Popularity of Medicare Advantage Plans fuels influx of new companies into the marketplace with anticipated enrollment of more than 22.6 million beneficiaries, or more than one-third of Medicare-eligible consumers

Continuing enrollment growth in Medicare Advantage plans is expected in 2019 and beyond. The projections are for double-digit percentage increases in Medicare Advantage enrollees. This is not auspicious for clinical laboratories and anatomic pathology groups because it means a shrinking proportion of Medicare beneficiaries remain in the Part B program.

Whereas any medical laboratory can provide services for any Medicare Part B beneficiary, that is not true for beneficiaries enrolled in Medicare Advantage plans. That’s because private health insurers operating Medicare Advantage plans typically contract with national lab companies while narrowing their lab networks, thereby limiting access to these patients by independent community laboratories, hospital lab outreach programs, and pathology groups.

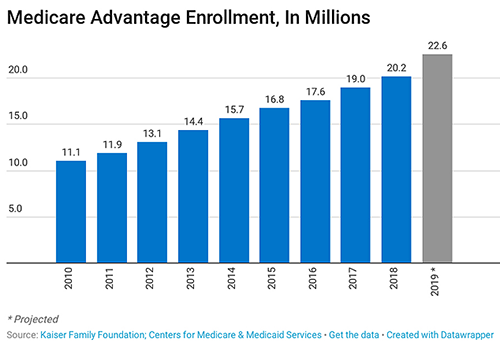

Enrollment in Medicare Advantage is expected to reach record totals in 2019. More than 22.6 million new Medicare beneficiaries are anticipated, with 14 new private companies offering plans, Kaiser Health News (KHN) reports. As enrollment shifts from traditional Medicare to Medicare Advantage the health of regional clinical laboratories can suffer, as smaller labs lose access to beneficiaries.

Enrollment in

Medicare Advantage Plans Increases, Despite Cut in Funding

Because Medicare Advantage penetration varies across counties and states, some local laboratories may experience less of an impact from the growing popularity of Medicare Advantage plans than others. According to the Kaiser Family Foundation (KFF), Medicare Advantage plans attract less than 11% of eligible beneficiaries in Arkansas, Vermont and Wyoming. However, more than 41% of Medicare participants in Florida, Hawaii, Minnesota, and Oregon choose Medicare private health plans over Medicare Part B.

Although the Patient Protection and Affordable Care Act (ACA) cut federal funding to Medicare Advantage plans, the 2010 law ultimately did not cause insurers to exit states or leave the business altogether, as was predicted. Instead, enrollment in Medicare Advantage doubled to more than 22.6 million enrollees, growing from a quarter of Medicare beneficiaries to more than a third, between 2010 and 2019, KHN reported.

Bonus payments from the federal government to Medicare

Advantage plans that have quality ratings of four or more stars (on a one to five

scale) helped fuel the growth. Plans without ratings also are eligible for

bonus payments, which must be used to reduce cost-sharing or premiums or to

provide extra benefits.

Since 2010, enrollment in Medicare Advantage has doubled to more than 22.6 million enrollees, growing from a quarter of Medicare enrollees to more than one-third. This trend is not favorable to many clinical laboratories, as the private health insurers who operate Medicare Advantage plans often contract with the billion-dollar lab companies and exclude regional and independent medical laboratories as network providers. (Photo copyright: Kaiser Family Foundation, Centers for Medicare and Medicaid Services.)

“The Affordable Care Act did not kill Medicare Advantage, and the program looks poised to continue to grow quite rapidly,” Bill Frack, Managing Director with healthcare advisor L.E.K. Consulting, told KHN.

In total, 2,734 Medicare Advantage plans will be available nationwide to consumers in 2019, an 18% increase from 2018 (417 more plans). That’s the largest number available since 2009, KFF announced late last year in a report on the program’s growth. These numbers exclude employer or union-sponsored group plans and Special Needs Plans, which are only available to select populations.

The average Medicare beneficiary has access to 24 Medicare

Advantage plans in 2019, an increase from 21 last year and 19 from 2016-2017.

