When people receive COVID-19 testing at an out-of-network facility, federal law requires insurers to pay that clinical laboratory’s posted ‘cash price’ when negotiated prices have not previously been established

In the latest example that some COVID-19 testing companies are charging significantly higher prices than others, The New York Times (NYT) recently reported that one COVID lab company with “more than a dozen testing sites” throughout the US was charging $380 for a COVID-19 rapid test that can be purchased at many drug stores for $20. Sadly, this practice, the NYT also noted, is protected by federal law.

Media reporters and the lay public are not fully aware of the long-established clinical laboratory test payment modalities that govern the daily performance of tests ordered as part of regular healthcare. Thus, when the COVID-19 pandemic hit—along with tens of billions of federal dollars to pay for SARS-CoV-2 tests—it triggered a gold rush of people wanting to get into the clinical laboratory testing business specifically to make money.

It is the bad actors in this group who are tainting the entire clinical laboratory industry with often outrageous business practices that, at best, cross ethical lines—such as overpricing tests to consumers—and at worst, represent fraudulent behavior, such as inducing medically-unnecessary tests, then submitting claims for these tests.

Even as the pandemic appears to be waning, news outlets are reporting instances of insurers being charged higher “cash prices” for tests performed by out-of-network testing laboratories. Worse yet, federal law requires insurers to pay these exorbitant prices and they are not happy about it.

In-Network versus Out-of-Network Pricing

In its report, the NYT noted that the CARES Act (H.R. 748) requires insurers to pay whatever “cash prices” out-of-network labs post online, and that this is leading to “expensive coronavirus tests” that could ultimately be reflected in future “higher insurance premiums” charged to healthcare consumers.

One company the NYT highlighted in its report is GS Labs in Omaha, Neb., a provider of COVID-19 testing throughout the US. The testing company’s COVID-19 Pricing Transparency webpage lists these prices for the following COVID-19 tests:

“Insurers are obligated to pay cash price, unless we come to a negotiated rate,” Christopher Erickson, a GS Labs Partner, told the NYT.

Negotiate or ‘Pay the Provider’s Cash Price’

In Missouri, Blue Cross and Blue Shield of Kansas City (Blue KC) has filed a lawsuit against GS Labs. “This action seeks a judgment declaring Blue KC and our members are not required to pay GS Labs’ unreasonable, inflated reimbursement demands,” according to a Blue KC news release.

However, section 3202 of the Coronavirus Aid, Relief, and Economic Security (CARES) Act “specifies the process for private health insurance plan issuers to reimburse providers of COVID-19 diagnostic tests. Specifically, a reimbursement rate negotiated for such test prior to the public health emergency declared on January 31, 2020, continues to apply for the duration of the emergency. If a reimbursement rate was not negotiated prior to the emergency declaration, an issuer may either negotiate such rate or pay the provider’s cash price.”

In its own news release, GS Labs said it has “countersued Blue KC over the insurance company’s failure to pay $9.7 million for COVID tests covered by federal law.”

According to a legal expert who spoke with the NYT, GS Labs has grounds for its test charges due to the CARES Act. “Whatever price the lab puts on their public facing website, that is what has to be paid. I don’t read a whole lot of wiggle room in it,” said Sabrina Corlette, JD, Research Professor and Co-Director of the Center on Health Insurance Reforms at Georgetown University.

“Unfortunately,” noted Loren Adler (above), Associate Director of the USC-Brookings Schaeffer Initiative for Health Policy, in a blog post, “this ‘cash price’ is not a market-determined price—it is irrelevant to patients because all options have to be made free to them by law, so there is little constraint on how high this is set by testing entities. Nor is there any reason for out-of-network entities to accept any less than this amount (other than a desire to contract in the future with the insurer for fear of a public relations backlash). Moreover, in theory the patient can still be surprise balance billed if the provider’s charge is higher than this ‘cash price,’ though it is unclear why any provider would list a ‘cash price’ lower than their charge.” (Photo copyright: The Brookings Institution.)

In his analysis, Adler suggested the law be revised to require commercial insurers to pay for COVID-19 testing at Medicare prices.

Patient Receives a $54,000 ‘Surprise’ Bill for COVID-19 Out-of-Network Test

The patient, Travis Warner, reportedly has insurance from Molina Healthcare through the federal Health Insurance Marketplace. After an employee at his company tested positive for COVID-19, Warner drove 30 miles outside of Dallas in search of COVID-19 testing sites. He eventually visiting an out-of-network free-standing emergency room in Lewisville where he received PCR diagnostic and rapid antigen tests. The results of the tests were negative for COVID-19. But the bill was a shock.

