To register for the webinar and see details about the topics to be discussed, use this link (or copy and paste this URL into your browser: https://ddaily.wpengine.com/webinar/using-diagnostic-management-teams-to-add-value-with-clinical-laboratory-tests-and-pathologists-expertise).

This is an essential webinar for any pathologist or lab manager wanting to put the lab front and center in contributing clinical value in ways that directly improve patient outcomes while reducing medical costs. With hospital lab budgets shrinking and fee-for-service payments being slashed, the time is right for your lab team to consider how organizing diagnostic management teams can be the perfect vehicle to demonstrate why clinical lab tests and expertise can be a diagnostic game-changer within your hospital or health system.

And don’t forget, your participation in this webinar can be the foundation for a highly-successful effort to collaborate with physicians and clinical services, to the benefit of both the parent hospital and individual patients. That makes this webinar the smartest investment you can make for crafting your lab’s test utilization and added-value programs in support of clinical care.

—Michael McBride

Related Information:

Webinar: Using Diagnostic Management Teams to Add Value with Clinical Laboratory Tests and Pathologists’ Expertise

Pathologist Michael LaPosata, MD, Delivers the Message about Diagnostic Management Teams and Clinical Laboratory Testing to Attendees at Arizona Meeting

Dec 15, 2017 | Instruments & Equipment, Laboratory Hiring & Human Resources, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology, Laboratory Testing, Management & Operations

As the still-developing pathology profession in China struggles to meet demand, 3rd-party medical laboratory groups, and university/industry arrangements, find opportunities to fill the needs of China’s hospitals

China is currently facing a severe shortage of anatomic pathologists, which blocks patients’ access to quality care. The relatively small number of pathologists are often overworked, even as more patients want access to specialty care for illnesses. Some hospitals in China do not even have pathologists on staff. Thus, they rely on understaffed anatomic pathology departments at other facilities, or they use imaging only for diagnoses.

To serve a population of 1.4 billion people, China has only 29,000 hospitals with seven million beds. Among the healthcare providers, there just 20,000 licensed pathologists, according to the Chinese Pathologist Association. By contrast, recent statistics show that the United States has a population of 326 million people with approximately 18,000 actively practicing pathologists and 5,815 registered hospitals with 898,000 beds.

The largest pathology department in China is at Fudan University Shanghai Cancer Center (FUSCC), a hospital with 1,259 beds in operation and 50 pathologists on staff. News accounts say those pathologists are expected to process 40,000 cases this year, surpassing their 2016 workload by 5,000 cases. The FUSCC pathologists are supported by a small number of supplemental personnel, which include assistants, technicians, and visiting clinicians.

Qifeng Wang, a pathologist at FUSCC, indicated that most leading hospitals in China with average or above-average pathology staffing are experiencing similar barriers as FUSCC. Large hospitals, such as:

· Cancer Hospital at the Chinese Academy of Medical Sciences;

· Beijing Cancer Hospital;

· Peking Union Medical College Hospital;

· West China Hospital; and

· First Affiliated Hospital of Sun Yat-sen University also deal with similar staffing shortages and excessive workloads for their pathology departments.

“The diagnostic skill level at FUSCC is not that different from that in the U.S.,” Wang told Global HealthCare Insights (GHI). He added, however, that the competent skill level of their staffers is not sufficient to handle the internal workload at FUSCC plus the additional workload referred to them from other facilities.

Though not at the top of the list, as the graphic above illustrates, China is preceded only by Uganda, Sudan, and Malaysia for the number of patients per anatomic pathologist. China has approximately one pathologist per 74,000 people. By contrast, the United States has one pathologist for every 19,000 people. Studies indicate that, globally, the number of pathologists each year is shrinking. (Image copyright: Clinical Laboratory Products)

Patients Forced to Migrate to Receive Diagnoses

Because there are so few pathologists in the vast, heavily-populated country, many Chinese patients travel to major cities to increase their chances of obtaining reliable diagnosis and care, which further overwhelms the system.

The 1,530-bed Yunnan Cancer Hospital in the western city of Kunming handles more than 4,000 cases forwarded to them from other institutions annually. The 14 pathologists at the center also sometimes travel to rural communities to provide anatomic pathology services.

“It’s the complex cases that make it hard to keep up with our workload” said Yonglin Wang, an anatomic pathologist at the Yunnan Cancer Hospital, in the GHI article. The pathologists at Yunnan often refer their more demanding cases to larger hospitals to ensure the best analysis and outcomes for the patients.