Profits Increase

While Premiums Decline

Medicare Advantage plans are attractive to seniors because

premiums, deductibles, and cost sharing typically are lower than government-run

Medicare Part B and because many plans include additional benefits such as vision,

dental, and prescription drug coverage and fitness programs.

In a press release, the Centers for Medicare and Medicaid Services (CMS) noted that the Medicare Advantage average monthly premium has continued to steadily decline, recording an estimated 6% drop in 2019 to $28, from an average of $29.81 in 2018. Nearly 83% of Medicare Advantage enrollees remaining in their current plan will have the same or lower premium in 2019. Approximately 46% of enrollees in their current plan will have a zero premium.

“The steps that the Trump Administration has taken to improve and drive competition in Medicare Advantage means more savings, more benefits and lower costs for seniors, CMS Administrator Seema Verma said in the press release. “[With the] popularity of programs, such as Medicare Advantage, and with the various new supplemental benefits and policy changes that have been adopted, we expect plan choices to be even more robust moving forward.” [Photo copyright: Centers for Medicare and Medicaid Services.)

Declining premiums, however, have not meant reduced profits

for Medicare Advantage plan administrators. Healthcare Finance recently reported

that UnitedHealth Group’s third-quarter earnings from operations grew $502

million, or 12.3%, year-over-year to $4.6 billion, with growth in the insurer’s

Medicare Advantage business claiming most of the credit for the higher numbers.

UnitedHealthcare’s Medicare Advantage plans served 525,000

more consumers year-over-year, with the purchase of a physician-owned Medicare

Advantage organization in Louisiana accounting for 65,000 of the total.

“These results reflect our businesses delivering increased value at an accelerating pace to society and the millions of people we serve—one person at a time,” David S. Wichmann, CEO of UnitedHealth Group, told Healthcare Finance.

While Medicare Advantage plan growth may be good news for insurers,

the outlook for anatomic pathology groups and medical laboratories is less

rosy. The proportion of Medicare beneficiaries enrolled in the Part B program

shrinks steadily. Meanwhile, payers’ increased reliance on narrow networks as a

way to rein in rising costs excludes many regional laboratories. Ultimately,

these developments threaten many in the clinical laboratory industry, not just

smaller laboratories, and underline the need for pathologists and clinical

laboratory managers to add recognized value to the medical testing services

they provide in their communities.

Studies show medical laboratories may be particularly hit by adjustments to hospital chargemasters as hospitals prepare to comply with Medicare’s New Transparency Rule

Recently, Kaiser Health News (KHN) published a story about a $48,329 bill for allergy testing that cast a spotlight on hospital chargemaster rates just as healthcare providers are preparing to publish their prices online to comply with a new Centers for Medicare and Medicaid Services (CMS) rule aimed at increasing pricing transparency in healthcare. The rule goes into effect January 1, 2019.

The patient—a Eureka, Calif., resident with a persistent rash—had received an invoice for more than $3000 from her in-network provider.

Though this type of allergy skin-patch testing is usually performed in an outpatient setting by a trained professional, such as an allergist or dermatologist, the patient elected to have the testing performed at Stanford Health Care (Stanford), a respected academic medical system with multiple hospitals, outpatient services, and physician practices.

The patient’s insurance plan, Anthem Blue Cross (Anthem), paid $11,376 of the $48,329 amount billed by Stanford Health Care, which was the rate negotiated between the insurer and Stanford, Becker’s Healthcare reported. The patient ultimately paid $1,561 out-of-pocket.

So, where did that $48,329 in total charges come from? Experts pointed to the provider’s chargemaster. A chargemaster (AKA, charge description master or CDM) lists a hospital’s prices for services, suppliers and procedures, and is used by providers to create a patient’s bill, according to California’s Office of Statewide Health Planning and Development (OSHPD).

Chargemasters note high prices beyond hospitals’ costs and may be considered jumping off points for hospitals to use in invoicing payers and patients, RevCycleIntelligence explained.