The total bill came to $56,384. Molina Healthcare paid its negotiated rate of $16,915.20 for the testing and facility fee, leaving Warner responsible for the remaining $54,000!

In the end, Warner did not have to pay the bill. Molina resolved the charge with SignatureCare and, in a statement to KHN, wrote, “This matter was a provider billing error, which Molina identified and corrected.”

For its part, SignatureCare Emergency Centers, with freestanding centers throughout Texas, said it has a “robust audit process” to flag errors and processed “thousands of records a day” at the height of the pandemic, according to KHN, which reported the business showing a $175 price for a COVID-19 test on its website.

“If the insurance company is paying astronomical sums of money for your care, that means in turn that you are going to be paying higher (insurance) premiums,” Adler told KHN.

Insurance Group Finds Price Gouging

“Price gouging on COVID-19 tests by certain providers continues to be a widespread problem,” according to a statement by America’s Health Insurance Plans (AHIP), a national association representing insurers.

AHIP has studied COVID-19 test prices since April 2020. It released a survey earlier this year which found COVID-19 test prices were on average $130. However, AHIP also found that out-of-network providers charged “significantly higher” (more than $185) for more than half (54%) of COVID-19 tests (PCR, antigen, antibody) in March 2021—a 12% increase since 2020. More than 27% of COVID-19 tests in March 2021 were done out-of-network, a 6% increase since 2020.

However, in, “COVID-19 Lab Test Prices Give Some Health Plans ‘Indigestion’,” Dark Daily’s sister publication, The Dark Report, wrote, “Interestingly, [AHIP] researchers reported that the share of COVID-19 tests claims submitted from ‘high-cost locations’—identified as hospitals and emergency departments—declined from 18% in the first three months of the pandemic to only 5% during the first three months of 2021.”

Niall Brennan, President and CEO of the Health Care Cost Institute (HCCI), told KHN, “People are going to charge what they think they can get away with. Even a perfectly well-intentioned provision like [the CARES Act] can be hijacked by certain unscrupulous providers for nefarious purposes.”

Of course, most medical laboratories priced their tests fairly and have performed them in an efficient and professional manner during the pandemic. So, it is unfortunate to learn through AHIP’s survey findings and the media that some COVID-19 testing providers are posting prices that may confuse patients and affect their health insurance premiums.

Prostate cancer currently has the highest positive surgical margin rate of any cancer in men, with 21% of patients left with cancer cells at the resection site

Cancer surgeons may soon have a new technology to help them completely remove cancerous tissue during prostate cancer surgery. Called Cerenkov luminescence imaging (CLI), this new diagnostic technology under development at the Essen University Hospital in Essen, Germany, will be of interest to surgical pathologists since it could become a common intraoperative strategy to improve surgical precision during radical cancer procedures.

For example, radical prostatectomy is the removal of the entire prostate gland and surrounding tissues. It is one of the primary treatments for malignant cancer. Failure to remove all the cancer tissue during the procedure typically leads to poor clinical outcomes, including tumor reoccurrence and subsequent increased risk of metastasis and death.

A 2018 study published in Nature Scientific Reports, titled, “Positive Surgical Margins in the 10 Most Common Solid Cancers,” noted that prostate cancer has the highest positive surgical margin rate of any cancer in men, with 21.03% of patients left with remaining cancer cells at the resection site.

Currently, intraoperative frozen-section analysis of the prostate is the most common intraoperative method for real-time analysis of surgical margins. But research into CLI may provide surgeons with an additional strategy for reducing positive surgical margins.

“Our objective was to assess the feasibility and accuracy of Cerenkov luminescence imaging (CLI) for assessment of surgical margins intraoperatively during radical prostatectomy,” they wrote.

According to the Essen researchers, the “single-center” study “included 10 patients with high-risk primary prostate cancer. 68Ga-PSMA PET scans were performed followed by radical prostatectomy and intraoperative CLI of the excised prostate. CLI images were analyzed postoperatively to determine regions of interest based on signal intensity, and tumor-to-background ratios were calculated. CLI tumor margin assessment was performed by analyzing elevated signals at the surface of the intact prostate images.

