As mandatory screenings for private industry workers increases, some states launch free COVID-19 testing for state employees, while engaging medical laboratories to provide such testing

Amid the SARS-CoV-2 pandemic, welcoming employees back to work is not as simple as opening the company’s doors. Businesses based in some areas of the US and Canada are being required by state and provincial governments to conduct employee COVID-19 screenings. For clinical laboratories, the increase in mandatory screening programs could mean an expanding market for employee testing programs and opportunities for lab outreach programs.

But companies and medical laboratories may also face legal and regulatory risks as workplaces reopen and people return.

For example, how do clinical laboratory managers ensure their labs have the information they need to respond to new rules and regulations, and do employers have recourse should an employee receive a COVID-19 test report with an incorrect result?

Not COVID-19 Screening Can Lead to Fines, Imprisonment

Is there existence of “new or worsening symptoms,” such as fever or chills, difficulty breathing, and cough?

Has the employee travelled outside Canada in the past 14 days?

Has the employee had close contact with other confirmed or “probable” COVID-19 cases?

A “probable” case is “a person with symptoms compatible with COVID-19 AND in whom laboratory diagnosis of COVID-19 is inconclusive,” according to a blog post by Justin P’ng, Employment and Labor Lawyer/Associate at international law firm Fasken in Toronto.

“Employers [in Ontario] must now specifically comply with the requirements of the Screening Tool and to implement such screening at any physical workplaces it operates in the province,” P’ng wrote. “Failure to comply can lead to significant penalties, including potentially fines and imprisonment under the legislation.”

It is possible the new requirements may ease Ontario workers’ minds about heading back to work during the pandemic. A Canadian workforce survey of employers and employees during July 2020 by PricewaterhouseCoopers (PwC) Canada found:

Most employers (78%) expect a return to the workplace in 2020.

Just one in five employees indicated they want to go back to the workplace full-time.

Michigan Makes Remote Work Mandatory

In the US, state rules enforced by the Michigan Occupational Safety and Health Administration (MIOSHA) require employers—for infection prevention reasons—to establish remote work programs for employees, unless it is not feasible for employees to work away from the workplace.

“The employer shall create a policy prohibiting in-person work for employees to the extent that their work activities can feasibly be completed remotely,” MIOSHA said.

Similar to the Ontario law, Michigan employers are also required to establish COVID-19 screenings. The MIOSHA rules direct employers to “conduct a daily entry self-screening protocol for all employees or contractors entering the workplace, including, at a minimum, a questionnaire covering symptoms and suspected or confirmed exposure to people with possible COVID-19, together with, if possible, a temperature screening.”

Michigan employers not in compliance with the state’s requirements for office work may be fined up to $7,000 per violation, a McDonald Hopkins Insights article noted.

Furthermore, anti-retaliation law in Michigan prohibits employers from terminating or “retaliating against” employees who oppose violation of the law or report COVID-19 “health violations,” the McDonald Hopkins Insights article added.

However, Michigan businesses may have protection under the COVID-19 Response and Reopening Liability Assurance Act. The law states a “person who acts in compliance with all federal, state, and local statutes, rules, regulations, executive orders, and agency orders related to COVID-19 that had not been denied legal effect at the time of the conduct or risk that allegedly caused harm is immune from liability for a COVID-19 claim.”

The law defines a “person” as “an individual, partnership, corporation, association, governmental entity, or other legal entity, including, but not limited to, a school, a college or university, an institution of higher education, and a nonprofit charitable organization. Person includes an employee, agent, or independent contractor of the person, regardless of whether the individual is paid or an unpaid volunteer.”

New York Launches Free RT-PCR Tests for Transit Employees

Meanwhile, in New York, free COVID-19 tests are now available on a voluntary basis to 2,000 frontline employees of the Metropolitan Transit Authority, a news release states.

“Quality COVID-19 testing is critical to helping our nation’s frontline workers do their jobs as safely as possible,” Wendi Mader, Executive Director of Employer Population Health at Quest Diagnostics, said in the news release.

New Special Report Available on COVID-19 Employee Testing Programs

As the SARS-CoV-2 pandemic progresses, laws, regulations, and rules pertaining to COVID-19 employee testing and screening will likely continue to develop—and they will vary by area and by test type—making them a challenge to interpret, track, and ensure compliance.

