Clinical laboratory information would be part of a “massive” transfer of data that may affect medical decision-making ‘to the detriment of consumers and healthcare providers’ the AHA stated in a letter to the DOJ

In yet another example of healthcare market concentration and consolidation where the big get bigger—sometimes at the expense of patients, physicians, and clinical laboratories—UnitedHealth Group (NYSE:UNH) announced in January the agreement that would enable it to acquire and merge Change Healthcare (NASDAQ:CHNG) with UnitedHealth Group’s (UHG’s) subsidiary OptumInsight. Many medical laboratories and anatomic pathology groups are clients of Change Healthcare.

Healthcare Finance reported that Nashville-based Change Healthcare “will join with OptumInsight to provide software and data analytics, technology-enabled services and research, advisory and revenue cycle management offerings, according to Optum parent company UnitedHealth Group.”

Change Healthcare says its Pathology Practice Revenue Cycle Management (RCM) services are used by more than 600 pathology and laboratory clients representing about 3,800 doctors. Perhaps this is why the American Hospital Association (AHA) has registered opposition to the proposed acquisition with the federal Department of Justice (DOJ).

In a letter to Richard Powers, JD, Acting Assistant Attorney General of the Antitrust Division at the DOJ, the AHA asked the DOJ to “conduct a thorough investigation of the proposed transaction because it threatens to reduce competition for the sale of healthcare information technology (HIT) services to hospitals and other healthcare providers, which could negatively impact consumers and healthcare providers.”

‘Substantial Antitrust Concerns’ Notes the AHA about the Merger

Optum, based in Eden Prairie, Minn., has approximately 5,000 hospitals and 300 health plans in its portfolio, according to Healthcare Finance. The health information technology and services firm offers data analytics, pharmacy care services, population health management, and more and is UHG’s fastest growing subsidiary, Modern Healthcare reported. UHG also owns UnitedHealthcare, the largest US health insurer.

When the AHA became troubled by UHG’s Optum/Change Healthcare plans, the national healthcare industry trade group asked the Antitrust Division of the DOJ to investigate the merger, noting in its letter to Powers that the merger “presents substantial antitrust concerns because the transaction agreement provides that the Parties will divest assets that generate hundreds of millions of dollars in revenue in order to obtain DOJ approval.”

Merger Could Affect Provider Reimbursement and Create Opportunity for Misuse of Patient Data

In its March 17 letter to DOJ’s Richard Powers, the AHA urged review of the proposed merger for these overarching reasons:

Possible loss of competition for services such as RCM and health IT services.

Likely repercussions from combining “massive” Optum and Change Healthcare data sets, which could be misused.

The marriage of Optum’s and Change Healthcare’s private patient data, the AHA portends, could possibly lead to altered decisions on patient care and claims processing and denials, Healthcare Finance reported.

Analysts told Healthcare Dive the merger would “consolidate Optum’s dominance in the data analytics space.”

In the AHA letter to the DOJ, Melinda Reid Hatton, JD, AHA Vice President and General Counsel, wrote, “The proposed acquisition would produce a massive consolidation of competitively sensitive healthcare data and shift such data from Change Healthcare, a neutral third party, to Optum.”

She continued, “Post-merger, Optum will have strong financial incentives to use competitive payers’ data to inform its reimbursement rates and set its competitive clinical strategy, which will reduce competition among payers and harm hospitals and other providers.

“Optum’s proposed acquisition of Change Healthcare will reduce the competition between two similarly scaled competitors,” Hatton concluded.

In the letter the AHA sent to Richard Powers, JD, Acting Assistant Attorney General of the Antitrust Division at the DOJ, Melinda Reid Hatton, JD (above), AHA Vice President and General Counsel, wrote, “Because Optum’s parent, UHG, also owns the largest health insurance company—UnitedHealthcare—the combination of the Parties’ data sets would impact and likely distort decisions about patient care and claims processing and denials to the detriment of consumers and healthcare providers.” Much of this data would come from the clinical laboratories and pathology groups in those two company’s databases. (Photo copyright: American Hospital Association.)

Optum, Change Healthcare Say Their Goal is Better Outcomes

For their part, according to a UHG news release announcing the merger in January, Optum and Change Healthcare are intent on combining their technology and service companies for the purpose of improving “core clinical, administrative, and payment processes.”

