Clinical laboratories that service both settings could be impacted as new CMS proposed rule attempts to align Medicare’s payment policies for outpatient and in-patient settings

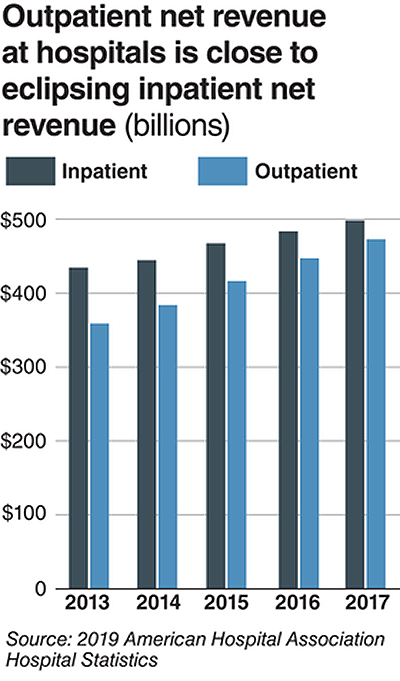

Hospital outpatient revenue is catching up to inpatient

revenue, according to data released from the American

Hospital Association (AHA). This increase is part of a growing trend to

reduce healthcare costs by treating patients outside of hospital settings. It’s

a trend that is supported by the White House and Medicare and continues to

impact clinical

laboratories, which serve both hospital inpatient and outpatient customers.

The AHA published this study data in its annual Hospital Statistics, 2019Edition. The data comes from a 2017 survey of 5,262

US hospitals. The report includes data about utilization, revenue, expenses,

and other indicators for 2017, as well as historical data.

The AHA statistics on outpatient revenue suggest providers

nationwide are working to keep people out of more expensive hospital settings. Hospitals,

like medical

laboratories, appear to be succeeding at developing outpatient and outreach

services that generate needed operating revenue.

This aligns with Medicare’s push to make healthcare more accessible through outpatient settings, such as urgent care clinics and physician’s offices. A growing trend Dark Daily has covered extensively.

Outpatient Revenue

Climbs

In its coverage of

the AHA’s study, Modern Healthcare reported that 2017

hospital net inpatient revenue was $498 billion and net outpatient revenue was

$472 billion.

The Becker’s Hospital CFO Report notes that

gross inpatient revenue in 2017 was $92.7 billion higher than gross outpatient

revenue. But in 2016, gross inpatient revenue was much further ahead—$129.5

billion more than gross outpatient revenue. The “divide” between inpatient and

outpatient revenue is narrowing, Becker’s reports.

The graphic above illustrates the shrinking gap between hospital inpatient and outpatient revenues. “Outpatient revenue will ultimately eclipse inpatient revenue,” Chuck Alsdurf, Director of Healthcare Finance Policy and Operational Initiatives at the Healthcare Financial Management Association (HFMA), told Modern Healthcare. (Graphic copyright: Modern Healthcare/AHA.)

The Becker’s

report also stated:

Admissions increased by less than 1% to 34.3

million in 2017, up from 34 million in 2016;

Inpatient days were flat at 186.2 million;

Outpatient visits rose by 1.2% to 766 million in

2017; and,

Outpatient revenue increased 5.7% between 2016

and 2017.

Similar Study Offers Additional

Insight into 2018 Outpatient Revenue

A benchmarking report by Crowe,

a public accounting, consulting, and technology firm, which analyzed data from

622 hospitals for the period January through September of 2017 and 2018, showed

the following, as reported by RevCycleIntelligence:

Inpatient volume was up 0.6% in 2018 and gross

revenue per case grew by 5.3%;

Outpatient services rose 2.4% in 2018 and gross

revenue per case was up 7.1%.

Physicians’ Offices

Have Lower Prices for Some Hospital Outpatient Services

Everything, however, is relative. When certain healthcare

services traditionally rendered in physician’s offices are rendered, instead,

in hospital outpatient settings, the numbers tell a different story.

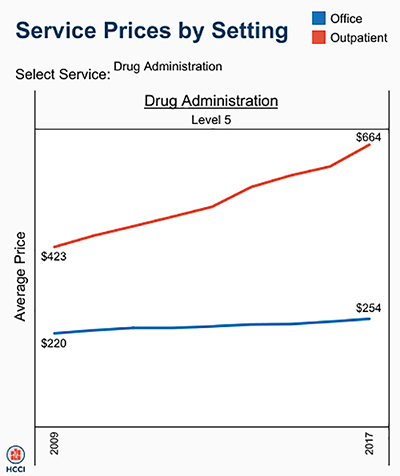

In fact, according to the Health

Care Cost Institute (HCCI), the price for services was “always higher” when

performed in an outpatient setting, as compared to doctor’s offices.