Workload, Low Pay, and Lawsuits Discourage Pathology Enrollments

A logical solution to the critical shortage of pathologists in China would be to increase the number of people choosing the profession. However, medical students in the country tend to steer clear of surgical pathology due to the excessive workload, lower pay and status, and the threat of lawsuits relating to improper diagnoses.

To address the demand, a private pathology industry is emerging in China. There are currently more than 300 private medical laboratories located throughout the country. The largest of these businesses is KingMed Diagnostics in Guangzhou. According to their website, the 3rd-party medical laboratory group focuses on medical testing, clinical trials, food and hygiene testing, and scientific research. They examine more than 4,000 pathology cases annually, concentrating on:

· Immunohistochemistry;

· Specialized staining; and,

· Ultrastructural and molecular pathological diagnosis.

American Colleges Partnering with Chinese Laboratory Groups

Organizations from other countries, including the United States, also are entering the pathology industry in China.

In 2014, the UCLA Department of Pathology and Laboratory Medicine partnered with Chinese firm Centre Testing International Corporation (CTI) to operate a clinical laboratory in Shanghai. In the endeavor, pathologists from UCLA trained Chinese lab specialists on the proper interpretation of tests at the 25,000 square-foot facility. (See The Dark Report, “UCLA, Centre to Open Lab In China to Offer High Quality Testing,” May 19, 2014.)

“Because pathology has a history of being undervalued in China, the country has a shortage of pathologists trained to diagnose and interpret complex test results in specialized fields of medicine,” said Scott Binder, MD, Senior Vice Chair at UCLA Health in a statement. “Our partnership gives CTI and UCLA the opportunity to save lives by changing that.”

“Our collaboration will offer the people of China oncology, pathology, and laboratory medicine services they can trust. Many of these services are not largely available in China and are needed by physicians and healthcare providers to accurately diagnose and treat their patients,” stated Dr. Sangem Hsu, President of CTI in the UCLA statement.

As the need for pathologists increases worldwide, many countries will struggle to fulfill the demand. This may create even more opportunities for enterprising medical laboratory organizations and anatomic pathology groups who have the wherewithal and determination to make a difference overseas.

—JP Schlingman

Related Information:

China Grapples with a Pathologist Shortage

In China, More Irate Patients Violently Attack Doctors over Wrong Diagnoses and Poor Healthcare

UCLA Launches Joint Venture with Chinese Firm to Open Sophisticated Lab in Shanghai

The Pathologist Workforce in the United States

UCLA, Centre to Open Lab In China to Offer High Quality Testing

Digital Pathology Gives Rise to Computational Pathology

Pathologist Workforce in the United States: I. Development of a Predictive Model to Examine Factors Influencing Supply

Anatomic Pathology in China Is a Booming Growth Industry

Digital Pathology Enables UCLA-China Lab Connection

Lab Testing, Pathology is Fast-growing in China

Nov 8, 2017 | Laboratory Hiring & Human Resources, Laboratory Instruments & Laboratory Equipment, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology, Laboratory Testing, Management & Operations

Increased use of telemedicine may create opportunities for clinical laboratories to deliver increased value to both physicians and nurses

Recent data shows widespread employer adoption of telehealth services may soon become a reality. However, studies also show virtual provider visits and other telemedicine technologies are unlikely to diminish the role of clinical laboratories in providing the data required for diagnosis and treatment decisions. Instead, laboratories and anatomic pathology groups will likely see changes in how samples are collected from patients using telemedicine and how medical laboratory test results are reported, as access to telemedicine grows.

A recent National Business Group on Health (NBGH) survey indicates that in 2018 “virtually all [large] employers (96%) will make telehealth services available in states where it is allowed.” The survey was conducted between May and June 2017, with 148 large employers participating.

Christine Smalley, Managing Director with consulting firm Claremont Hudson, divides telemedicine technology into three distinct segments:

1. Provider-to-provider;

2. Remote patient monitoring; and,

3. Patient-to-provider.

In an article she penned for MedCityNews, Smalley calls provider-to-provider telemedicine the “most evolved to-date” segment of the telehealth trend. She highlights ICU stroke care with remote consults and monitoring as an example of its “success,” and notes a large potential for growth in remote patient monitoring (RPM). Smalley cites a Berg Insight report that estimates 50-million patients will use remote monitored devices by 2021. However, Smalley also notes consumer acceptance of patient-to-provider telemedicine has fallen short of industry expectations.