This exclusive report offers guidance, best practices, and insights necessary to launch and operate high quality, compliant COVID-19 employee testing programs. Clinical laboratories and employers tasked with developing and maintaining coronavirus testing programs will gain critical insights and data from this invaluable special report. (Photo copyright: Dark Intelligence Group.)

Included in the report:

Ten regulatory essentials for launching a COVID-19 testing program

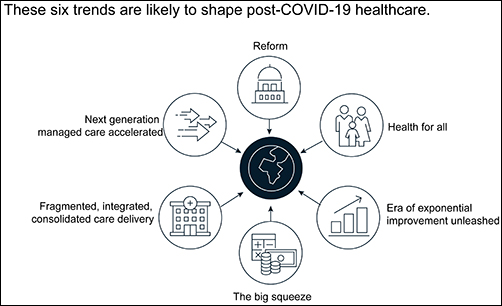

Clinical laboratory managers and pathology practice administrators should consider how these trends may affect their business and patients when planning for the future.

The McKinsey graphic above illustrates the “six trends that are likely to shape post-COVID-19 healthcare.” Clinical laboratories that support health networks struggling with any of these challenges should take steps to prepare for anticipated changes to healthcare delivery. (Graphic copyright: McKinsey and Company.)

1: Healthcare Reform

McKinsey identified three areas where the coronavirus pandemic may impact healthcare reform:

“COVID-19-era waivers that could become permanent.

“Actions that may be taken to strengthen the healthcare system to deal with pandemics.

“Reforms to address the COVID-19-induced crisis.”

McKinsey reports that “the Centers for Medicare and Medicaid Services has introduced more than 190 waivers since the beginning of March 2020.” These waivers can affect all aspects of healthcare, from clinical practice to reimbursement. Some of them, according to McKinsey, are “only relevant during the crisis (for example, the waiver of intensive care unit death reporting). A retrospective assessment of others (for example, expansion of telehealth access) could reveal beneficial innovation worth preserving.”

Several areas that McKinsey says are clearly ripe for reform include improving the resiliency of the healthcare system and the way the system is funded.

Public sector budgets are generally kept strictly separate, each with its own rules and policies that dictate operations. But in his article, “After COVID-19—Thinking Differently About Running the Health Care System,” published in JAMA Health Network, Stuart M. Butler, PhD, Senior Fellow in Economic Studies at the Brookings Institution, wrote, “The intensity of the COVID-19 pandemic … is forcing jurisdictions all across the country to find ways to be nimble so that multiple agencies can work together.”

Thus, McKinsey recommends, “Given the substantial shifts in relative market positioning among industry players that prior reforms have created, leaders would do well to plan ahead now.”

2: Better Access to Healthcare Services

Some people who develop COVID-19 are at far greater risk of hospitalization and death than others, including those who have:

Chronic health conditions, including obesity.

Mental and behavioral health challenges, such as substance abuse.

Unmet social needs, such as food or housing insecurity.

Poor access to healthcare.

McKinsey wrote that these “intersecting health and social conditions,” combined with certain races that have higher risk for severe complications, including Black, Indian, and Hispanic/Latino Americans, “correlated with poorer health outcomes.”

Value-based healthcare, telehealth, and greater attention to the social determinants of health may help address some of these issues, McKinsey notes, but the pandemic has shined a spotlight on how lack of care increases risk for certain populations during a public health crisis.

3: Era of Exponential Improvement Unleashed

Some of the trends that appear to be accelerating as a result of the pandemic are good news. McKinsey cites several benefits, including:

Improved understanding of patients.

Delivery of more convenient and individualized care.

$350-$410 billion in annual revenue by 2025.

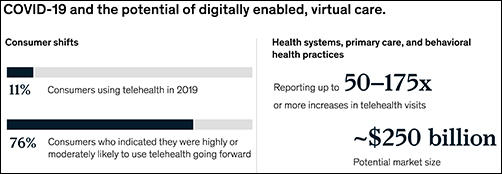

Through telehealth and other types of virtual care enabled by digital technology, “intuitive healthcare ecosystems” may arise and offer a more integrated experience for patients and their caregivers, McKinsey notes.