Hospital representatives will negotiate with insurance companies, asking them to pay a discounted rate off the chargemaster list. A patient with health insurance accesses care at that negotiated rate and perhaps has responsibility for a share of that amount as well.

However, an out-of-network patient, uninsured person, or cash customer who receives care will likely be billed the full chargemaster rate.

In a statement to KHN, Stanford explained that the California woman’s care was customized and, therefore, costly: “We conducted a comprehensive evaluation of the patient and her environmental exposures and meticulously selected appropriate allergens, which required obtaining and preparing putative allergens on an individual basis.”

Johns Hopkins researchers Ge Bai, PhD, CPA (left), and Gerard Anderson, PhD (right), authored a study published in Health Affairs that shows “Hospitals on average charged more than 20 times their own costs in 2013 in their CT scan and anesthesiology departments.” Hospitals with clinical laboratory outreach programs will want to consider how their patients may respond as new federal price transparency requirements make it easier for patients to see medical laboratory test prices in advance of service. (Photo copyright: Johns Hopkins University.)

Now is a Good Time for Clinical Laboratories to Make Chargemaster Changes

Some organizations, such as the Healthcare Financial Management Association (HFMA), are calling for chargemaster adjustments as part of a comprehensive plan to improve transparency and lower healthcare costs. This falls in line with the new CMS rule requiring hospitals to post prices online starting Jan.1, 2019.

In fact, hospital medical laboratories, which cannot distinguish their services from competitors, may be impacted by the new CMS rule perhaps more than other services, the HFMA analysis warned.

“The initial impact for healthcare organizations, if they have not already experienced it, will be on commoditized services such as [clinical] lab and imaging. Consumers do not differentiate between high and low quality on a commoditized service the same way a physician might, which means cost plays a larger role in consumers’ decision making.” That’s according to Nicholas Malenka, Senior Consultant, GE Healthcare Partners, and author of the HFMA report. He advises providers to do chargemaster adjustments that relate charges to costs of services, competitors’ charges, and national data.

Are Chargemaster Charges Truly Excessive? Johns Hopkins Researchers Say ‘Yes!’

Most hospitals with 50 beds or more have a charge-to-cost ratio of 4.32. In other words, $432 is charged when the actual cost of a service is $100, according a study conducted by Johns Hopkins University and published in Health Affairs.

The researchers also noted in a news release about their findings titled, “Hospitals Charge More than 20 Times Cost on Some Procedures to Maximize Revenue,” that:

Charge-to-cost ratios range from 1.8 for routine inpatient care to 28.5 for a CT scan; and,

Hospitals with $100 in CT costs may charge an uninsured patient or out-of-network patient $2,850 for the service.

“Hospitals apparently markup higher in the departments with more complex services because it is more difficult for patients to compare prices in these departments,” lead author Ge Bai, PhD, CPA, Associate Professor at Johns Hopkins Carey Business School, noted in the news release.

“(The bills for high charges) affect uninsured and out-of-network patients, auto insurers, and casualty and workers’ compensation insurers. The high charges have led to personal bankruptcy, avoidance of needed medical services, and much higher insurance premiums,” co-author Gerard Anderson, PhD, Professor of Health Policy and Management at Johns Hopkins Bloomberg School of Public Health, stated in the news release.

Legal Issues Possible for Hospitals, Medical Laboratories, Other Providers

Still another study published in the American Journal of Managed Care (AJMC) explored the legality of “surprising” uninsured and out-of-network patients with bills at the chargemaster rates. It found that contract law supports market-negotiated rates—not chargemaster rates that do not reflect actual costs or the market.

“Patients and payers should know that they are under no obligation to pay surprise bills containing chargemaster rates, and state attorneys generally can use the law to prevent providers from pursing chargemaster-related collection efforts against patients,” the researchers wrote.

Labs Need to Get Involved

Clinical laboratory leaders in hospitals and health systems are advised to reach out to hospital chargemaster coordinators to ensure the chargemaster, as it relates to the lab, is inclusive, accurate, and in sync with competitive market data. Independent medical laboratories may want to similarly check their chargemasters to see how their lab test prices compare to the prices charged by other labs serving the same community.