While virtual office visits—where patients have access to physicians via telephone or videoconferencing—grab headlines, Smalley argues that “several factors” are hindering adoption.

“Reimbursement is not yet universal,” she notes. “But consumers are growing used to paying more out-of-pocket with high-deductible plans. Physicians have long resisted change in how they practice, and many remain lukewarm at best about telemedicine. It’s no coincidence that many of the innovations and pioneering models have come from outside of healthcare delivery … The barriers that loom the largest may likely be consumer awareness and trial.”

The Center for Connected Health Policy (CCHP) reports that 35 states have laws governing private payer reimbursement of telehealth, a number that has not changed since 2016. According to a CCHP press release, some state laws require reimbursement be equal to in-person visits, though not all laws mandate reimbursement.

Adopting Existing Retail Models to Promote Telemedicine to Patients

Smalley contends “smart marketing” will be needed to get consumers to leverage the telemedicine options that are becoming available to them. She says simply offering video or telephone visits is not enough. She encourages integrated delivery systems to take a page out of retailers’ playbooks.

“Look at how retailers, like Walmart, integrate online shopping and the store experience by offering side-by-side options supporting product delivery and in-store pickup. Telemedicine options ultimately need to be offered in a way that feels integrated and seamless to the health consumer,” she suggested, in her MedCityNews article. One example, she notes, would be providing an easy-to-navigate link to a virtual visit on a healthcare network’s urgent care webpage.

Click image above to see YouTube video

Healthcare Spending Could Increase Due to Telehealth

While health plans have zeroed in on telehealth as a way to drive down healthcare costs, a 2017 RAND Corp. study published in Health Affairs found virtual visits to physicians might not decrease spending, though access to care is improved.

“Instead of saving money by substitution [replacing more expensive visits to physician offices or EDs], direct-to-consumer telehealth may increase spending by new utilization [increasing the total number of patient visits],” a MedCityNews article suggests.

The RAND study examined commercial claims data of workers enrolled in the California Public Employees’ Retirement System (CalPERS) Blue Shield of California HMO (Health Maintenance Organization) from 2011-2013. Researchers focused on care received for acute respiratory infections. According to a RAND press release, net annual spending for acute respiratory infections increased by $45 per telehealth user.

“Given that direct-to-consumer telehealth is even more convenient than traveling to retail clinics, it may not be surprising that an even greater share of telehealth services represents new medical use,” noted Lori Uscher-Pines, PhD, a RAND Policy Researcher. “There may be a dose response with respect to convenience and use: the more convenient the location, the lower the threshold for seeking care and the greater the use of medical services.”

Telehealth in Clinical Laboratories

Will telehealth services offered by hospital networks and healthcare providers impact clinical laboratories? While a physical visit is still required for drawing blood, collecting urine, or performing pathology testing, interpretive digital pathology, such as Whole Slide Imaging (AKA, Virtual Slide), does enable pathologists to provided distance interpretation services of blood tests to remote and/or resource deficient areas of the world, as Dark Daily reported in past e-briefings. This could become a substantial revenue stream in the future if telepathology’s global popularity continues to rise.

—Andrea Downing Peck

Related Information:

Telemedicine Is on the Rise, Including for Labs

Large U.S. Employers Project Health Care Benefit Costs to Surpass $14,000 per Employee in 2018, National Business Group on Health Survey Finds

Large Employers’ 2018 Health Care Strategy and Plan Design Survey

Take a Lesson from Retail to Improve Patient Adoption

mHealth and Home Monitoring

Direct-to-Consumer Telehealth Prompts New Use of Medical Services; Not Likely to Decrease Health Spending

State Telehealth Laws and Reimbursement Policies, April 2017

CCHP Releases Fifth Edition of 50 State Telehealth Lawns and Reimbursement Policies Report

Almost All Large Employers Plan to Offer Telehealth in 2018, but Will Employees Use It?

Direct-to-Consumer Telehealth May Increase Access to Care but Does Not Decrease Spending

International Telemedicine Gains Momentum, Opening New Markets for Pathologists and Other Specialists

‘Nighthawk’ Radiology Services Expand to Hospital Pharmacies: Could Pathology Laboratories Be Next?