“Optum and Change Healthcare share a vision for better health outcomes and experiences for everyone at lower cost,” an Optum spokesperson told Becker’s Hospital Review.

A UHG spokesperson told Healthcare Dive a separation of UnitedHealthcare and Optum businesses is in place.

The AHA’s letter acknowledged Optum’s inclusion of an “informational firewall,” but noted that it is not enough. “UHG has never demonstrated that firewalls are sufficiently robust to prevent sensitive and strategic information-sharing,” Hatton wrote.

The deal, which was originally expected to close in the second quarter of 2021, has a $13 billion valuation, Healthcare Dive reported.

How Might This Affect Clinical Laboratories?

For clinical laboratories and pathology groups, the proposed merger could introduce questions about UnitedHealthcare’s access to information about how labs bill different payers other than UnitedHealthcare.

Change Healthcare each year processes more than 87 million pathology and clinical laboratory procedures, for which it charges $4.4 billion, according to the company’s website. The services it provides are aimed at increasing clinical laboratory cash flow, patient revenue and billing, coding efficiency, and compliance, according to Change Healthcare.

Therefore, Change Healthcare—in serving labs and pathology groups—already has data about agreements on charges for tests and other prices labs have with different insurers, noted Robert Michel, Editor-in-Chief of Dark Daily and its sister publication The Dark Report.

“It’s only reasonable for lab leaders to be concerned—if this deal is made—about lab pricing and other information,” Michel said. “Could it be reviewed and possibly used by UnitedHealthcare to establish its own terms in its network contracts with clinical labs and pathology groups?”

Clinical laboratory leaders will want to monitor these events as DOJ receives more information and further examines the UHG Optum/Change Healthcare proposed merger. It will be interesting to see if opposition to the merger arises from other healthcare associations and professional groups.

Consolidation of hospitals and health systems means consolidated medical laboratory services as well, and that impacts laboratory revenue and staff

Though COVID-19 shifted many healthcare systems’ priorities in 2020—including quite dramatically altering the priorities of the nation’s clinical laboratories—the SARS-CoV-2 pandemic does not appear to have slowed the pace of healthcare mergers and acquisitions. Many such deals are kept secret until closed by Dec. 31. They are then then announced after Jan. 1, so we may see additional big and surprising healthcare acquisitions announced in coming weeks.

Leaving aside the shock waves brought about by COVID-19, transformational changes to the healthcare community have been underway for a while.

In his article on HealthManagement.org, healthcare consultant Paul D. Vitale, MPA, FACHE, noted that for the past several years, health systems have set records in the mergers and acquisitions space. In 2017, he noted, there were more than 115 deals, and by 2019, there was a series of “mega” mergers, each worth more than $10 billion. The pattern continued in 2020, even with economic concerns brought about by the pandemic.

“According to many health systems, acquiring another organization, or merging with it, holds the key to future success. Faced with intense pressure to cut back on costs, mergers and acquisitions can leverage the economies of scale,” he wrote.

Below are several “deals” that closed in 2020 or are expected to close in 2021.

Pre-merger, Atrium Health’s network included 41 hospitals and 900 care locations, while the Wake Forest Baptist Health system was comprised of 42 hospitals and 1,500 care locations. Plans are underway to build a second campus for the school of medicine, where 3,500 students will be trained in more than 100 specialized programs.

“The impact of the strategic combination will be far-reaching, elevating North Carolina as a clear destination of choice to receive medical care for people all across the nation,” Julie Ann Freischlag, MD (above), CEO of Wake Forest Baptist Health and Dean of Wake Forest School of Medicine, told Healthcare Finance News. “Through our combined, nationally recognized clinical centers of excellence in multiple specialties, we will be able to expand our research in signature areas, such as cancer, cardiovascular, regenerative medicine and aging, and target bringing research breakthroughs to the community in less than half the time of the national average.” Freischlag will serve as Atrium Health’s Chief Academic Officer as well. (Photo copyright: Triad Business Journal.)

Doctors Acquire a Controlling Stake of Steward Health Care

In June, physicians in Dallas purchased a controlling stake of Steward Health Care through a structured recapitalization transaction. Though not strictly a merger and acquisition, the deal represents a similar transformational change of a health system. The change makes Steward the largest physician-owned-and-operated health system in the country, noted a news release.