Employers and consumers continue to pay more for health benefits from one year to the next, continuing a trend that is not auspicious for clinical laboratories and anatomic pathology groups

Most clinical laboratories don’t have the capability to collect payments from patients at time of service the same way patients pay doctors during office visits. Thus, Milliman’s annual report which details the increasing amounts patients are expected to pay out of their own pockets should be of interest to clinical laboratory managers and stakeholders. As this trend accelerates, labs will need to adopt new procedures and technologies to conduct business and remain profitable.

The Milliman Medical Index report (MMI) details how much consumers are predicted to pay for healthcare each year, as compared to previous years. Milliman, a Seattle-based independent actuarial and consulting firm with offices throughout the world, examines healthcare costs, property and casualty insurance, life insurance, financial services, and employee benefits.

Milliman released its first MMI in 2005. That year, the average annual medical cost for a family of four was $12,214.

Both Employees and Employers to See Increase in Healthcare Costs

The 2018 MMI report provides both good and bad news for the healthcare industry and patients. Milliman examined the costs for a typical family of four that participates in an employee-sponsored health insurance plan. For the report, a family of four consists of a 47-year old male, a 37-year old female, and two children under the age of five.

The MMI estimates a family of four will spend an average of $28,166 in healthcare expenditures in 2018. Included in this amount is the cost of the insurance paid by the employers and the employees, deductibles and out-of-pocket expenses. The figure represents an increase of $1,222 from 2017. The report found the amount families have been paying for healthcare has been increasing by an average of $100 per month over the last ten years.

The graphic above, taken from the 2018 Milliman Medical Index report, illustrates the increasing medical costs for a family of four. (Image copyright: Milliman.)

Both employers and employees will see an upsurge in costs from last year with employees experiencing an increase of 5.9% and employers seeing an increase of 3.5%.

The MMI found that employees will pay approximately 44% of their healthcare costs in 2018. By contrast, in 2008 employees paid less than 40% of their healthcare expenditures. In 2018, employers will pay about $15,788 of healthcare costs for a family of four, the employee will pay $7,674 via payroll deductions, with the remaining $4,704 being out-of-pocket expenses.

Costs Increasing While Growth Slows

The MMI also found that while the dollar amount families are spending on healthcare is increasing, the overall pace of the growth is slowing. The 4.5% rate of increase over last year is the slowest percentage growth in 18 years.

“We asked key stakeholders across the healthcare system what might be driving the decline in growth rates,” said Sue Hart, co-author of the MMI, in a Milliman news release. “Several common themes emerged, in particular provider engagement, more effective provider contracting, value-driven plan design, and spillover effects from public program initiatives.”

The reasons cited for this slowing trend include:

Involvement of healthcare providers to reduce costs;

More sophisticated contracting and provider consolidation;

Increased member cost sharing;

High deductible health plans;

Role of government and public programs; and the,

Impact of pharmacy initiatives.

“There are two ways of looking at this year’s MMI,” said Chris Girod, co-author of the Milliman Medical Index, in the news release. “On the one hand it’s heartening to see the rate of healthcare cost increase remain low. On the other hand, we’re still talking about more than $28,000 in total healthcare costs for the typical American family.”

The MMI graphic above breaks down healthcare costs into their constituent categories. (Image copyright: Milliman.)

To explore how costs have grown, the MMI examined five separate components of services. The typical family of four spends:

31% ($8,631) of their healthcare costs on inpatient facility care;

29% ($8,257) on professional services;

19% ($5,395) on outpatient facility care; and,

17% ($4,888) on pharmacy services.

The remaining 4% ($995) of costs are spent on other services, such as:

Home healthcare;

Ambulance services;

Durable medical equipment; and,

Prosthetics.

The MMI measures costs for a typical family of four, but certain families or individuals may have variations in costs depending on such factors as age, gender, health status, geographic area, provider variation, and insurance coverage.

Prescription drug costs is one such variance that is hard to predict. The 2018 MMI determined drug costs for a family of four increased by 6%, which represents the lowest percentage increase since 2015.