HCCI analyzed services at outpatient facilities as well as

those appropriate to freestanding physician offices. They found the following

differences in 2017 prices:

Diagnostic and screening ultrasound: $241 in

physician’s office—$650 in hospital outpatient setting;

Level 5 drug administration: $254 in office—$664

in hospital outpatient setting;

Upper airway endoscopy: $527 in office—$2,679 in

hospital outpatient setting.

One example where hospital outpatient settings provide similar services at increased costs is in drug administration, as the graphic above illustrates. “The difference was higher than I expected. With some services, the price is two or three times higher when rendered in the outpatient setting,” Julie Reiff, HCCI researcher and report author, told Fierce Healthcare. (Graphic copyright: HCCI.)

Medicare Proposed

Rule Would Change How Hospital Outpatient Clinics Get Paid

Meanwhile, the Centers for

Medicare and Medicaid Services (CMS) has released its final rule (CMS-1695-FC),

which make changes to Medicare’s hospital outpatient prospective payment and

ambulatory surgical center payment systems and quality reporting programs.

In a news

release, CMS stated that it “is moving toward site neutral payments for

clinic visits (which are essentially check-ups with a clinician). Clinic visits

are the most common service billed under the OPPS [Medicare’s Hospital

Outpatient Prospective Payment System). Currently, CMS often pays more for

the same type of clinic visit in the hospital outpatient setting than in the

physician office setting.”

“CMS is also proposing to close a potential loophole through

which providers are billing patients more for visits in hospital outpatient

departments when they create new service lines,” the news release states.

Hospitals are fighting the policy change through a lawsuit, Fierce Healthcare reported.

In summary, clinical laboratories based in hospitals and

health systems are in the outpatient as well as inpatient business. Medical laboratory

tests contribute to growth in outpatient revenue, and physician offices compete

with clinical laboratories for some outpatient tests and procedures. Thus, a new

site-neutral CMS payment policy could affect the payments hospitals receive for

clinic visits by Medicare patients.

Shifts to new types of facilities where patients are treated provide clinical laboratories and pathology groups with new opportunities to add value to providers and patients

Two important trends have serious implications for the nation’s traditional hospitals. One is the ongoing shift of patient care from inpatient settings to outpatient providers. The other trend is to proactively manage patients so as to avoid the need for hospitalization. Both trends create challenges and opportunities for medical laboratories and anatomic pathology groups.

Thus, it is significant that one advisory group to the federal government on Medicare and health policy recognizes these trends with the recommendations it made to Congress. In June, the Medicare Payment Advisory Commission (MedPAC) released its “Medicare and the Health Care Delivery System” report to Congress. It includes proposals that support healthcare’s shift toward outpatient settings and away from in-hospital care. It also makes two recommendations that impact EDs based on their locations (rural versus urban) and proximity to parent hospitals.

MedPAC believes that shifting money/reimbursement toward different sites of care and for different services improves the ability of providers to be proactive and manage patients in ways that support earlier diagnosis and more active management of conditions—all in ways that help avoid acute events that would otherwise send patients to hospitals.

Thus, for clinical laboratories, the message with MedPAC is that other sites of service would get better reimbursement for the above reasons and would want lab services that support the objectives of their providers. And the recommended enrichment of reimbursement for ambulatory evaluation and similar management services would encourage providers to do a better job of ordering the right test and doing the right thing with the results. This gives labs an opportunity to add value.

Ensuring Access to ED Services in Rural Environments

MedPAC is a nonpartisan legislative branch agency that provides the US Congress with analysis and policy advice on the Medicare program. Most of the points the June report makes pertain to the Medicare program in general. However, chapter two of MedPAC’s report addresses payments to emergency departments specifically, including:

Increasing Medicare payment rates to isolated rural stand-alone EDs; and,

Decreasing payment rates to urban stand-alone EDs located near hospital-based emergency departments.

To ensure rural residents have access to ED services, MedPAC recommends allowing hospitals located more than 35 miles from another ED to convert to stand-alone EDs that would bill under the Outpatient Prospective Payment System (OPPS). Effectively they would become “outpatient-only” hospitals and would receive annual payments to assist with their fixed costs.

In contrast, MedPAC noted an oversupply of emergency services in urban areas, where stand-alone EDs—particularly those affiliated with nearby hospitals—may be shifting services from lower cost urgent care centers and physicians’ offices to higher cost 24/7 stand-alone EDs.