Ralph de la Torre, MD (above), CEO and founder of Steward, says the industry is in the midst of a transformational moment. “The COVID-19 global pandemic has exposed serious deficiencies in the world’s healthcare systems, with a disproportionate impact on underserved communities and populations,” he stated in the news release. “We believe that future healthcare management must completely integrate long-term clinical needs with investments. As physicians first, we will focus on creating structures and timelines that meet the long-term clinical needs of our communities and the short-term needs of our patients.” (Photo copyright: The Boston Globe.)

Harrington Healthcare System and UMass Memorial Health Care

In January 2020, Harrington Healthcare of Massachusetts announced it was pursuing a corporate affiliation with UMass Memorial Health Care. The transaction was expected to be finalized by 2021.

“When we entered into our initial agreement with UMass Memorial in January, we had no idea what the next several months would bring,” said Ed Moore (above), President and CEO of Harrington Healthcare, in a news release. “Our team performed exceptionally well, and the community supported us every step of the way, but we could not have provided the outstanding care we did without the partnership and support of the clinical team at UMass Memorial. This experience redoubled our confidence that becoming part of the system would offer maximum benefit to our community at a time that requires flexibility, scale, and resources.” (Photo copyright: Worcester Telegram.)

Will More Announcements Come in 2021? Probably

For clinical laboratory managers and pathologists, the healthcare mergers and acquisitions of greatest interest are those that involve hospitals and health systems. When two big health systems merge—such as the transaction involving Atrium Health and Wake Forest Baptist Health—one of the first clinical services to undergo rationalization and consolidation is the clinical laboratory. One reason for this is because it is much easier to move more lab test specimens around the system than it is to move patients. So, many healthcare merger and acquisition deals directly affect the medical laboratory professionals employed by the institutions involved in the transaction.

Despite the pandemic—or because of the financial stresses created by it—there continue to be strong buyers and financially-weak sellers. For this reason alone, pathologists and clinical laboratory administrators should expect to see a regular flow of merger or acquisition announcements involving major healthcare organizations during 2021.

Clinical laboratory managers and pathology practice administrators should consider how these trends may affect their business and patients when planning for the future.

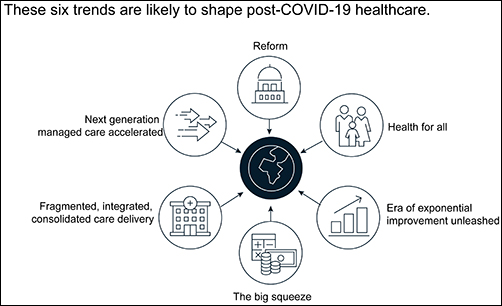

The McKinsey graphic above illustrates the “six trends that are likely to shape post-COVID-19 healthcare.” Clinical laboratories that support health networks struggling with any of these challenges should take steps to prepare for anticipated changes to healthcare delivery. (Graphic copyright: McKinsey and Company.)

1: Healthcare Reform

McKinsey identified three areas where the coronavirus pandemic may impact healthcare reform:

“COVID-19-era waivers that could become permanent.

“Actions that may be taken to strengthen the healthcare system to deal with pandemics.

“Reforms to address the COVID-19-induced crisis.”

McKinsey reports that “the Centers for Medicare and Medicaid Services has introduced more than 190 waivers since the beginning of March 2020.” These waivers can affect all aspects of healthcare, from clinical practice to reimbursement. Some of them, according to McKinsey, are “only relevant during the crisis (for example, the waiver of intensive care unit death reporting). A retrospective assessment of others (for example, expansion of telehealth access) could reveal beneficial innovation worth preserving.”

Several areas that McKinsey says are clearly ripe for reform include improving the resiliency of the healthcare system and the way the system is funded.

Public sector budgets are generally kept strictly separate, each with its own rules and policies that dictate operations. But in his article, “After COVID-19—Thinking Differently About Running the Health Care System,” published in JAMA Health Network, Stuart M. Butler, PhD, Senior Fellow in Economic Studies at the Brookings Institution, wrote, “The intensity of the COVID-19 pandemic … is forcing jurisdictions all across the country to find ways to be nimble so that multiple agencies can work together.”

Thus, McKinsey recommends, “Given the substantial shifts in relative market positioning among industry players that prior reforms have created, leaders would do well to plan ahead now.”