“While the pace of change in healthcare has lagged other industries in the past, potential for rapid improvement may accelerate due to COVID-19. An example is the exponential uptake of digitally enabled, virtual care,” McKinsey wrote. “Our analysis … showed that health systems, primary care, and behavioral health practices are reporting increases of more than 50–175 times in telehealth visits, and the potential market size for virtual care could reach around $250 billion.”

The graphic above is taken from the McKinsey and Co. report, which noted, “Proliferation of digitally enabled, virtual care could further contribute to the rise of personalized and intuitive healthcare ecosystems [that] have the potential to deliver an integrated experience to consumers, enhance productivity of providers, engage both formal and informal caregivers, and improve outcomes while lowering cost.” (Graphic copyright: McKinsey and Company.)

4: The Big Squeeze

The pandemic has caused an enormous outflow of cash from the healthcare system, and some experts don’t expect an injection of funding until 2022. “This outflow is expected to be primarily driven by coverage shifts out of employer-sponsored insurance and possible coverage reductions by employers as well as Medicaid rate pressures from states,” McKinsey states.

“We estimate that COVID-19 could depress healthcare industry earnings by between $35 billion and $75 billion compared with baseline expectations,” McKinsey predicted, adding, “Select high-growth segments will remain attractive (for example, virtual care, home health, software and platforms, specialty pharmacy) and will disproportionally drive growth. These high-growth areas are expected to increase more than 10% over the next five years, while other segments may stagnate or decline altogether.”

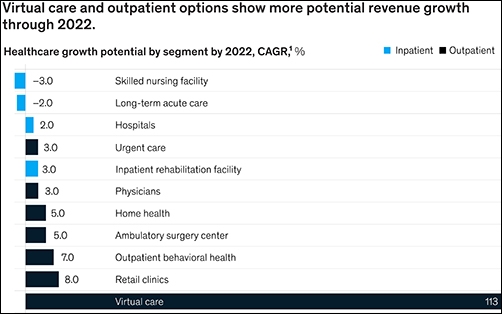

5: Fragmented, Integrated, Consolidated Care Delivery

McKinsey says, “The shift of care out of hospitals is not new but has been accelerated by COVID-19.” Rather than the hospital being the center of care delivery, patients are increasingly choosing to receive care at a range of sites across many healthcare ecosystems that are connected digitally and through analytics.

Early in the course of the pandemic, visits to ambulatory care facilities dropped nearly 60% by early April. But by mid-May, those visits were beginning to rebound.

In, “The Impact of the COVID-19 Pandemic on Outpatient Visits: A Rebound Emerges,” the Commonwealth Fund reported that “the relative decline in visits remains largest among surgical and procedural specialties and pediatrics” but is “smaller in other specialties, such as adult primary care and behavioral health.”

The McKinsey graphic above shows how “virtual care and outpatient options show more potential revenue growth through 2022.” Clinical laboratories that support those healthcare settings, especially ambulatory surgery, behavioral health, and retail clinics, should experience similar growth. (Graphic copyright: McKinsey and Company.)

6: Adoption of Next-Generation Managed Care Is Accelerating

How will COVID-19 affect the managed care industry? McKinsey says the “next generation” of managed care might use Medicare Advantage as a model.

“Payers pursuing the next generation of managed care model (through deep integration with care delivery) demonstrate better financial performance, capturing an additional 50 basis points of earnings before interest, taxes, depreciation, and amortization above expectation,” McKinsey noted, adding, “Employers and payers could consider fundamentally rethinking how employer-sponsored health coverage is structured. Learning from Medicare Advantage could provide inspiration for such a reimagination.”

What Should Clinical Laboratory Managers Do?

The McKinsey article concludes by stating, “While the challenges are numerous, leaders who seize the mindset that “disruptive change provides an opportunity to separate yourself from the pack” will build organizations meaningfully stronger than the ones they ran going into the crisis.”

The McKinsey article authors recommend that healthcare organizations take several proactive steps, including:

Launch a plan-ahead team.

Question your role and your future business model.

Prepare to transform your business.

Reimagine your organization to make faster decisions.

Take action to drive health equity.

Though the McKinsey and Company article covered healthcare in general, many of the authors’ observations and recommendations can apply to clinical laboratories and pathology groups as well and may be valuable in future planning.