From Micro-hospitals to Mobile ERs: New Models of Healthcare Create Challenges and Opportunities for Pathologists and Medical Laboratories

Oct 2, 2017 | Laboratory Hiring & Human Resources, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology, Laboratory Testing, Management & Operations

Research conducted by Kalorama suggests the popularity of retail clinics represents a trend towards newer healthcare models that challenge existing models of care, and which could severely impact hospitals, clinical laboratories, and pathology groups

In recent years, pathologists and medical laboratory managers have watched as retail clinics housed in drug and grocery stores became a go-to service for healthcare customers seeking relief from minor illnesses. However, to market research company Kalorama, retail clinics also are a “game-changer” that could pose a threat to healthcare providers if their growth remains unchecked.

At risk are health systems and office-based physicians, along with the clinical laboratories and pathology groups that serve them. This would happen if patients shy away from primary care doctors in favor of cheaper, faster, medical care. However, as retail clinics expand the services they provide, they also could become an important source of orders for certain types of medical laboratory tests.

Kalorama defines retail clinics as, “healthcare centers that provide basic and preventative care in a retail setting; excluded are crisis and acute care centers; urgent care centers; emergency facilities; and wellness centers.” According to Kalorama’s data, “in 2016, total US retail clinic sales are estimated at more than $1.4 billion, an increase of 20.3% per year from $518 million in 2010.”

This increased use of retail clinics is a mixed blessing. On one hand, easy accessibility, low-wait times, and flexibility combined with lower costs for basic care is a boon for certain patients. On the other hand, this emergent healthcare model requires that traditional healthcare facilities address the impact of retail clinics on traditional practices, patient care, and regulatory standards.

Here are five reasons why retail clinics could threaten traditional healthcare models:

Retail Clinics Disrupt the Normal Healthcare Delivery Environment

Retail clinics are designed for immediate treatment of symptoms and vaccinations, not in-depth examination or long-term healthcare relationships between physician and patient. However, because retail clinics are a convenient low-cost option for patients, they become direct competition for full-service. Why visit a primary care physician (PCP) when you can receive off-hour care at lower prices and with faster wait times?

Based on data from peer-reviewed journal Mayo Clinic Proceedings, the graph above illustrates the huge growth of retail clinics over just the past 10 years, which is expected to continue. (Image copyright: Accenture Consulting.)

There is a rising fear among PCPs that the quick fix of retail clinic services will translate into poorer overall health for patients who fail to establish permanent long-term healthcare connections. This fear is validated by an American Medical Association (AMA) report that states, “only 39% of retail clinic users report having an established relationship with a primary care physician, which contrasts to about 80% of the general population reporting such a relationship.”

Retail Clinics Increase Competition for Primary Care Practices

Rather than competing with emergency departments, retail clinics directly compete with primary care clinics, according to Kalorama and the AMA. Staffed primarily by nurse practitioners and physician assistants, retail clinics treat symptoms of acute and easily identifiable health issues. There is growing concern that this limits opportunity for patients to receive more comprehensive healthcare that includes identification and treatment of chronic diseases.

And though competition in the healthcare market is good, physicians worry that retail clinics may push smaller stand-alone clinics out of business. The Kalorama report explains that “ultimately, medical practices are businesses that rely upon a steady flow of [patients] for their success.” When primary care facilities close due to loss of patients, it can create immediate healthcare gaps in communities.

Retail Clinics Could Increase Strain on Medical Laboratories and Pathology Groups

Kalorama’s data shows that retail clinics could place strain on medical laboratories and pathology practices. The study notes, “retail clinics are becoming relatively large users of point-of-care (POC) tests, clinical chemistry, and immunoassay laboratory tests and vaccines.” Kalorama’s report states, “the combined sales of these three types of products to retail clinics reached $240 million” in 2015, reflecting a 26% per year growth in testing since 2010. Projections from Kalorama suggest further increases in retail clinic test ordering in years to come.

The Clinical Laboratory Improvement Amendments (CLIA) advisory boards, the US Food and Drug Administration (FDA), and the Commission on Office Laboratory Accreditation (COLA) all have expressed concerns about the rise of retail clinic testing. COLA’s 2017 Spring Newsletter states that the increased use of retail clinics could lead to unnecessary testing, and increasing use of “non-laboratory personnel for laboratory testing.”

The COLA newsletter also warns that pathologists and clinical laboratory managers “should expect to see, over time, a steady increase in the menu of diagnostic testing offered by retail clinics.” COLA suggests that pathologists and laboratory scientists will experience increased demand from retail clinics for their services and expertise, but that because retail clinics often require high-volume, fast-paced testing without the benefit of full clinical laboratories (both in terms of staff and equipment) there is potential for retail clinic testing to fall short of industry standards.