2: Better Access to Healthcare Services

Some people who develop COVID-19 are at far greater risk of hospitalization and death than others, including those who have:

Chronic health conditions, including obesity.

Mental and behavioral health challenges, such as substance abuse.

Unmet social needs, such as food or housing insecurity.

Poor access to healthcare.

McKinsey wrote that these “intersecting health and social conditions,” combined with certain races that have higher risk for severe complications, including Black, Indian, and Hispanic/Latino Americans, “correlated with poorer health outcomes.”

Value-based healthcare, telehealth, and greater attention to the social determinants of health may help address some of these issues, McKinsey notes, but the pandemic has shined a spotlight on how lack of care increases risk for certain populations during a public health crisis.

3: Era of Exponential Improvement Unleashed

Some of the trends that appear to be accelerating as a result of the pandemic are good news. McKinsey cites several benefits, including:

Improved understanding of patients.

Delivery of more convenient and individualized care.

$350-$410 billion in annual revenue by 2025.

Through telehealth and other types of virtual care enabled by digital technology, “intuitive healthcare ecosystems” may arise and offer a more integrated experience for patients and their caregivers, McKinsey notes.

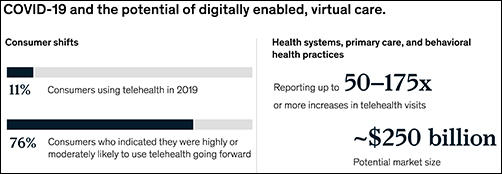

“While the pace of change in healthcare has lagged other industries in the past, potential for rapid improvement may accelerate due to COVID-19. An example is the exponential uptake of digitally enabled, virtual care,” McKinsey wrote. “Our analysis … showed that health systems, primary care, and behavioral health practices are reporting increases of more than 50–175 times in telehealth visits, and the potential market size for virtual care could reach around $250 billion.”

The graphic above is taken from the McKinsey and Co. report, which noted, “Proliferation of digitally enabled, virtual care could further contribute to the rise of personalized and intuitive healthcare ecosystems [that] have the potential to deliver an integrated experience to consumers, enhance productivity of providers, engage both formal and informal caregivers, and improve outcomes while lowering cost.” (Graphic copyright: McKinsey and Company.)

4: The Big Squeeze

The pandemic has caused an enormous outflow of cash from the healthcare system, and some experts don’t expect an injection of funding until 2022. “This outflow is expected to be primarily driven by coverage shifts out of employer-sponsored insurance and possible coverage reductions by employers as well as Medicaid rate pressures from states,” McKinsey states.

“We estimate that COVID-19 could depress healthcare industry earnings by between $35 billion and $75 billion compared with baseline expectations,” McKinsey predicted, adding, “Select high-growth segments will remain attractive (for example, virtual care, home health, software and platforms, specialty pharmacy) and will disproportionally drive growth. These high-growth areas are expected to increase more than 10% over the next five years, while other segments may stagnate or decline altogether.”

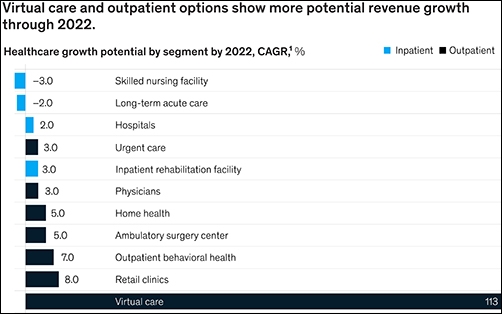

5: Fragmented, Integrated, Consolidated Care Delivery

McKinsey says, “The shift of care out of hospitals is not new but has been accelerated by COVID-19.” Rather than the hospital being the center of care delivery, patients are increasingly choosing to receive care at a range of sites across many healthcare ecosystems that are connected digitally and through analytics.

Early in the course of the pandemic, visits to ambulatory care facilities dropped nearly 60% by early April. But by mid-May, those visits were beginning to rebound.

In, “The Impact of the COVID-19 Pandemic on Outpatient Visits: A Rebound Emerges,” the Commonwealth Fund reported that “the relative decline in visits remains largest among surgical and procedural specialties and pediatrics” but is “smaller in other specialties, such as adult primary care and behavioral health.”