MedPAC reported that outpatient Medicare ED payments increased 72% per beneficiary between 2010 and 2016. A MedPAC press release attributed the growth in off-campus EDs in certain urban locations to “Medicare payment policy [rather] than unmet need for ED services.”

“I think [the MedPAC proposal] is a move in the right direction,” Renee Hsia, MD, MSc, Professor of Emergency Medicine and Institute of Health Policy Studies at the University of California-San Francisco, toldLeaders in Health Care. “We have to understand there are limited resources, and the fixed costs for stand-alone EDs are lower.” Hsia co-authored a report titled, “Don’t Hate the Player; Hate the Game,” published in the Annals of Emergency Medicine. In it she argues that “freestanding EDs will continue to proliferate in areas in which there are few restrictions, potentially creating more supply than demand.” (Photo copyright: University of California San Francisco.)

75% of Freestanding EDs within Six Miles of Hospital EDs

In April, MedPAC published an analysis of five healthcare markets—Charlotte, Cincinnati, Denver, Dallas, and Jacksonville, Fla. In “Using Payment to Ensure Appropriate Access to and Use of Hospital Emergency Department Services,” MedPAC showed that 75% of the freestanding EDs were located within six miles of a hospital emergency room. The average drive time to the nearest hospital was 10.3 minutes.

In that report, MedPAC proposed cutting payment rates 30% for off-campus stand-alone EDs located within six miles of an on-campus hospital emergency room. This proposal means off-campus EDs, which have lower standby costs and typically treat patients with less acute medical problems, would receive Medicare payment rates on par with ED facilities open less than 24/7. If the rate change is enacted, MedPAC estimates Medicare would save between $50 million and $250 million annually.

MedPAC’s recommendation drew the ire of the American Hospital Association (AHA) and other hospital industry stakeholders who believe a payment cut could result in off-campus stand-alone EDs closing. The AHA in March submitted a “comment letter” to MedPAC Executive Director James E. Mathews, PhD, calling the proposal “unfounded and arbitrary.”

“The recommendation is not based on any analysis of Medicare beneficiaries, Medicare costs, or Medicare payments, and would make Medicare’s record underpayment of outpatient departments and hospitals even worse,” Joanna Hiatt Kim, Vice President of Policy at the AHA, told Modern Healthcare. “Even more troubling to us is that [the recommendation] has the potential to reduce patient access to care, particularly in vulnerable communities, following a year in which hospital EDs responded to record-setting natural disasters and flu infections.”

This latest report indicates MedPAC believes shifting reimbursement toward different sites of care and for different services improves the ability of providers to be proactive and manage patients in ways that support earlier diagnosis and active management of conditions.

Medical laboratories and anatomic pathology groups should use this opportunity to create lab services that support these objectives and add value to both providers and patients.

UK study shows how LDTs may one day enable physicians to identify patients genetically predisposed to chronic disease and prescribe lifestyle changes before medical treatment becomes necessary

Could genetic predisposition lead to clinical laboratory-developed tests (LDTs) that enable physicians to assess patients’ risk for specific diseases years ahead of onset of symptoms? Could these LDTs inform treatment/lifestyle changes to help reduce the chance of contracting the disease?

A UK study into the genetics of one million people with high blood pressure reveals such tests could one day exist.

They also confirmed 274 loci (gene locations) and replicated 92 loci for the first time.

“This is the most major advance in blood pressure genetics to date. We now know that there are over 1,000 genetic signals which influence our blood pressure. This provides us with many new insights into how our bodies regulate blood pressure and has revealed several new opportunities for future drug development,” said Mark Caulfield, MD,

The researchers believe “this means almost a third of the estimated heritability for blood pressure is now explained,” the news release noted.

Clinical Laboratories May Eventually Get a Genetic Test Panel for Hypertension

Of course, more research is needed. But the study suggests a genetic test panel for hypertension may be in the future for anatomic pathologists and medical laboratories. Physicians might one day be able to determine their patients’ risks for high blood pressure years in advance and advise treatment and lifestyle changes to avert medical problems.

By involving more than one million people, the study also demonstrates how ever-growing pools of data will be used in research to develop new diagnostic assays.

The video above summarizes research led by Queen Mary University of London and Imperial College London, which found over 500 new gene regions that influence people’s blood pressure, in the largest global genetic study of blood pressure to date. Click here to view the video. (Photo and caption copyright: Queen Mary University of London.)