Critical shortages in medical laboratory workers and supplies are yet to be offset by new applicants and improved supply chains. But there is cause for hope.

Medical laboratory scientists (aka, medical technologists) can be hard to find and retain under normal circumstances. During the current coronavirus pandemic, that’s becoming even more challenging. As demand for COVID-19 tests increases, clinical laboratories need more technologists and lab scientists with certifications, skills, and experience to perform these complex assays. But how can lab managers find, attract, and retain them?

The Johns Hopkins Coronavirus Resource Center reports that as of mid-October more than one million tests for SARS-CoV-2 were being performed daily in the US. And as flu season approaches, the pandemic appears to be intensifying. However, supply of lab technologists remains severely constrained, as it has been for a long time.

Still, qualified medical technologists (MT) and clinical laboratory scientists (CLS) are hard to find.

Demand for COVID Tests Exceeds Available Clinical Lab Applicants

“I can replace hardware and I can manage not having enough reagents, but I can’t easily replace a qualified [medical] technologist,” said David Grenache, PhD, Chief Scientific Officer at TriCore Reference Laboratories, Albuquerque, N.M., in the WSJ.

Another area where demand outstrips supply is California. Megan Crumpler, PhD, Laboratory Director, Orange County Public Health Laboratory, told the WSJ, “We are constantly scrambling for personnel, and right now we don’t have a good feel about being able to fill these vacancies, because we know there’s not a pool of applicants.”

Are Reductions in Academic Programs Responsible for Lack of Available Lab Workers?

Recent data from the US Bureau of Labor Statistics (BLS) show 337,800 clinical laboratory technologists and technicians employed by hospitals, public health, and commercial labs, with Job Outlook (projected percent change in employment) growing at 7% from 2019 to 2029. This, according to the BLS’ Occupational Outlook Handbook on Clinical Laboratory Technologists and Technicians, is “faster than average.”

“The average growth rate for all occupations is 4%,” the BLS notes.

Medical laboratories have the most staff vacancies in phlebotomy (13%) and the least openings in point-of-care (4%), according to an American Society for Clinical Pathology 2018 Vacancy Survey published in the American Journal of Clinical Pathology (AJCP).

Becker’s Hospital Review reported that “Labor shortages in [clinical] testing labs have existed for years due to factors including low recruitment, an aging workforce, and relatively low pay for [medical] lab technicians and technologists compared to that of other healthcare workers with similar education requirements.

“In 2019, the median annual salary for clinical laboratory technologists and technicians was $53,000, according to the US Bureau of Labor Statistics. The skills required for lab workers also are often specialized and not easily transferred from other fields.”

At the “root” of the problem, according to an article in Medical Technology Schools, is a decrease in available academic programs. Laboratory technologists require a Bachelor of Science (BS) degree and technicians need an associate degree or post-secondary certificate.

“(The programs) are expensive to offer, so when it comes to cuts and budgets, some of those cuts have been based on how much it costs to run them. That, and they may not have high enough enrollments,” said Lisa Cremeans, MMDS, CLS(NCA), MLS(ASCP), Clinical Assistant Professor at University of North Carolina at Chapel Hill, in the Medical Technology Schools article. (Photo copyright: University of North Carolina.)

AACC has called for federal funding of these programs, which now number 608, down from 720 programs for medical laboratory scientists in 1990.

“The pandemic has shone a spotlight on how crucial testing is to patient care. It also has revealed the weak points in our country’s [clinical laboratory] testing infrastructure, such as the fact that the US has allowed the number of laboratory training programs to diminish for years now,” said Grenache, who is also AACC President, in a news release.

Creative Staffing Strategies Clinical Labs Can Take Now

select “apply code” and complete the registration.

How Some Clinical Labs are Coping with Staff and Recruitment Challenges

The Arizona Chamber Business News reported that Sonora Quest Laboratories in Tempe earlier this year launched “Operation Catapult” to help with a 60,000 COVID-19 test increase in daily test orders. The strategy involved hiring 215 employees and securing tests with the help of partners:

Meanwhile, students in the UMass Lowell (UML) medical laboratory science (MLS) program, see brighter skies ahead.