The McKinsey graphic above shows how “virtual care and outpatient options show more potential revenue growth through 2022.” Clinical laboratories that support those healthcare settings, especially ambulatory surgery, behavioral health, and retail clinics, should experience similar growth. (Graphic copyright: McKinsey and Company.)

6: Adoption of Next-Generation Managed Care Is Accelerating

How will COVID-19 affect the managed care industry? McKinsey says the “next generation” of managed care might use Medicare Advantage as a model.

“Payers pursuing the next generation of managed care model (through deep integration with care delivery) demonstrate better financial performance, capturing an additional 50 basis points of earnings before interest, taxes, depreciation, and amortization above expectation,” McKinsey noted, adding, “Employers and payers could consider fundamentally rethinking how employer-sponsored health coverage is structured. Learning from Medicare Advantage could provide inspiration for such a reimagination.”

What Should Clinical Laboratory Managers Do?

The McKinsey article concludes by stating, “While the challenges are numerous, leaders who seize the mindset that “disruptive change provides an opportunity to separate yourself from the pack” will build organizations meaningfully stronger than the ones they ran going into the crisis.”

The McKinsey article authors recommend that healthcare organizations take several proactive steps, including:

Launch a plan-ahead team.

Question your role and your future business model.

Prepare to transform your business.

Reimagine your organization to make faster decisions.

Take action to drive health equity.

Though the McKinsey and Company article covered healthcare in general, many of the authors’ observations and recommendations can apply to clinical laboratories and pathology groups as well and may be valuable in future planning.

CEOs of NorDx Laboratories, Sonora Quest Laboratories, and HealthPartners/Park Nicollet Laboratories expect demand for SARS-CoV-2 tests to only increase in coming months

The short answer is that large volumes of COVID-19 testing will be needed for the remaining weeks of 2020 and substantial COVID-19 testing will occur throughout 2021 and even into 2022. This has major implications for all clinical laboratories in the United States as they plan budgets for 2021 and attempt to manage their supply chain in coming weeks. The additional challenge in coming months is the surge in respiratory virus testing that is typical of an average influenza season.

Stan Schofield (above center), President of NorDx, a regional laboratory corporation that supports an integrated delivery system at MaineHealth in Portland, Maine.

Rick L. Panning (above right), MBA, MLS(ASCP)CM, retired as of Oct. 2 from the position of Senior Administrative Director of Laboratory Services for HealthPartners and Park Nicollet in Minneapolis-St. Paul, Minnesota.

Each panelist was asked how his parent health system and clinical laboratory was preparing to respond to the COVID-19 pandemic through the end of 2020 and into 2021.

First to answer was Panning, whose laboratory serves the Minneapolis-Saint Paul market.

A distinguishing feature of healthcare in the Twin Cities is that it is at the forefront of operational and clinical integration. Competition among health networks is intense and consumer-focused services are essential if a hospital or physician office is to retain its patients and expand market share.

Panning first explained how the pandemic is intensifying in Minnesota. “Our state has been on a two-week path of rising COVID-19 case numbers,” he said. “That rise is mirrored by increased hospitalizations for COVID-19 and ICU bed utilization is going up dramatically. The number of hospitalized COVID-19 patients has doubled during this time and Minnesota is surrounded by states that are even in worse shape than us.”

These trends are matched by the outpatient/outreach experience. “We are also seeing more patients use virtual visits to our clinics, compared to recent months,” noted Panning. “About 35% of clinical visits are virtual because people do not want to physically go into a clinic or doctor’s office.

“Given these recent developments, we’ve had to expand our network of specimen collection sites because of social distancing requirements,” explained Panning. “Each patient collection requires more space, along with more time to clean and sterilize that space before it can be used for the next patient. Our lab and our parent health system are focused on what we call crisis standards of care.

“For all these reasons, our planning points to an ongoing demand for COVID-19 testing,” he added. “Influenza season is arriving, and the pandemic is accelerating. Given that evidence, and the guidance from state and federal officials, we expect our clinical laboratory will be providing significant numbers of COVID-19 tests for the balance of this year and probably far into 2021.”

COVID-19 Vaccine Could Increase Antibody and Rapid Molecular Testing

Arizona is seeing comparable increases in new daily COVID-19 cases. “There’s been a strong uptick that coincides with the governor’s decision to loosen restrictions that allowed bars and exercise clubs to open,” stated Dexter. “We’ve gone from a 3.8% positivity rate up to 7% as of last night. By the end of this week, we could be a 10% positivity rate.”