Retail Clinics Fragment Health Records

According to an article in AMA Wire, the AMA House of Delegates (HOD) established guidelines for retail clinics that focus on continuity of medical records and the safeguarding of patient care. The guidelines state that retail clinics “must produce patient visit summaries that are transferred to the appropriate physicians and other healthcare providers in a meaningful format that prominently highlights salient patient information.” The fear, according to the AMA, is that the fragmenting of medical records may bring harm to patients via miscommunication that undermines patient-physician relationships and complicates oversight in treatment plans.

The Kalorama report echoes this sentiment. It states that physicians often take a negative view of retail clinics because of the lack of communication between retail clinics and primary care practices, citing a lack of cooperation or “unwillingness or inability on the part of convenience clinics to share medical information about patients with primary care providers.”

Retail Clinics Are Expanding Their Reach

Despite the fact that the AMA Council on Medical Services 2017 report on delivery reform recommends that retail clinics limit the scope of their care, expansion of retail clinic services has gone unchecked in many areas according to the Kalorama report. AMA policy states that retail clinics must have a “well-defined and limited scope of clinical services,” and the AMA’s 2017 guidelines state that “retail health clinics should neither expand their scope of services beyond minor acute illnesses … nor expand their scope of services to include infusions or injections.”

As retail clinics open around the country and expand their offerings there is a call for increased regulation of retail clinics to check that growth. COLA states that retail clinics are positioning themselves to play a major role in the delivery of primary care services. And the Kalorama report suggests that the trend towards retail clinic use will continue to rise, creating both challenges and opportunities for providers, clinical laboratories, pathologists, and healthcare policy makers who will be required to address the disruption to their businesses.

-Amanda Warren

Related Information:

Retail Clinics 2017: The Game-Changer in Healthcare

Report 7 of The Council on Medical Service: Retail Health Clinics

COLA’s Insights Spring 2017: The Rise of Retail Medicine

The Advance of the Retail Health Clinic Market: The Liability Risk Physicians May Potentially Face When Supervising or Collaborating with Other Professionals

Primary Care Practice Response to Retail Clinics

Retail Clinics are Poised to Offer More Health Services, Participate in ACOS, and Offer Expanded Menu of Clinical Pathology Laboratory Tests

Retail Clinics Continue to Shape Local Healthcare Markets

More Medical Laboratory Testing Expected as Retail Clinics Change Delivery of Routine Healthcare Services

Top-5 Diagnostics Trends Identified by Kalorama Will Impact In Vitro Diagnostics Manufacturers, Medical Laboratories in 2017

UnitedHealth’s Plans to Build More MedExpress Urgent Care Centers Is a Sign of Strong Consumer Demand and Could Be an Opportunity for Clinical Laboratories

Sep 8, 2017 | Laboratory Hiring & Human Resources, Laboratory Management and Operations, Laboratory News, Laboratory Operations, Laboratory Pathology

Gen Z values differ from previous generations’ values and medical laboratory managers should know in advance how members of this generation are likely to view their new workplaces

Medical laboratories managers and pathology group stakeholders have long been concerned about the looming retirement of Baby Boomers working in America’s clinical laboratories. With more and more members of this age group leaving the workforce, and with the following Gen X and Gen Y workers moving into positions vacated by Boomers, the next generation of workers—Generation Z (Gen Z)—is arriving to fill the gap.

This newest, youngest generation brings unique attributes and values to the clinical laboratory industry. Laboratory managers, pathologists, and business leaders need to understand those characteristics to work with them effectively.

Gen Z Values Reflect the Turbulent Times We Live In

With the addition of this newest age group in corporate America, there are now four distinct generations simultaneously working in the marketplace:

1. Baby Boomers (born early- to mid-1940s to early-1960s;

2. Generation X (born mid-1960s to early-1980s);

3. Generation Y (Millennials: born mid-1980s to early-1990s); and

4. Generation Z (Centennials: born mid-1990s to the mid-2000s).

A poll conducted by Ernst and Young LLP (EY) of London for the US Oil and Gas industry found that members of Gen Z have “fairly traditional” career priorities, however their values have been shaped by the nation’s struggles.

“When asked which three considerations are the most important in selecting a future career, both Millennials and Generation Z, as whole, prioritized salary (56%), good work-life balance (49%), job stability (37%), and on-the-job happiness (37%),” the EY survey reported.