“The job outlook even before COVID-19 was so amazing,” said Dannalee Watson, a UML MLS student, in a news release. “It’s like you’re figuring out a puzzle with your patient. Then, we help the doctor make decisions.”

Such enthusiasm is refreshing and reassuring. In the end, the SARS-CoV-2 pandemic and the resultant demand for clinical laboratory testing may call more students’ attention to careers in medical laboratories and actually help to solve the lab technologist/technician shortage. We can hope.

Though gene sequencing is touted as a key component of precision medicine, the medical value of direct-to-consumer testing has yet to show up in improved health outcomes, nor have clinical laboratories benefitted

In a recent example that the market for genetic genealogy testing may have peaked and the days of spectacular growth in the number of direct-to-consumer (DTC) genetic test orders and revenue is over, private-equity firm Blackstone—in a $4.7 billion deal—announced it will acquire a majority stake in Ancestry, which also does some clinical laboratory genetic testing as well.

Blackstone (NYSE:BX) acquired Ancestry of Lehi, Utah, one of the two largest genealogy testing companies (the other being 23andMe of Sunnyvale, Calif.), from a group of equity holders led by investment firms Silver Lake, GIC, Spectrum Equity, and Permira, noted a press release. GIC will retain a “significant minority stake” in Ancestry.

“We are very excited to partner with Ancestry and its management team. We believe Ancestry has significant runway for further growth as people of all ages and backgrounds become increasingly interested in learning more about their family histories and themselves,” David Kestnbaum, a Senior Managing Director at Blackstone, said in the press release. “We look forward to investing behind further data, functionality, and product development across Ancestry’s market leading platform to continue to provide a differentiated service.”

Is Genetic Testing for Genealogy Still a Growth Industry?

Ancestry is the global leader in digital family history services, operating in more than 30 countries with more than three million paying subscribers across its Ancestry online properties and more than $1 billion in annual revenue.

However, some experts say the road ahead may not be smooth for Ancestry or its major competitor, 23andMe.

“The business landscape fell off a cliff last year,” Laura Hercher, Director of Human Genetics Research at Sarah Lawrence College in New York, told STAT. “Fads pass,” she added.

Hercher points out that Ancestry has “this enormous database, which inherently has a lot of value hidden in it—potential energy. But they have not figured out how to get that information out in the way 23andMe has.”

23andMe’s pivot into medical research gained steam in 2018 when pharmaceutical giant GlaxoSmithKline (NYSE:GSK) purchased a $300 million stake in the company with the aim of using 23andMe’s resources to develop new medicines. That collaboration began bearing fruit earlier this year when GlaxoSmithKline started human trials of the first medicine (a cancer drug) to emerge from the partnership, STAT reported.

The public’s declining interest in at-home genealogy, however, has caused both companies to reduce staffing. 23andMe began the year by laying off about 100 employees—an estimated 14% of its workers—and Ancestry followed suit in February, letting go a similar number of employees, representing roughly 6% of its workforce.

According to MIT Technology Review, direct-to-consumer genetic genealogy testing reached its zenith in 2018 when consumers purchased as many DNA tests in one year as they had in all previous years combined, propelling total sales from Ancestry, 21andMe, and other DTC gene testing companies to roughly $26 million.

In 2019, CNBC reported that, market-wide, roughly 30 million tests had been sold across the globe. However, in recent years, sales have fallen short of expectations as the number of people willing to pay $99 to learn about their ancestry has dwindled. “I suspect those that are curious about this information are thinning out and there’s less people to go around to grow,” Greg Yap (above), Partner at Menlo Ventures, told CNBC. “I think there’s a broader issue, which is that the ultimate medical value is still really unproven,” Yap added. “There’s lots of research being done, but value for mass market consumer isn’t there yet, so it keeps a ceiling on the size of that market.” (Photo copyright: VentureBeat.)

Privacy Still a Concern

Ancestry has begun to insert itself into the genetic testing healthcare arena. In a press release, the company announced the launch of AncestryHealth, a $179 DNA testing kit that uses next generation sequencing (aka, high-throughput or massive parallel sequencing), aimed at providing adult consumers information on their inherited health risks.