Looking at the balance of 2020 and into 2021, Dexter said, “Our lab is in the midst of budget planning. We are budgeting to support an increase in COVID-19 PCR testing in both November and December. Arizona state officials believe that COVID-19 cases will peak at the end of January and we’ll start seeing the downside in February of 2021.”

The possible availability of a SARS-CoV-2 vaccine is another factor in planning at Dexter’s clinical laboratory. “If such a vaccine becomes available, we think there will be a significant increase in antibody testing, probably starting in second quarter and continuing for the balance of 2021. There will also be a need for rapid COVID-19 molecular tests. Today, such tests are simply unavailable. Because of supply chain difficulties, we predict that they won’t be available in sufficient quantities until probably late 2021.”

COVID-19 Testing Supply Shortages Predicted as Demand Increases

At NorDx Laboratories in Portland, Maine, the expectation is that the COVID-19 pandemic will continue even into 2022. “Our team believes that people will be wearing masks for 18 more months and that COVID-19 testing with influenza is going to be the big demand this winter,” observed Schofield. “The demand for both COVID-19 and influenza testing will press all of us up against the wall because there are not enough reagents, plastics, and plates to handle the demand that we see building even now.

“Our hospitals are already preparing for a second surge of COVID-19 cases,” he said.

COVID-19 patients will be concentrated in only three or four hospitals. The other hospitals will handle routine work. Administration does not want to have COVID-19 patients spread out over 12 or 14 hospitals, as happened last March and April.

“Administration of the health system and our clinical laboratory think that the COVID-19 test volume and demand for these tests will be tough on our lab for another 12 months. This will be particularly true for COVID-19 molecular tests.”

As described above, the CEOs of these three major clinical laboratories believe that the demand for COVID-19 testing will continue well into 2021, and possibly also into 2022. A recording of the full session was captured by the virtual Executive War College and, as a public service to the medical laboratory and pathology profession, access to this recording will be provided to any lab professional who contacts info@darkreport.com and provides their email address, name, title, and organization.

Robert L. Michel, Panelist—Publisher, Editor-in-Chief, The Dark Report and Dark Daily, Spicewood, Texas.

Given the importance of sound strategic planning for all clinical laboratories and pathology groups during their fall budget process, the virtual Executive War College is opening this session to all professionals in laboratory medicine, in vitro diagnostics, and lab informatics.

Though gene sequencing is touted as a key component of precision medicine, the medical value of direct-to-consumer testing has yet to show up in improved health outcomes, nor have clinical laboratories benefitted

In a recent example that the market for genetic genealogy testing may have peaked and the days of spectacular growth in the number of direct-to-consumer (DTC) genetic test orders and revenue is over, private-equity firm Blackstone—in a $4.7 billion deal—announced it will acquire a majority stake in Ancestry, which also does some clinical laboratory genetic testing as well.

Blackstone (NYSE:BX) acquired Ancestry of Lehi, Utah, one of the two largest genealogy testing companies (the other being 23andMe of Sunnyvale, Calif.), from a group of equity holders led by investment firms Silver Lake, GIC, Spectrum Equity, and Permira, noted a press release. GIC will retain a “significant minority stake” in Ancestry.

“We are very excited to partner with Ancestry and its management team. We believe Ancestry has significant runway for further growth as people of all ages and backgrounds become increasingly interested in learning more about their family histories and themselves,” David Kestnbaum, a Senior Managing Director at Blackstone, said in the press release. “We look forward to investing behind further data, functionality, and product development across Ancestry’s market leading platform to continue to provide a differentiated service.”

Is Genetic Testing for Genealogy Still a Growth Industry?

Ancestry is the global leader in digital family history services, operating in more than 30 countries with more than three million paying subscribers across its Ancestry online properties and more than $1 billion in annual revenue.

However, some experts say the road ahead may not be smooth for Ancestry or its major competitor, 23andMe.

“The business landscape fell off a cliff last year,” Laura Hercher, Director of Human Genetics Research at Sarah Lawrence College in New York, told STAT. “Fads pass,” she added.

Hercher points out that Ancestry has “this enormous database, which inherently has a lot of value hidden in it—potential energy. But they have not figured out how to get that information out in the way 23andMe has.”