“To determine accuracy, tumor margin status as detected by CLI was compared to postoperative histopathology. Tumor cells were successfully detected on the incised prostate CLI images and confirmed by histopathology. Three patients had positive surgical margins, and in two of the patients, elevated signal levels enabled correct identification on CLI. Overall, 25 out of 35 CLI regions of interest proved to visualize tumor signaling according to standard histopathology,” the Essen researchers concluded.

The research showed that CLI can accurately assess surgical margins during radical prostatectomy. This first in vivo research of the technique was conducted over a 17-month period between 2018 and 2019.

“Intraoperative radio guidance with CLI may help surgeons in the detection of extracapsular extension, positive surgical margins, and lymph node metastases with the aim of increasing surgical precision,” said the study’s first author Christopher Darr, PhD (above), a resident urologist at Essen University Hospital, in a Society of Nuclear Medicine and Molecular Imaging (SNMMI) news release. “The intraoperative use of CLI would allow the examination of the entire prostate surface and provide the surgeon with real-time feedback on the resection margins.” (Photo copyright: Essen University Hospital.)

The researchers found that two of three patients who had positive surgical margins were correctly identified using CLI images. Overall, 25 of 35 CLI regions of interest successfully visualized tumor signaling, which is a result in line with standard histopathology. The one positive surgical margin CLI missed had group 3 prostate cancer at the surgical margin.

Essen Study Finds CLI Results in ‘Higher than Expected’ False Positives

A companion article published in the JNM, titled, “Cerenkov Luminescence Imaging for Surgical Margins in Radical Prostatectomy: A Surgical Perspective,” noted that, “Although this is consistent with other studies showing reduced PSMA (prostate-specific membrane antigen) expression in lower-grade prostate cancer, the interval between PSMA-agent injection and CLI (median, 333 min) was long and potentially detrimental to identification of lower-grade [prostate cancer]. Future studies may aim to reduce the interval between PSMA-agent injection and commencement of surgery to improve signal intensity and potentially the overall sensitivity of CLI.”

The Essen University Hospital’s CLI feasibility study also revealed the technique resulted in a higher-than-expected number of false positives, with 10 of 35 regions of interest showing “elevated signal levels without histopathologic evidence of PC tissue at the resection margin.” Most of the false positives occurred at the prostate base.

The Essen study authors speculated that the presence of radioactive tracer in the urinary bladder and other factors may explain the false positive rate. They suggested that, “Further optimization of the CLI protocol, or the use of lower-energy imaging tracers such as 18F-PSMA, is required to reduce false-positives.”

The researchers called for a larger study to assess CLI’s diagnostic performance.

Boris A. Hadaschik, PhD, Director of the Clinic for Urology at Essen University Hospital, added, “Radical prostatectomy could achieve significantly higher accuracy and oncological safety, especially in patients with high-risk prostate cancer, through the intraoperative use of radioligands that specifically detect prostate cancer cells. In the future, a targeted resection of lymph node metastases could also be performed in this way. This new imaging combines urologists and nuclear medicine specialists in the local treatment of patients with prostate cancer.”

Because of the high reoccurrence rate of prostate cancer in men, surgical pathologists will find this potential new strategy for reducing positive surgical margins a welcomed advancement, but additional investigation will be needed to ensure its promise can be realized.

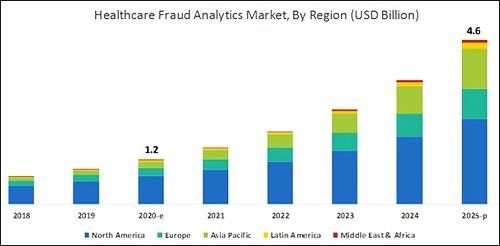

It did not take long for fraudsters to pursue hundreds of billions of federal dollars designated to support SARS-CoV-2 testing and it is rare when federal prosecutors bring cases only a few months after illegal lab testing schemes are identified

As if the COVID-19 pandemic weren’t bad enough, unscrupulous clinical laboratory operators quickly sought to take advantage of the critical demand for SARS-CoV-2 testing and defraud the federal government.

Unfortunately for the many defendants in these cases, federal investigations into alleged cases of fraud were launched with noteworthy speed. As a result of these investigations into alleged healthcare fraud by clinical laboratories and other organizations during fiscal year (FY) 2020, the US Department of Justice (DOJ) announced the US government has recovered $1.8 billion.