However, as MedCity News points out, the sale to Blackstone has increased privacy concerns around the direct-to-consumer DNA testing market. Ancestry’s consumer privacy and data protections remain unchanged under the new ownership, but Alan Butler, Interim Executive Director at Electronic Privacy Information Center (EPIC), told MedCity News, “This is one example of a very troubling trend. It’s something regulatory agencies are not up to date to deal with. It’s one of the reasons we need comprehensive privacy law in the US.”

As genealogy companies such as 23andMe and Ancestry shift their focus from providing genetic histories to improving consumers’ health through genetic testing, clinical laboratories should be mindful of the logical next step, which is predicted to be genetic tests where the consumer collects the sample at home and the test is used to aid in diagnosing and treating patients.

This fourth edition of the annual event will be held virtually with free registration for pathologists and clinical laboratory professionals

In its fourth year, stakeholders in the clinical laboratory community have promoted thought leadership around the Lab Industry at the Project Santa Fe Foundation’s Clinical Lab 2.0 Workshop. Clinical Lab 2.0 (CL 2.0) which identifies new opportunities for medical labs to add value as the healthcare industry transitions from fee-for-service to value-based delivery models. But how does this concept apply during the era of COVID-19? That’s a key question participants will discuss at the 2020 Clinical Lab 2.0 Workshop, a virtual event scheduled for Oct. 26-27 with a focus on Population Health.

“This workshop will help all clinical laboratory leaders and pathologists to better understand, ‘How do we manage a pandemic, identifying high risk pool, where are the care gaps, and how do we better manage in the future proactively?’” said Khosrow Shotorbani, MBA, MT (ASCP), co-founder of the CL2.0 initiative and a regular speaker at the Executive War College, in an exclusive interview with Dark Daily. He is President and Executive Director of the Project Santa Fe Foundation, the organization that promotes the Clinical 2.0 Movement.

The coronavirus pandemic has “truly elevated the value of the clinical laboratory and diagnostics as one essential component of the care continuum,” he noted. “The value of the SARS-CoV-2 test became immense, globally, and the mantra became ‘test to trace to treat.’”

Project Santa Fe Foundation’s website defines Clinical Laboratory 2.0 as an effort to demonstrate “the power of longitudinal clinical lab data to proactively augment population health in a value-based healthcare environment.” The “goals are to improve the clinical outcomes of populations, help manage population risk, and reduce the overall cost of delivering healthcare,” the CL 2.0 website states.

“It’s about harnessing lab test results and other data that have predictive value and can help us proactively identify individuals that need care,” explained Shotorbani. “In the context of population health or value-based care, our labs potentially can utilize the power of this data to risk-stratify a population for which we are responsible or we can identify gaps in care.”

Clinical Lab 2.0 and the SARS-CoV-2 Pandemic

In the context of COVID-19, “Clinical Lab 2.0 argues that there is a hidden universe of value that can help augment what happens between COVID-19 testing and COVID-19 tracing to convert this reactive approach—meaning we wait for the person to get ill—versus considering who may be most at risk if they were to become infected so that our clinical laboratories can help caregivers create proactive isolation or quarantine strategies,” he added.

Shotorbani then explained how clinical laboratories have data about comorbidities such as diabetes, asthma, heart disease, and immunosuppression that are associated with more serious cases of COVID-19. “This clinical lab data can be harnessed, associated with demographic and risk data such as age and zip codes to help physicians and others identify patients who would be most at risk from a COVID-19 infection,” he noted.

“Historically, the primary focus of a clinical laboratory was very much on the clinical intervention, contacting the care manager physician, and identifying who’s at risk,” he said. But with COVID-19, Shotorbani sees opportunities to forge relationships with public health specialists to encourage what he describes as “consumer engagement.”

“As medical laboratory professionals, we must evolve to accommodate and support the needs of consumers as they take a more active role in their health,” he continued. “This is moving past simply providing lab test results, but to then be a useful diagnostic and therapeutic resource that helps consumers understand their health conditions and what the best next steps are to manage those conditions.”