23andMe’s pivot into medical research gained steam in 2018 when pharmaceutical giant GlaxoSmithKline (NYSE:GSK) purchased a $300 million stake in the company with the aim of using 23andMe’s resources to develop new medicines. That collaboration began bearing fruit earlier this year when GlaxoSmithKline started human trials of the first medicine (a cancer drug) to emerge from the partnership, STAT reported.

The public’s declining interest in at-home genealogy, however, has caused both companies to reduce staffing. 23andMe began the year by laying off about 100 employees—an estimated 14% of its workers—and Ancestry followed suit in February, letting go a similar number of employees, representing roughly 6% of its workforce.

According to MIT Technology Review, direct-to-consumer genetic genealogy testing reached its zenith in 2018 when consumers purchased as many DNA tests in one year as they had in all previous years combined, propelling total sales from Ancestry, 21andMe, and other DTC gene testing companies to roughly $26 million.

In 2019, CNBC reported that, market-wide, roughly 30 million tests had been sold across the globe. However, in recent years, sales have fallen short of expectations as the number of people willing to pay $99 to learn about their ancestry has dwindled. “I suspect those that are curious about this information are thinning out and there’s less people to go around to grow,” Greg Yap (above), Partner at Menlo Ventures, told CNBC. “I think there’s a broader issue, which is that the ultimate medical value is still really unproven,” Yap added. “There’s lots of research being done, but value for mass market consumer isn’t there yet, so it keeps a ceiling on the size of that market.” (Photo copyright: VentureBeat.)

Privacy Still a Concern

Ancestry has begun to insert itself into the genetic testing healthcare arena. In a press release, the company announced the launch of AncestryHealth, a $179 DNA testing kit that uses next generation sequencing (aka, high-throughput or massive parallel sequencing), aimed at providing adult consumers information on their inherited health risks.

However, as MedCity News points out, the sale to Blackstone has increased privacy concerns around the direct-to-consumer DNA testing market. Ancestry’s consumer privacy and data protections remain unchanged under the new ownership, but Alan Butler, Interim Executive Director at Electronic Privacy Information Center (EPIC), told MedCity News, “This is one example of a very troubling trend. It’s something regulatory agencies are not up to date to deal with. It’s one of the reasons we need comprehensive privacy law in the US.”

As genealogy companies such as 23andMe and Ancestry shift their focus from providing genetic histories to improving consumers’ health through genetic testing, clinical laboratories should be mindful of the logical next step, which is predicted to be genetic tests where the consumer collects the sample at home and the test is used to aid in diagnosing and treating patients.

This fourth edition of the annual event will be held virtually with free registration for pathologists and clinical laboratory professionals

In its fourth year, stakeholders in the clinical laboratory community have promoted thought leadership around the Lab Industry at the Project Santa Fe Foundation’s Clinical Lab 2.0 Workshop. Clinical Lab 2.0 (CL 2.0) which identifies new opportunities for medical labs to add value as the healthcare industry transitions from fee-for-service to value-based delivery models. But how does this concept apply during the era of COVID-19? That’s a key question participants will discuss at the 2020 Clinical Lab 2.0 Workshop, a virtual event scheduled for Oct. 26-27 with a focus on Population Health.

“This workshop will help all clinical laboratory leaders and pathologists to better understand, ‘How do we manage a pandemic, identifying high risk pool, where are the care gaps, and how do we better manage in the future proactively?’” said Khosrow Shotorbani, MBA, MT (ASCP), co-founder of the CL2.0 initiative and a regular speaker at the Executive War College, in an exclusive interview with Dark Daily. He is President and Executive Director of the Project Santa Fe Foundation, the organization that promotes the Clinical 2.0 Movement.

The coronavirus pandemic has “truly elevated the value of the clinical laboratory and diagnostics as one essential component of the care continuum,” he noted. “The value of the SARS-CoV-2 test became immense, globally, and the mantra became ‘test to trace to treat.’”

Project Santa Fe Foundation’s website defines Clinical Laboratory 2.0 as an effort to demonstrate “the power of longitudinal clinical lab data to proactively augment population health in a value-based healthcare environment.” The “goals are to improve the clinical outcomes of populations, help manage population risk, and reduce the overall cost of delivering healthcare,” the CL 2.0 website states.