“Prescription drug costs have steadied, but this trend is volatile and hard to predict,” said Scott Weltz, co-author of the MMI in the news release. “High-cost drugs can have a big impact on trends, as we witnessed a few years ago when hepatitis C treatments hit the market. Alternatively, point-of-sale rebates could push a consumer’s costs in the other direction, particularly for people taking high-cost drugs. As the environment evolves, changes in drug prices can be deployed quite quickly.”

Scott Waltz (left), Christopher Girod (center), and Susan Hart (right) are Principles, Consulting Actuaries, for Milliman in Seattle. They co-authored the 2018 annual Milliman Medical Index report, which outlines the rising burden of out-of-pocket medical and insurance costs on patients, especially those on high deductible health plans. These costs are increasing and could impact clinical laboratories unprepared to collect fees at time of service. (Photo copyrights: Milliman.)

Preparing to Accept Payments

The results of this year’s MMI illustrate the impact increasing consumer costs could have on the way clinical laboratories conduct business and receive payments for services rendered. Studies have shown that patients with high deductible health plans (HDHPs), who frequently must pay 100% of lab costs, are especially affected by these trends. And the numbers of patients on HDHPs have increased each year since they were enacted.

Many clinical laboratories and anatomic pathology practices do not have the capability to collect fees from patients at the time of service. This lack of preparedness could threaten the survival of those labs and should be addressed.

Ongoing federal regulatory push for EHR interoperability requires medical laboratories and anatomic pathology groups to have strategies for ensuring seamless interfaces with providers and hospitals

Make the program more flexible and less burdensome;

Emphasize measures that require the exchange of health information between providers and patients; and,

Incentivize providers to make it easier for patients to obtain their medical records electronically.

“We’re excited to make these changes to ensure care will focus on the patient, not on needless paperwork,” CMS Administrator Seema Verma stated in the news release. “We’ve listened to patients and their doctors who urged us to remove the obstacles getting in the way of quality care and positive health outcomes. Today’s final rule reflects public feedback on CMS proposals issued in April and the agency’s patient-driven priorities of improving the quality and safety of care, advancing health information exchange and usability, and removing outdated or redundant regulation on healthcare providers to make way for innovation and greater value.” (Photo copyright: Centers for Medicare and Medicaid Services.)

According to a CMS fact sheet, key provisions of the overhaul include:

The rule finalized an EHR reporting period to a minimum of any continuous 90-day period in each of calendar years 2019 and 2020 for new and returning participants attesting to CMS or their State Medicaid agency;

For the Medicare Promoting Interoperability Program, the rule finalized a new performance-based scoring methodology consisting of a smaller set of objectives that CMS states will provide a more flexible, less-burdensome structure, allowing eligible hospitals and critical access hospitals (CAHs) to place their focus back on patients;

CMS finalized two new e-Prescribing measures related to e-prescribing of opioids (Schedule II controlled substances); and,

Beginning with an EHR reporting period in CY 2019, all eligible hospitals and CAHs under the Medicare and Medicaid PI programs will be required to use the 2015 Edition of Certified EHR Technology;

CMS finalized changes to measures, including removing certain measures CMS believes do not emphasize interoperability and the electronic exchange of health information.

According to CMS, about 3,300 acute care hospitals and 420 long-term care hospitals will be subject to the final rule, which takes effect October 1. Obviously, medical laboratories servicing these healthcare organizations will be similarly affected.

Rebranding More than a Name Change

Healthcare Informatics analyzed the 2,593-page final rule explaining that the “core emphasis” of the meaningful use overhaul is “on advancing health data exchange among providers.”

The initial proposal in April, according to Healthcare Informatics, invited stakeholder feedback through a request for information on the possibility of revising CMS’ “Conditions of Participation” for hospitals by requiring providers to electronically transfer medically necessary information following a patient discharge or transfer. The final rule, however, did not include that change.