The federal prosecutions involved dozens of medical laboratory owners and operators who paid back “hundreds of millions in alleged federal healthcare program losses,” Goodwin Life Sciences Perspectives explained.

When combined with similar efforts starting in prior years, the program has returned to the federal government and private individuals a total of $3.1 billion, the DOJ noted.

“In its 24th year of operation, the program’s continued success confirms the soundness of a collaborative approach to identify and prosecute the most egregious instances of healthcare fraud, to prevent future fraud and abuse, and to protect program beneficiaries,” the report states.

According to the graphic above, which is based on analysis by B2B research company MarketsandMarkets, “North America will dominate the healthcare fraud analytics market from 2020–2025.” As clinical laboratory testing represents a significant portion of the fraud, medical lab managers will want to remain vigilant. (Graphic copyright: MarketsandMarkets.)

COVID-19 Pandemic an Opportunity for Fraud

The HHS report notes that the COVID-19 pandemic required CMS to develop a “robust fraud risk assessment process” to identify clinical laboratory fraud schemes, such as offering COVID-19 tests in exchange for personal details and Medicare information.

“In one fraud scheme, some labs are targeting retirement communities claiming to offer COVID-19 tests but are drawing blood and billing federal healthcare programs for medically unnecessary services,” the HHS report notes.

Still other alleged schemes involved billing for expensive tests and services in addition to COVID-19 testing. “For example, providers are billing a COVID-19 test with other far more expensive tests such as the Respiratory Pathogen Panel (RPP) and antibiotic resistance tests,” the report says.

“Other potentially unnecessary tests being billed along with a COVID-19 test include genetic testing and cardiac panels CPT (current procedural terminology) codes. Providers are also billing respiratory, gastrointestinal, genitourinary, and dermatologic pathogen code sets with the not otherwise specified code CPT 87798,” the report states.

Different Types of Healthcare Organizations Investigated in 2020

Beyond clinical laboratories, the HHS’ 124-page report also shares criminal and civil investigations of other healthcare organizations and areas including:

clinics,

drug companies,

durable medical equipment,

electronic health records,

home health providers,

hospice care,

hospitals and healthcare systems,

medical devices,

nursing home and facilities,

pharmacies, and

physicians/other practitioners.

According to the DOJ, “enforcement actions” in 2020 included:

1,148 new criminal healthcare fraud investigations opened,

440 defendants convicted of healthcare fraud and related crimes,

1,079 civil healthcare fraud investigations opened, and

1,498 pending civil health fraud matters at year-end.

“Federal Bureau of Investigation (FBI) investigative efforts resulted in over 407 operational disruptions of criminal fraud organizations and the dismantlement of the criminal hierarchy of more than 101 healthcare fraud criminal enterprises,” the DOJ reported.

Furthermore, the report said OIG investigations in 2020 led to:

578 criminal actions against people or organizations for Medicare-related crimes,

781 civil actions such as false claims, and

2,148 people and organizations eliminated from Medicare and Medicaid participation.

Implications for Clinical Laboratories

In 2020, OIG issued 178 reports, completed 44 evaluations, and made 689 recommendations to HHS divisions.

Clinical laboratory leaders may be most interested in those related to patient identification as a means to combating fraud and Medicare Part B lab testing reimbursement.

The HHS report says, “Medicare Advantage (MA) encounter data continue to lack National Provider Identifiers (NPIs) for providers who order and/or refer … clinical laboratory services,” adding that, “Almost half of MA organizations believe that using NPIs for ordering providers is critical for combating fraud.”

Additionally, the report states, “Medicare Part B spending for lab tests increased to $7.6 billion in 2018, despite lower payment rates for most lab tests. The $459 million spending increase was driven by:

“increased spending on genetic tests,

“ending the discount for certain chemistry tests, and the

“move to a single national fee schedule.”

Medical laboratory leaders may be surprised to learn that federal healthcare investigators were so vigorous in their investigations, even during the worst of the COVID-19 pandemic.

Vigilance is critical to ensure labs do not fall under the DOJ’s scrutiny. This HHS report, which describes the types and dollars involved in fraudulent schemes by clinical labs and other providers, could help inform revisions to federal compliance regulations and statutes.

Clinical laboratory managers and pathology practice administrators should consider how these trends may affect their business and patients when planning for the future.