Even though they are often clumped together with Millennials (Gen Y), recent research shows that the two generations are vastly different.

“Gen Z employees bring unique values, expectations, and perspectives to their jobs,” Paul McDonald, Senior Executive Director at staffing firm Robert Half, stated in a news release. “They’ve grown up in economically turbulent times, and many of their characteristics and motivations reflect that.”

Move over Baby Boomers! You no longer are the largest proportion of the population of the United States. According to the US Census Bureau, Generation Z (AKA, iGen and Post Millennials) make up about 25% of the US population or approximately 70-million people. However, it is estimated that by 2021, Gen Z will total 40% of all consumers in the US and account for one-fifth of the workforce. This youngest generation is now entering the clinical laboratory workforce in growing numbers. (Graphic copyright: Oklahoma Minerals.)

Though Millennials represent the largest portion of the workforce in America, Gen Z is the largest population of people overall and it’s growing. The oldest members will have reached the age of 21 in 2016-2017. Many will be graduating from college and seeking employment opportunities.

Gen Z Members are Technically Savvy; Seek Job Security/Stability

Members of Gen Z are familiar and fluent with computers, technology, and the Web. Therefore, business websites and social media presence are things they will examine when researching companies for job opportunities. Living in a world of perpetual updates and real-time communications makes them quick at processing information. Centennials also tend to be first-rate multitaskers, capable of focusing while numerous distractions occur around them.

“This group of professionals has grown up with technology available to them around the clock and is accustomed to constant learning,” McDonald stated in the Robert Half news release. “Companies with a solid understanding of this generation’s values and preferences will be well prepared to create work environments that attract a new generation of employees and maximize their potential.”

Stability and job security seem to be more important for Gen Z than it is for Gen Y. A recent study by staffing firm Adecco found that 70% of Gen Z prefer a stable work environment over one that offers passion, but little security.

“They saw their grandparents have to go back to work or their parents have struggles during the financial crisis,” noted McDonald in a MarketWatch article. “They want to work for companies long-term in their career.”

Where millennials are known to change jobs frequently, a 2015 study conducted by Robert Half found that centennials plan to work for only four companies in their entire careers. The same study also found that Generation Z prefer to work in business office environments instead of working remotely.

Centennials are also more interested in the values and fairness of their bosses and the company mission statements. Equal pay, promotions, and accolades need to be equitable across all genders, races, and other differences. Generation Z is also entrepreneurial and creative and they desire to interact with people in person.

“Be prepared to spend time with them face to face,” McDonald stated. “They want to be mentored and coached. If you coach them, you’re going to retain them.”

Gen Z Politics are Mixed

Generation Z also differs from Millennials in the political arena. In a New York Post column, Jeff Brauer, Professor of Political Science at Keystone College in La Plume, Penn., indicated that Generation Z is liberal on some issues while being conservative on other issues.

“Politically, Generation Z is liberal-moderate with social issues like support for marriage, equality, and civil rights, and moderate-conservative with fiscal and security issues,” Brauer stated. “While many are not connected to the two major parties and lean independent, Gen Z’s inclinations generally fit moderate Republicans.”

Brauer’s research found that members of Gen Z tend to value economic stability and security higher than the previous generation because they have grown up in an era peppered with terror threats, a shaky economy, and mass school shootings.

“This generation is different, and they are about to have a profound impact on commerce, politics, and trends,” stated Brauer in the NY Post column. “If politicians and business leaders aren’t paying attention yet, they better, because [Centennials] are about to change the world.”

As Generation Z comes of age, more of them will be working in the medical professions. Clinical laboratories and anatomic pathology groups would be well advised to prepare their businesses by adjusting leadership, adapting recruiting efforts, and shifting marketing to attract Centennials and remain relevant and successful in the future.

—JP Schlingman

Related Information:

The Secrets to Hiring and Managing Gen Z

Why the Generation After Millennials Will Vote Republican

Move Over Millennials, Members of Generation Z are Ready to Work

Eight Key Differences Between Gen Z and Millennials

Gen Z White Paper: The State of Gen Z 2017 National Research Study

What is Generation Z, and What Does It Want?

Gen Z Nothing Like Millennials, Prof Warns Liberals

Generation Z is Entering the Workforce: What does This Mean for Management?

Births: Provisional Data for 2016

The Six Living Generations in America

Wisdom of Hiring Across the Six Living Generations in America and the World

Generation Z: Five Surprising Insights