Khosrow Shotorbani (above) is President, Executive Director, of the Project Santa Fe Foundation and one of the leaders of the Clinical Laboratory 2.0 movement. He is hopeful that the prominent role of medical laboratories in responding to the coronavirus pandemic will lead to an ongoing “seat at the table” in the higher echelons of healthcare organizations. In normal times, “we reside in basements, and we’re done when we release a result,” he said during an exclusive interview with Dark Daily. “COVID-19 was a kick in the rear to get us upstairs to the C-suite, because healthcare CEOs are under the gun to demonstrate more SARS-CoV-2 testing capacity.” Looking ahead, “we want to make sure that our clinical laboratories stay in that seat and design a future delivery model above and beyond COVID-19, maybe even help health systems, hospitals, and other providers drive their strategies.” (Photo copyright: Albuquerque Business First.)

“None of these are pathologists or come from the lab,” Shotorbani said. “They represent the C-suite and higher organization constituents. These are the healthcare executives who are dealing with their organization’s pain points. As clinical labs, we want to align ourselves to those organizational objectives.”

Pathologist Mark Fung, MD, PhD, will then present a CL 2.0 model for managing COVID-19 or other infectious disease pandemics, followed by a response from the other panelists. Fung is Vice Chair for Population Health in the Department of Pathology and Laboratory Medicine at the Larner College of Medicine at the University of Vermont. He is also on the Project Santa Fe Foundation (PSFF) board of directors.

“Lab 2.0 is a thought leadership organization,” Shotorbani said. “We are developing a template and abstract of this model of clinical laboratory services that other labs can follow while applying some of their own intuition as they make it operational.”

Day Two to the CL 2.0 workshop will feature case studies from the Henry Ford Health System in Detroit and Geisinger Health in Danville, Pa., followed by a discussion with eight PSFF directors. Then, Beth Bailey of TriCore Reference Laboratories in Albuquerque, N.M., will preside over a crowdsourcing session with participation from audience members.

Free Registration for Clinical Laboratories

This will be the first Clinical Lab 2.0 Workshop to be held virtually and registration this year will be free for members of the clinical laboratory community, Shotorbani said. In the past “there has been a hefty tuition to get into this because it’s a very high-touch workshop, especially for senior leaders. But given the critical topic that we’re facing, we felt it was important to waive the cost.”

The Fourth Annual Clinical Lab 2.0 Workshop is partnering this year with the American Society for Clinical Pathology (ASCP), which will provide the software platform for hosting the event, he said. In addition to the live conference sessions, registrants will have access to prerecorded presentations from past workshops. Content will be viewable for six months following the event.

Register for this critical event by clicking here, or by placing this URL in your browser (https://projectsantafefoundation.regfox.com/clinical-lab-20-workshop).

Financial losses for hospitals and health systems due to cancelled procedures and coronavirus expenses will lead to changes in healthcare delivery, operations, and clinical laboratory test ordering

COVID-19 is reshaping how people work, shop, and go to school. Is healthcare the next target of the coronavirus-induced transformation? According to two experts, the COVID-19 pandemic is pushing hospitals and health systems toward a “fundamental and likely sustained transformation,” which means clinical laboratories must be prepared to adapt to new provider needs and customer demands.

Burik and Fisher called attention to the staggering $50 billion-per-month loss for hospitals and health systems that was first revealed in an American Hospital Association (AHA) report published in May. The AHA report estimated a $200 billion loss from March 1, 2020, to June 30, 2020, due to increased COVID-19 expenses and cancelled elective and non-elective surgeries.

Adding to the financial carnage is the expectation that patient volumes will be slow to return. In “Hospitals Forecast Declining Revenues and Elective Procedure Volumes, Telehealth Adoption Struggles Due to COVID-19,” Burik said, “Healthcare has largely been insulated from previous economic disruptions, with capital spending more acutely affected than operations. But this time may be different since the COVID-19 crisis started with a one-time significant impact on operations that is not fully covered by federal funding.

“Providers face a long-term decrease in commercial payment, coupled with a need to boost caregiver and consumer-facing digital engagement, all during the highest unemployment rate the US has seen since the Great Depression,” he continued. “For organizations in certain locations, it may seem like business as usual. For many others, these issues and greater competition will demand more significant, material change.”

A Guidehouse analysis of a Healthcare Financial Management Association (HFMA) survey, suggests one-in-three provider executives expect to end 2020 with revenues at 15% below pre-pandemic levels, while one-in-five of them anticipate a 30% or greater drop in revenues. Government aid, Guidehouse noted, is likely to cover COVID-19-related costs for only 11% of survey respondents.