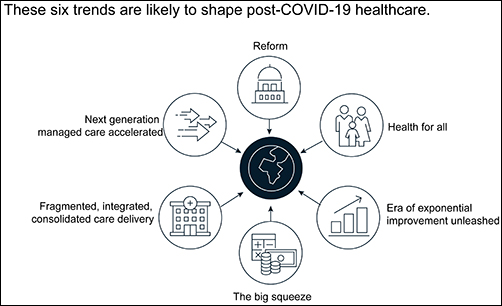

The McKinsey graphic above illustrates the “six trends that are likely to shape post-COVID-19 healthcare.” Clinical laboratories that support health networks struggling with any of these challenges should take steps to prepare for anticipated changes to healthcare delivery. (Graphic copyright: McKinsey and Company.)

1: Healthcare Reform

McKinsey identified three areas where the coronavirus pandemic may impact healthcare reform:

“COVID-19-era waivers that could become permanent.

“Actions that may be taken to strengthen the healthcare system to deal with pandemics.

“Reforms to address the COVID-19-induced crisis.”

McKinsey reports that “the Centers for Medicare and Medicaid Services has introduced more than 190 waivers since the beginning of March 2020.” These waivers can affect all aspects of healthcare, from clinical practice to reimbursement. Some of them, according to McKinsey, are “only relevant during the crisis (for example, the waiver of intensive care unit death reporting). A retrospective assessment of others (for example, expansion of telehealth access) could reveal beneficial innovation worth preserving.”

Several areas that McKinsey says are clearly ripe for reform include improving the resiliency of the healthcare system and the way the system is funded.

Public sector budgets are generally kept strictly separate, each with its own rules and policies that dictate operations. But in his article, “After COVID-19—Thinking Differently About Running the Health Care System,” published in JAMA Health Network, Stuart M. Butler, PhD, Senior Fellow in Economic Studies at the Brookings Institution, wrote, “The intensity of the COVID-19 pandemic … is forcing jurisdictions all across the country to find ways to be nimble so that multiple agencies can work together.”

Thus, McKinsey recommends, “Given the substantial shifts in relative market positioning among industry players that prior reforms have created, leaders would do well to plan ahead now.”

2: Better Access to Healthcare Services

Some people who develop COVID-19 are at far greater risk of hospitalization and death than others, including those who have:

Chronic health conditions, including obesity.

Mental and behavioral health challenges, such as substance abuse.

Unmet social needs, such as food or housing insecurity.

Poor access to healthcare.

McKinsey wrote that these “intersecting health and social conditions,” combined with certain races that have higher risk for severe complications, including Black, Indian, and Hispanic/Latino Americans, “correlated with poorer health outcomes.”

Value-based healthcare, telehealth, and greater attention to the social determinants of health may help address some of these issues, McKinsey notes, but the pandemic has shined a spotlight on how lack of care increases risk for certain populations during a public health crisis.

3: Era of Exponential Improvement Unleashed

Some of the trends that appear to be accelerating as a result of the pandemic are good news. McKinsey cites several benefits, including:

Improved understanding of patients.

Delivery of more convenient and individualized care.

$350-$410 billion in annual revenue by 2025.

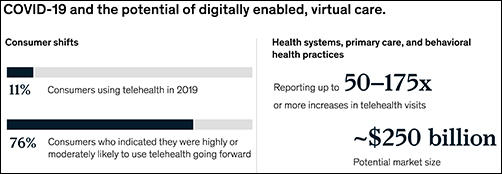

Through telehealth and other types of virtual care enabled by digital technology, “intuitive healthcare ecosystems” may arise and offer a more integrated experience for patients and their caregivers, McKinsey notes.

“While the pace of change in healthcare has lagged other industries in the past, potential for rapid improvement may accelerate due to COVID-19. An example is the exponential uptake of digitally enabled, virtual care,” McKinsey wrote. “Our analysis … showed that health systems, primary care, and behavioral health practices are reporting increases of more than 50–175 times in telehealth visits, and the potential market size for virtual care could reach around $250 billion.”

The graphic above is taken from the McKinsey and Co. report, which noted, “Proliferation of digitally enabled, virtual care could further contribute to the rise of personalized and intuitive healthcare ecosystems [that] have the potential to deliver an integrated experience to consumers, enhance productivity of providers, engage both formal and informal caregivers, and improve outcomes while lowering cost.” (Graphic copyright: McKinsey and Company.)