Instead, the CMS Fact Sheet on the rule states the April request for information was “to obtain feedback on positive solutions to better achieve interoperability, or the sharing of healthcare data between providers, which will inform next steps in advancing this critical initiative.”

Rebranding meaningful use is CMS’s first step in implementing core pieces of the Administration’s MyHealthEData Initiative to strengthen interoperability. In remarks during the ONC Interoperability Forum in Washington, DC, CMS Administrator Seema Verma described the rebranding decision as “much more than a name change” and signaled future CMS actions.

“It is a change in direction for the programs—from programs that support the adoption of health IT, to programs that promote interoperability and patient access to data,” she explained. “To avoid payment reductions and gain incentives, doctors and hospitals will have to give patients electronic access to their health records. We are also considering whether CMS should require—as a condition of participation in the Medicare program—that providers share data with patients in a universal electronic format and hope to share more information on that soon.”

The recent changes follow passage of the Bipartisan Budget Act of 2018, which included a provision relaxing meaningful-use requirements. Though the legislation affects only hospitals and outpatient Medicaid providers, Robert Tennant, Director of Health Information Technology Policy for the Medical Group Management Association (MGMA), declared the revision a “huge win” for providers.

“I don’t think the government recognized how difficult it would be to move from stage 1 to stage 2 to stage 3 [meaningful use] requirements and the significant costs involved,” Tennant stated told Modern Healthcare. “We hope that it signals an interest in Congress in having the administration and HHS (Federal Health and Human Services) not make these quality reporting programs so onerous that it results in large swaths of providers not being successful.”

Clinical laboratories and anatomic pathology groups should be aware that interoperability between their laboratory information systems and the EHRs of providers and hospitals continues to be important. Although the term “Meaningful Use” is to be supplanted by “Promoting Interoperability,” the ability to move patient health information seamlessly among providers continues to be a major goal of this country’s healthcare system.

Healthcare revenue cycle consultant Jonathan Wiik suggests healthcare providers must prepare their organizations for patients who need help paying increasing medical costs

A recent analysis of this issue by TransUnion Healthcare (NYSE:TRU) states, “patients experienced an 11% increase in average out-of-pocket costs during 2017, rising from $1,630 in Q4 2016 to $1,813 in Q4 2017.” It is a development that should send up red flags to clinical laboratory managers seeking ways to maintain and increase revenues.

“Given the increased payment responsibility, being able to determine a patient’s ability to pay is increasingly important for hospitals,” noted Jonathan Wiik, Principal, Healthcare Strategy at TransUnion Healthcare (TRU). “In order to allow patients to focus on getting the care they need healthcare providers need processes and tools in place to help patients meet their financial obligations and to establish funding mechanisms that will benefit both the patient and provider.” Obviously, this also applies to clinical laboratories.

According to a news release, “The [TRU] analysis also revealed that in 2017, on average, 49% of patient out-of-pocket costs per healthcare visit were below $500; 39% were $501-$1,000; and 12% were more than $1,000.”

For providers, patients’ swelling unpaid balances mean more uncompensated care, the analysis also showed. And that means more unpaid balances for clinical laboratories as well.

“Increasing healthcare costs and patient responsibility is a continuing trend that does not seem to be slowing anytime in the near future,” noted Jonathan Wiik (above) Principal, Healthcare Strategy, at TransUnion Healthcare and author of the new book “Healthcare Revolution: The Patient Is the New Payer,” during a HIMSS 2018 presentation. (Photo copyright: Colorado Managed Care Collaborative.)

Patients Struggle to Pay Amounts Under $500

Each year, more healthcare consumers are forced onto high-deductible health plans (HDHPs) that make them responsible for thousands and even tens of thousands of dollars in upfront costs.

And according to another TRU news release, patients with commercial insurance plans experienced a 67% increase in their financial responsibility over five years. In other words, after insurance plans paid providers, patients still needed to pony up 12.2% of the total bill in 2017, as compared to 8% in 2012.

During the most recent year studied by TransUnion Healthcare, patients’ out-of-pocket costs increased 11%, rising to $1,813 in 2017 from $1,630 in 2016, a news release revealed.