“The figures illustrate how the virus has hurled American medicine into unparalleled volatility. No one knows how long patients will continue to avoid getting elective care or how state restrictions and climbing unemployment will affect their decision making once they have the option,” Burik and Fisher wrote. “All of which leaves one thing for certain: Healthcare’s delivery, operations, and competitive dynamics are poised to undergo a fundamental and likely sustained transformation.”

As a result, the two experts predict these pandemic-related changes to emerge:

Payer-Provider Complexity on the Rise; Patients Will Struggle. As the pandemic has shown, elective services are key revenues for hospitals and health systems. But the pandemic also will leave insured patients struggling with high deductibles, while the number of newly uninsured will grow. Furthermore, upholding of the hospital price transparency ruling will add an unwelcomed spotlight on healthcare pricing and provider margins.

Best-in-Class Technology Will Be a Necessity, Not a Luxury. COVID-19 has been a boon for telehealth and digital health usage, creating what is likely to be a permanent expansion of virtual healthcare delivery. But only one-third of executives surveyed say their organizations currently have the infrastructure to support such a shift, which means investments in speech recognition software, patient information pop-up screens, and other infrastructure to smooth workflows will be needed.

“Through all the uncertainty COVID-19 has presented, one thing hospitals and health systems can be certain of is their business models will not return to what they were pre-pandemic,” Guidehouse Partner Chuck Peck, MD (above), a former health system CEO, said in a statement. “A comprehensive consumer-facing digital strategy built around telehealth will be a requirement for providers. Moreover, shifting hardware and physical assets to the cloud, and use of robotic process automation, has proven to be successful in improving back-office operations in other industries. Providers will need to follow suit.” Clinical laboratories and anatomic pathology groups should track these developments and respond appropriately to meet the changing needs of the hospitals and physicians they serve with diagnostic testing services. (Photo copyright: Athens Banner-Herald.)

The Tech Giants Are Coming. Both major retailers and technology stalwarts, such as Amazon, Walmart, and Walgreens, are entering the healthcare space. In January, Dark Daily reported on Amazon’s roll out of Amazon Care, a 24/7 virtual clinic, for its Seattle-based employees. Amazon (NASDAQ:AMZN) is adding to a healthcare portfolio that includes online pharmacy PillPack and joint-venture Haven Healthcare. Meanwhile, Walmart is offering $25 teeth cleaning and $30 checkups at its new Health Centers. Dark Daily covered this in an e-briefing in May, which also covered a new partnership between Walgreens and VillageMD to open up to 700 primary care clinics in 30 US cities in the next five years.

Work Location Changes Mean Construction Cost Reductions. According to Guidehouse’s analysis of the HFMA COVID-19 survey, one-in-five executives expect some jobs to remain virtual post-pandemic, leading to permanent changes in the amount of real estate needed for healthcare delivery. The need for a smaller real estate footprint could reduce capital expenditures and costs for hospitals and healthcare systems in the long term.

Consolidation is Coming. COVID-19-induced financial pressures will quickly reveal winners and losers and force further consolidation in the healthcare industry. “Resilient” healthcare systems are likely to be those with a 6% to 8% operating margins, providing the financial cushion necessary to innovate and reimagine healthcare post-pandemic.

Policy Will Get More Thoughtful and Data-Driven. COVID-19 reopening plans will force policymakers to craft thoughtful, data-driven approaches that will necessitate engagement with health system leaders. Such collaborations will be important not only during this current crisis, but also will provide a blueprint for policy coordination during any future pandemic.

As Burik and Fisher point out, hospitals and healthcare systems emerged from previous economic downturns mostly unscathed. However, the COVID-19 pandemic has proven the exception, leaving providers and health systems facing long-term decreases in commercial payments, while facing increased spending to bolster caregiver- and consumer-facing engagement.

“While situations may differ by market, it’s clear that the pre-pandemic status quo won’t work for most hospitals or health systems,” they wrote.

The message for clinical laboratory managers and surgical pathologists is clear. Patients may be permanently changing their decision-making process when considering elective surgery and selecting a provider, which will alter provider test ordering and lab revenues. Independent clinical laboratories, as well as medical labs operated by hospitals and health systems, must be prepared for the financial stresses that are likely coming.