4: The Big Squeeze

The pandemic has caused an enormous outflow of cash from the healthcare system, and some experts don’t expect an injection of funding until 2022. “This outflow is expected to be primarily driven by coverage shifts out of employer-sponsored insurance and possible coverage reductions by employers as well as Medicaid rate pressures from states,” McKinsey states.

“We estimate that COVID-19 could depress healthcare industry earnings by between $35 billion and $75 billion compared with baseline expectations,” McKinsey predicted, adding, “Select high-growth segments will remain attractive (for example, virtual care, home health, software and platforms, specialty pharmacy) and will disproportionally drive growth. These high-growth areas are expected to increase more than 10% over the next five years, while other segments may stagnate or decline altogether.”

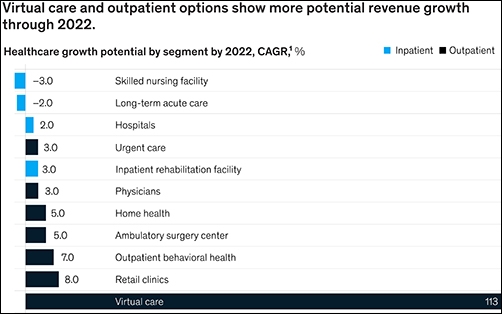

5: Fragmented, Integrated, Consolidated Care Delivery

McKinsey says, “The shift of care out of hospitals is not new but has been accelerated by COVID-19.” Rather than the hospital being the center of care delivery, patients are increasingly choosing to receive care at a range of sites across many healthcare ecosystems that are connected digitally and through analytics.

Early in the course of the pandemic, visits to ambulatory care facilities dropped nearly 60% by early April. But by mid-May, those visits were beginning to rebound.

In, “The Impact of the COVID-19 Pandemic on Outpatient Visits: A Rebound Emerges,” the Commonwealth Fund reported that “the relative decline in visits remains largest among surgical and procedural specialties and pediatrics” but is “smaller in other specialties, such as adult primary care and behavioral health.”

The McKinsey graphic above shows how “virtual care and outpatient options show more potential revenue growth through 2022.” Clinical laboratories that support those healthcare settings, especially ambulatory surgery, behavioral health, and retail clinics, should experience similar growth. (Graphic copyright: McKinsey and Company.)

6: Adoption of Next-Generation Managed Care Is Accelerating

How will COVID-19 affect the managed care industry? McKinsey says the “next generation” of managed care might use Medicare Advantage as a model.

“Payers pursuing the next generation of managed care model (through deep integration with care delivery) demonstrate better financial performance, capturing an additional 50 basis points of earnings before interest, taxes, depreciation, and amortization above expectation,” McKinsey noted, adding, “Employers and payers could consider fundamentally rethinking how employer-sponsored health coverage is structured. Learning from Medicare Advantage could provide inspiration for such a reimagination.”

What Should Clinical Laboratory Managers Do?

The McKinsey article concludes by stating, “While the challenges are numerous, leaders who seize the mindset that “disruptive change provides an opportunity to separate yourself from the pack” will build organizations meaningfully stronger than the ones they ran going into the crisis.”

The McKinsey article authors recommend that healthcare organizations take several proactive steps, including:

Launch a plan-ahead team.

Question your role and your future business model.

Prepare to transform your business.

Reimagine your organization to make faster decisions.

Take action to drive health equity.

Though the McKinsey and Company article covered healthcare in general, many of the authors’ observations and recommendations can apply to clinical laboratories and pathology groups as well and may be valuable in future planning.

CEOs of NorDx Laboratories, Sonora Quest Laboratories, and HealthPartners/Park Nicollet Laboratories expect demand for SARS-CoV-2 tests to only increase in coming months

The short answer is that large volumes of COVID-19 testing will be needed for the remaining weeks of 2020 and substantial COVID-19 testing will occur throughout 2021 and even into 2022. This has major implications for all clinical laboratories in the United States as they plan budgets for 2021 and attempt to manage their supply chain in coming weeks. The additional challenge in coming months is the surge in respiratory virus testing that is typical of an average influenza season.

Stan Schofield (above center), President of NorDx, a regional laboratory corporation that supports an integrated delivery system at MaineHealth in Portland, Maine.

Rick L. Panning (above right), MBA, MLS(ASCP)CM, retired as of Oct. 2 from the position of Senior Administrative Director of Laboratory Services for HealthPartners and Park Nicollet in Minneapolis-St. Paul, Minnesota.