And it doesn’t take a huge bill for patients to feel the pain. TransUnion’s data reveals that 68% of patients with medical bills below $500 did not fully pay what they owed, RevCycle Intelligence reported. This has major implications for clinical laboratories and anatomic pathology groups because many lab charges fall under $500 and TransUnion shows that almost 70% of patients do not pay the full amount of these bills.

According to TRU, medical specialties with the highest out-of-pocket estimated amounts due from patients include:

And, as Dark Daily previously reported, affluent and self-employed people also feel the pinch, as deductibles can be as high as $5,000/year for individuals and more than $10,000/year for a families, whether plans are purchased through the Affordable Care Act (ACA) or employers.

When patients cannot afford to pay their bills, hospitals’ bad debt and charity-care levels rise. Together, bad debt and charity care comprise a provider’s uncompensated care.

“A lot of patients can’t afford these bills, which is why uncompensated care has bounced,” Wiik told Modern Healthcare.

Indeed, uncompensated care was $38.3 billion in 2016, up $2.6 billion since 2015, according to an American Hospital Association (AHA) 2017 fact sheet.

Meanwhile, the Centers for Medicare and Medicaid Services (CMS) reported that Medicare bad debt (the effect of Medicare patients not paying deductibles and co-pays) increased to $3.69 billion in 2016 from $3.14 billion in 2012, a 17% bump, TransUnion Healthcare pointed out.

Consumers Say They Want Prices, Financing Plans

Consumers say healthcare providers are not transparent about costs for procedures, nor do they effectively offer financing options. That’s according to a HealthFirst Financial news release, which states, “More than three-quarters, or 77%, of healthcare consumers say it’s important or very important they know their costs before treatment and 53% want to discuss financing options before care. However, the vast majority of healthcare providers are not satisfying these consumer demands.”

“53% voice concern about the ability to pay a medical bill of less than $1,000;

“35% worried about the ability to pay a bill of less than $500; and,

“16% are concerned about the ability to pay a bill of less than $250.”

These numbers fall well into the amounts clinical laboratories charge for services rendered.

What Can Medical Laboratories Do?

To help their customers pay their bills and improve revenue, Dark Daily suggest labs:

Use software that enables ordering clinicians to process advanced beneficiary notices and prior authorizations for services;

Inform the customer prior to specimen collection about their financial responsibility for the test;

Ask for payment-due at time of the patient encounter;

Share key lab test price data in easily accessible and understandable ways;

Keep credit card information securely on-hand for agreed-to balances patients are responsible for paying; and,

Offer payment options, such as e-billing and financing plans.

As we’ve pointed out many times, because clinical laboratories are dependent on the physicians and hospitals they service, they are particularly vulnerable when patients stop paying their bills.

As PAMA brings estimated Medicare reimbursement cuts of up to 30% over the next three years to a range of typically high-volume tests and diagnostics, medical laboratories that wish to stay competitive must understand the needs of managed care payers and learn how to optimize collections, reduce denials, and communicate value effectively or risk their financial health

Recent years have seen major shifts in consolidation, automation, and efficiency analysis to help streamline both workflows and cashflows. However, the threat from the current and coming cuts to Medicare lab test prices will be particularly acute for smaller independent laboratories and hospital/health system lab outreach programs. These labs will continue to feel added strain due to reduced reimbursement across 25 of the most common tests billed to Medicare.

And, that doesn’t account for subsequent cuts, which are estimated to reach nearly 30% over the next three years.

Cost of Service Disparities/In-Network Status Further Impact Clinical Labs

If the CLFS reductions weren’t enough, labs face another threat—managed care and commercial payers aligning with big national laboratories and narrowing networks in an attempt to lower costs and provide maximum return for both patients and shareholders. For smaller and independent laboratories, this represents a double threat.

In the first situation, larger laboratories can offer services at lower costs due to increased automation, batch processing, and other scale advantages. This means that while the lower CLFS rates will impact the financial integrity of larger labs, the actual margin lost is less than that of smaller laboratories and facilities that face higher costs to perform tests and provide services.