“It’s about harnessing lab test results and other data that have predictive value and can help us proactively identify individuals that need care,” explained Shotorbani. “In the context of population health or value-based care, our labs potentially can utilize the power of this data to risk-stratify a population for which we are responsible or we can identify gaps in care.”

Clinical Lab 2.0 and the SARS-CoV-2 Pandemic

In the context of COVID-19, “Clinical Lab 2.0 argues that there is a hidden universe of value that can help augment what happens between COVID-19 testing and COVID-19 tracing to convert this reactive approach—meaning we wait for the person to get ill—versus considering who may be most at risk if they were to become infected so that our clinical laboratories can help caregivers create proactive isolation or quarantine strategies,” he added.

Shotorbani then explained how clinical laboratories have data about comorbidities such as diabetes, asthma, heart disease, and immunosuppression that are associated with more serious cases of COVID-19. “This clinical lab data can be harnessed, associated with demographic and risk data such as age and zip codes to help physicians and others identify patients who would be most at risk from a COVID-19 infection,” he noted.

“Historically, the primary focus of a clinical laboratory was very much on the clinical intervention, contacting the care manager physician, and identifying who’s at risk,” he said. But with COVID-19, Shotorbani sees opportunities to forge relationships with public health specialists to encourage what he describes as “consumer engagement.”

“As medical laboratory professionals, we must evolve to accommodate and support the needs of consumers as they take a more active role in their health,” he continued. “This is moving past simply providing lab test results, but to then be a useful diagnostic and therapeutic resource that helps consumers understand their health conditions and what the best next steps are to manage those conditions.”

Khosrow Shotorbani (above) is President, Executive Director, of the Project Santa Fe Foundation and one of the leaders of the Clinical Laboratory 2.0 movement. He is hopeful that the prominent role of medical laboratories in responding to the coronavirus pandemic will lead to an ongoing “seat at the table” in the higher echelons of healthcare organizations. In normal times, “we reside in basements, and we’re done when we release a result,” he said during an exclusive interview with Dark Daily. “COVID-19 was a kick in the rear to get us upstairs to the C-suite, because healthcare CEOs are under the gun to demonstrate more SARS-CoV-2 testing capacity.” Looking ahead, “we want to make sure that our clinical laboratories stay in that seat and design a future delivery model above and beyond COVID-19, maybe even help health systems, hospitals, and other providers drive their strategies.” (Photo copyright: Albuquerque Business First.)

“None of these are pathologists or come from the lab,” Shotorbani said. “They represent the C-suite and higher organization constituents. These are the healthcare executives who are dealing with their organization’s pain points. As clinical labs, we want to align ourselves to those organizational objectives.”

Pathologist Mark Fung, MD, PhD, will then present a CL 2.0 model for managing COVID-19 or other infectious disease pandemics, followed by a response from the other panelists. Fung is Vice Chair for Population Health in the Department of Pathology and Laboratory Medicine at the Larner College of Medicine at the University of Vermont. He is also on the Project Santa Fe Foundation (PSFF) board of directors.

“Lab 2.0 is a thought leadership organization,” Shotorbani said. “We are developing a template and abstract of this model of clinical laboratory services that other labs can follow while applying some of their own intuition as they make it operational.”

Day Two to the CL 2.0 workshop will feature case studies from the Henry Ford Health System in Detroit and Geisinger Health in Danville, Pa., followed by a discussion with eight PSFF directors. Then, Beth Bailey of TriCore Reference Laboratories in Albuquerque, N.M., will preside over a crowdsourcing session with participation from audience members.

Free Registration for Clinical Laboratories

This will be the first Clinical Lab 2.0 Workshop to be held virtually and registration this year will be free for members of the clinical laboratory community, Shotorbani said. In the past “there has been a hefty tuition to get into this because it’s a very high-touch workshop, especially for senior leaders. But given the critical topic that we’re facing, we felt it was important to waive the cost.”

The Fourth Annual Clinical Lab 2.0 Workshop is partnering this year with the American Society for Clinical Pathology (ASCP), which will provide the software platform for hosting the event, he said. In addition to the live conference sessions, registrants will have access to prerecorded presentations from past workshops. Content will be viewable for six months following the event.

Register for this critical event by clicking here, or by placing this URL in your browser (https://projectsantafefoundation.regfox.com/clinical-lab-20-workshop).