Each panelist was asked how his parent health system and clinical laboratory was preparing to respond to the COVID-19 pandemic through the end of 2020 and into 2021.

First to answer was Panning, whose laboratory serves the Minneapolis-Saint Paul market.

A distinguishing feature of healthcare in the Twin Cities is that it is at the forefront of operational and clinical integration. Competition among health networks is intense and consumer-focused services are essential if a hospital or physician office is to retain its patients and expand market share.

Panning first explained how the pandemic is intensifying in Minnesota. “Our state has been on a two-week path of rising COVID-19 case numbers,” he said. “That rise is mirrored by increased hospitalizations for COVID-19 and ICU bed utilization is going up dramatically. The number of hospitalized COVID-19 patients has doubled during this time and Minnesota is surrounded by states that are even in worse shape than us.”

These trends are matched by the outpatient/outreach experience. “We are also seeing more patients use virtual visits to our clinics, compared to recent months,” noted Panning. “About 35% of clinical visits are virtual because people do not want to physically go into a clinic or doctor’s office.

“Given these recent developments, we’ve had to expand our network of specimen collection sites because of social distancing requirements,” explained Panning. “Each patient collection requires more space, along with more time to clean and sterilize that space before it can be used for the next patient. Our lab and our parent health system are focused on what we call crisis standards of care.

“For all these reasons, our planning points to an ongoing demand for COVID-19 testing,” he added. “Influenza season is arriving, and the pandemic is accelerating. Given that evidence, and the guidance from state and federal officials, we expect our clinical laboratory will be providing significant numbers of COVID-19 tests for the balance of this year and probably far into 2021.”

COVID-19 Vaccine Could Increase Antibody and Rapid Molecular Testing

Arizona is seeing comparable increases in new daily COVID-19 cases. “There’s been a strong uptick that coincides with the governor’s decision to loosen restrictions that allowed bars and exercise clubs to open,” stated Dexter. “We’ve gone from a 3.8% positivity rate up to 7% as of last night. By the end of this week, we could be a 10% positivity rate.”

Looking at the balance of 2020 and into 2021, Dexter said, “Our lab is in the midst of budget planning. We are budgeting to support an increase in COVID-19 PCR testing in both November and December. Arizona state officials believe that COVID-19 cases will peak at the end of January and we’ll start seeing the downside in February of 2021.”

The possible availability of a SARS-CoV-2 vaccine is another factor in planning at Dexter’s clinical laboratory. “If such a vaccine becomes available, we think there will be a significant increase in antibody testing, probably starting in second quarter and continuing for the balance of 2021. There will also be a need for rapid COVID-19 molecular tests. Today, such tests are simply unavailable. Because of supply chain difficulties, we predict that they won’t be available in sufficient quantities until probably late 2021.”

COVID-19 Testing Supply Shortages Predicted as Demand Increases

At NorDx Laboratories in Portland, Maine, the expectation is that the COVID-19 pandemic will continue even into 2022. “Our team believes that people will be wearing masks for 18 more months and that COVID-19 testing with influenza is going to be the big demand this winter,” observed Schofield. “The demand for both COVID-19 and influenza testing will press all of us up against the wall because there are not enough reagents, plastics, and plates to handle the demand that we see building even now.

“Our hospitals are already preparing for a second surge of COVID-19 cases,” he said.

COVID-19 patients will be concentrated in only three or four hospitals. The other hospitals will handle routine work. Administration does not want to have COVID-19 patients spread out over 12 or 14 hospitals, as happened last March and April.

“Administration of the health system and our clinical laboratory think that the COVID-19 test volume and demand for these tests will be tough on our lab for another 12 months. This will be particularly true for COVID-19 molecular tests.”

As described above, the CEOs of these three major clinical laboratories believe that the demand for COVID-19 testing will continue well into 2021, and possibly also into 2022. A recording of the full session was captured by the virtual Executive War College and, as a public service to the medical laboratory and pathology profession, access to this recording will be provided to any lab professional who contacts info@darkreport.com and provides their email address, name, title, and organization.

Robert L. Michel, Panelist—Publisher, Editor-in-Chief, The Dark Report and Dark Daily, Spicewood, Texas.

Given the importance of sound strategic planning for all clinical laboratories and pathology groups during their fall budget process, the virtual Executive War College is opening this session to all professionals in laboratory medicine, in vitro diagnostics, and lab informatics.