Compounding the situation, commercial and managed care payers searching out the best value for their patients and shareholders tend to narrow their networks by excluding many independent clinical lab companies and hospital lab outreach programs, amplifying this inherent disparity and skewing the advantage away from independent providers yet again.

Higher cost providers without a clear understanding of promoting their value to payers could have trouble obtaining in-network status. Yet, failing to obtain in-network status may reduce overall test quantities, further raise prices, and make smaller labs less competitive with larger national laboratories—a dangerous cycle with today’s competitive laboratory landscape.

Shifting Focus and Optimizing Managed Care Reimbursements

As the financial stability of Medicare reimbursements wanes, it is imperative that laboratories look to new methods to further increase efficiency and stabilize cashflows. Once a smaller portion of laboratory revenue, managed care organizations and commercial payers will be of increased importance as overall reimbursement rates continue to shrink in the face of healthcare reform and value-based care.

Special June 26 Webinar: Improving Managed Care Reimbursement Efficiency

Understanding not just what these payers are attempting to achieve for their organization—but also how they structure requirements and processes to support their goals—is an essential element of succeeding in this previously smaller share of the marketplace.

For those interested in learning more about critical concerns regarding managed care payers in the post-2018 CLFS landscape, Pathology Webinars is hosting a 90-minute webinar on Tuesday, June 26, 2018, at 2:00 PM Eastern.

The webinar will include presentations from two experts on a range of topics including:

Actionable steps to absorb the loss of Medicare revenue due to the impact of the 2018 CLFS reductions;

How managed care payers process network status and payments;

Who in the managed care chain of command should receive your value proposition;

How to better align your value propositions, policies, and workflows with the requirements of managed care and commercial payers; and,

Understanding the roles managed care payers expect clinical laboratories and anatomic pathologists to play in managing and reducing unnecessary testing.

The first speaker, Frank Dookie, MBA, will provide an inside look at:

How managed care payers function;

Their requirements and workflows; and,

What they look for when considering network status for a laboratory.

Dookie is a laboratory professional who has worked on the payer side for 28 years. He is passionate about the role that diagnostics play or can play in healthcare, and has spent his career working for instrumentation providers, clinical laboratories, the intermediary space between laboratories and managed care companies, and managed care companies.

The second speaker, Michael Snyder, will bring the entire payment process into sharp focus. He will cover:

Optimizing the collection process;

Identifying the purpose of each step, each review, and each team member involved; and,

Critical points laboratories must address to ensure payment.

Snyder is the Senior Vice President of Network Operations for Avalon Healthcare Solutions, LLC, a firm that provides comprehensive benefit management services to the health plan industry and has more than 30 years’ experience in clinical laboratory management.

Frank R. Dookie, MBA (left), Contracting Executive with a major managed care company in Woodbridge, N.J.; and Michael Snyder (right), Senior Vice President with Avalon Healthcare Solutions in Flemington, N.J., will provide critical insights and actionable details for clinical laboratory and anatomic pathology group leaders who want to ensure future revenues.

An Essential Opportunity to Improve Your Reimbursements

This critical webinar offers anatomic pathology groups and medical laboratory managers essential information and actionable next steps to immediately leverage the potential of managed care payers. Additionally, it provides insider insight to laboratories straining to retain financial integrity as reduced reimbursements and increased regulatory burdens strain budgets and cashflows.

To register for the webinar and see further details about discussion topics, use this link (or copy and paste the URL into your browser: https://pathologywebinars.com/current/managed-care-an-insiders-guide-to-improving-your-reimbursement-efficiency-with-strategies-that-work-626/).

As further Medicare payment reductions over the next three years drive reimbursements even lower, understanding how to capture the positive attention of payers—while working within the rules and policies driving their reimbursement decisions—will be an essential element of successful laboratory management and growth. Register now!

, and Gerard Anderson, PhD (right)")

, Christopher Girod (center), and Susan Hart (right)")

, Contracting Executive with a major managed care company in Woodbridge, N.J.; and Michael Snyder (right)")