Genetics Influence Blood Pressure More Than Previously Thought

In addition to identifying hundreds of new genetic regions influencing blood pressure, the researchers compared people with the highest genetic risk of high blood pressure to those in the low risk group. Based on this comparison, the researchers determined that all genetic variants were associated with:

“having around a 13 mm Hg higher blood pressure;

“having 3.34 times the odds for increased risk of hypertension; and,

“1.52 times the odds for increased risk of poor cardiovascular outcomes.”

“We identify 535 novel blood pressure loci that not only offer new biological insights into blood pressure regulation, but also highlight shared genetic architecture between blood pressure and lifestyle exposures. Our findings identify new biological pathways for blood pressure regulation with potential for improved cardiovascular disease prevention in the future,” the researchers wrote in Nature Genetics.

Other Findings Link Known Genes and Drugs to Hypertension

The UK researchers also revealed the Apolipoprotein E (ApoE) gene’s relation to hypertension. This gene has been associated with both Alzheimer’s and coronary artery diseases, noted LabRoots. The study also found that Canagliflozin, a drug used in type 2 diabetes treatment, could be repurposed to also address hypertension.

“Identifying genetic signals will increasingly help us to split patients into groups based on their risk of disease,” Paul Elliott, PhD, Professor, Imperial College London Faculty of Medicine, School of Public Health, and co-lead author, stated in the news release. “By identifying those patients who have the greatest underlying risk, we may be able to help them to change lifestyle factors which make them more likely to develop disease, as well as enabling doctors to provide them with targeted treatments earlier.”

Working to Advance Precision Medicine

The study shares new and important information about how genetics may influence blood pressure. By acquiring data from more than one million people, the UK researchers also may be setting a new expectation for research about diagnostic tests that could become part of the test menu at clinical laboratories throughout the world. The work could help physicians and patients understand risk of high blood pressure and how precision medicine and lifestyle changes can possibly work to prevent heart attacks and strokes among people worldwide.

PwC’s list of 12 factors that will shape the healthcare landscape in 2018 calls attention to many new innovations Dark Daily has reported on that will impact how medical laboratories perform their tests

PwC’s Health Research Institute (HRI) issued its annual report, detailing the 12 factors expected to impact the healthcare industry the most in 2018. Dark Daily culled items from the list that will most likely impact clinical laboratories and anatomic pathology groups. They include:

How clinical laboratory leaders respond to these items could, in part, be determined by new technologies.

AI Is Everywhere, Including in the Medical Laboratory

Artificial intelligence is becoming highly popular in the healthcare industry. According to an article in Healthcare IT News, business executives who were polled want to “automate tasks such as routine paperwork (82%), scheduling (79%), timesheet entry (78%), and accounting (69%) with AI tools.” However, only about 20% of the executives surveyed have the technology in place to use AI effectively. The majority—about 75%—plan to invest in AI over the next three years—whether they are ready or not.

One such example of how AI could impact clinical laboratories was demonstrated by a recent advancement in microscope imaging. Researchers at the University of Waterloo (UW) developed a new spectral light fusion microscope that captures images in full color and is far less expensive than microscopes currently on the market.

“In medicine, we know that pathology is the gold standard in helping to analyze and diagnose patients, but that standard is difficult to come by in areas that can’t afford it,” Alexander Wong, PhD, one of the UW researchers, told CLP.

“The newly developed microscope has no lens and uses artificial intelligence and mathematical models of light to develop 3D images at a large scale. To get the same effect using current technologies—using a machine that costs several hundred thousand dollars—a technician is required to ‘stitch together’ multiple images from traditional microscopes,” CLP noted.

Healthcare Intermediaries Could Become Involved with Clinical Laboratory Data

Pricing is one of the biggest concerns for patients and government entities. This is a particular concern for the pharmaceutical sector. PwC’s report notes that “stock values for five of the largest intermediaries in the pharmacy supply chain have slumped in the last two years as demands for lower costs and better outcomes have intensified.”

Thus, according to PwC, pressure may come to bear on intermediaries such as Pharmacy Benefit Managers (PBMs) and wholesalers, to “prove value and success in creating efficiencies or risk losing their place in the supply chain.”

Similar pressures to lower costs and improve efficiency are at work in the clinical laboratory industry as well. Dark Daily reported on one such cost-cutting measure that involves shifting healthcare payments toward digital assets using blockchains. The technology digitally links trusted payers and providers with patient data, including medical laboratory test results. (See, “Blockchain Technology Could Impact How Clinical Laboratories and Pathology Groups Exchange Lab Test Data,” September 29, 2017.)