Though gene sequencing is touted as a key component of precision medicine, the medical value of direct-to-consumer testing has yet to show up in improved health outcomes, nor have clinical laboratories benefitted

In a recent example that the market for genetic genealogy testing may have peaked and the days of spectacular growth in the number of direct-to-consumer (DTC) genetic test orders and revenue is over, private-equity firm Blackstone—in a $4.7 billion deal—announced it will acquire a majority stake in Ancestry, which also does some clinical laboratory genetic testing as well.

Blackstone (NYSE:BX) acquired Ancestry of Lehi, Utah, one of the two largest genealogy testing companies (the other being 23andMe of Sunnyvale, Calif.), from a group of equity holders led by investment firms Silver Lake, GIC, Spectrum Equity, and Permira, noted a press release. GIC will retain a “significant minority stake” in Ancestry.

“We are very excited to partner with Ancestry and its management team. We believe Ancestry has significant runway for further growth as people of all ages and backgrounds become increasingly interested in learning more about their family histories and themselves,” David Kestnbaum, a Senior Managing Director at Blackstone, said in the press release. “We look forward to investing behind further data, functionality, and product development across Ancestry’s market leading platform to continue to provide a differentiated service.”

Is Genetic Testing for Genealogy Still a Growth Industry?

Ancestry is the global leader in digital family history services, operating in more than 30 countries with more than three million paying subscribers across its Ancestry online properties and more than $1 billion in annual revenue.

However, some experts say the road ahead may not be smooth for Ancestry or its major competitor, 23andMe.

“The business landscape fell off a cliff last year,” Laura Hercher, Director of Human Genetics Research at Sarah Lawrence College in New York, told STAT. “Fads pass,” she added.

Hercher points out that Ancestry has “this enormous database, which inherently has a lot of value hidden in it—potential energy. But they have not figured out how to get that information out in the way 23andMe has.”

23andMe’s pivot into medical research gained steam in 2018 when pharmaceutical giant GlaxoSmithKline (NYSE:GSK) purchased a $300 million stake in the company with the aim of using 23andMe’s resources to develop new medicines. That collaboration began bearing fruit earlier this year when GlaxoSmithKline started human trials of the first medicine (a cancer drug) to emerge from the partnership, STAT reported.

The public’s declining interest in at-home genealogy, however, has caused both companies to reduce staffing. 23andMe began the year by laying off about 100 employees—an estimated 14% of its workers—and Ancestry followed suit in February, letting go a similar number of employees, representing roughly 6% of its workforce.

According to MIT Technology Review, direct-to-consumer genetic genealogy testing reached its zenith in 2018 when consumers purchased as many DNA tests in one year as they had in all previous years combined, propelling total sales from Ancestry, 21andMe, and other DTC gene testing companies to roughly $26 million.

In 2019, CNBC reported that, market-wide, roughly 30 million tests had been sold across the globe. However, in recent years, sales have fallen short of expectations as the number of people willing to pay $99 to learn about their ancestry has dwindled. “I suspect those that are curious about this information are thinning out and there’s less people to go around to grow,” Greg Yap (above), Partner at Menlo Ventures, told CNBC. “I think there’s a broader issue, which is that the ultimate medical value is still really unproven,” Yap added. “There’s lots of research being done, but value for mass market consumer isn’t there yet, so it keeps a ceiling on the size of that market.” (Photo copyright: VentureBeat.)

Privacy Still a Concern

Ancestry has begun to insert itself into the genetic testing healthcare arena. In a press release, the company announced the launch of AncestryHealth, a $179 DNA testing kit that uses next generation sequencing (aka, high-throughput or massive parallel sequencing), aimed at providing adult consumers information on their inherited health risks.

However, as MedCity News points out, the sale to Blackstone has increased privacy concerns around the direct-to-consumer DNA testing market. Ancestry’s consumer privacy and data protections remain unchanged under the new ownership, but Alan Butler, Interim Executive Director at Electronic Privacy Information Center (EPIC), told MedCity News, “This is one example of a very troubling trend. It’s something regulatory agencies are not up to date to deal with. It’s one of the reasons we need comprehensive privacy law in the US.”

As genealogy companies such as 23andMe and Ancestry shift their focus from providing genetic histories to improving consumers’ health through genetic testing, clinical laboratories should be mindful of the logical next step, which is predicted to be genetic tests where the consumer collects the sample at home and the test is used to aid in diagnosing and treating patients.