PwC’s latest report predicts 12 forces that will continue to impact healthcare, including clinical laboratories and anatomic pathology groups, in 2018. Click on the image of the cover above to access an online version of the report. (Photo copyright: PwC/Issuu.)

The Opioid Crisis Remains at the Forefront

Healthcare will continue to feel the impact of the opioid crisis, according to the PwC report. Medical laboratories will continue to be involved in the diagnosis and treatment of opioid addition, which has garnered the full attention of the federal government and has become a multi-million-dollar industry.

Security Remains a Concern

Cybersecurity will continue to impact every facet of healthcare in 2018. Healthcare IT News reported, “While 95% of provider executives believe their organization is protected against cybersecurity attacks, only 36% have access management policies and just 34% have a cybersecurity audit process.”

Patients are aware of the risks and are often skeptical of health information technology (HIT), Dark Daily reported in June of last year. Clinical laboratories must work together with providers and healthcare organizations to audit their security measures. Recognizing the importance of the topic, the National Independent Laboratory Association (NILA) has named cybersecurity for laboratory information systems (LIS) a focus area.

Patient Experience a Priority

Although there have been significant improvements in the area of administrative tasks, there is still an enormous demand for a better patient experience, including in clinical laboratories. Healthcare providers want patients to make changes for the better that ultimately improve outcomes and the patient experience is one path toward that goal.

As they follow healthcare reform guidelines to increase quality while lowering costs, state governments will continue to ramp up pressure on healthcare providers and third parties in the area of pricing. Rather than simply requiring organizations to report on pricing, states are moving towards legislating price controls, as Dark Daily reported in February.

Social Factors Affect Healthcare Access

The transition to value-based care makes the fact that patients’ socioeconomic statuses matter when it comes to their health. “The most important part of getting good results is not the knowledge of the doctors, not the treatment, not the drug. It’s the logistics, the social support, the ability to arrange babysitting,” David Berg, MD, co-founder of Redirect Health told PwC.

One such transition that is helping patients gain access to healthcare involves microhospitals and their adoption of telemedicine technologies, which Dark Daily reported on in March.

“Right now, they seem to be popping up in large urban and suburban metro areas,” Priya Bathija, Vice President, Value Initiative American Hospital Association, told NPR. “We really think they have the potential to help in vulnerable communities that have a lack of access.”

“Physician decision-support software utilizes medical laboratory test data as a significant part of a full dataset used to guide caregivers,” Dark Daily noted. “Thus, if the FDA makes it easier for developers to get regulatory clearance for these types of products, that could positively impact medical labs’ ability to service their client physicians.”

Healthcare Delivery During and Following Natural Disasters

PwC predicts the long-term physical results, financial limitations, and supply chain disruptions following natural disasters will continue to affect healthcare in 2018. The devastation can prevent many people from receiving adequate, timely healthcare.

PwC’s report is an important reminder of from where the clinical laboratory/anatomic pathology industry has come, and to where it is headed. Sharp industry leaders will pay attention to the predictions contained therein.

Clinical laboratories may want to offset plunging patient lab specimens by increasing outreach business

Hospital admissions are in decline across the country and the trend is being blamed in part on the rising use of high-deductible health plans (HDHP). The implications for hospital-based clinical laboratories is that lower in-patient totals reduce the flow of patient lab specimens as well. This situation may encourage some hospital and health-system labs to increase their lab outreach business as a way to offset declining inpatient lab test volumes and help keep down overall average test costs.

Healthcare Dive, which named “changing patient admissions” its “Disruptor of the Year,” used data from America’s Health Insurance Plans (AHIP) annual surveys to show the admission rate trend that is causing hospital operators and health systems to rethink how they do business going forward.

“We are really talking about how providers are not taking in as much revenue as they are spending,” Healthcare Dive noted. “Hospitals are largely fixed cost businesses, and rising expenses have been outpacing admissions growth.”

Experts Claim the ‘Hand Writing Is on the Wall’

According to Healthcare Dive’s analysis of US hospital admissions, which used data from the American Hospital Association’s Annual Survey, hospital admissions peaked at 35.4 million in 2013, coinciding with the roll out of the Affordable Care Act. The total fell to 34.9 million in 2014, before rebounding slightly to 35.1 million in 2015. The 2016 survey, published in 2018, showed hospital admissions remaining relatively flat at approximately 35.2 million.

Paul Hughes-Cromwick (above), Co-Director, Sustainable Health Spending Strategies, Altarum in Ann Arbor, Mich., expects hospitals to be challenged by flat admission rates going forward. “Times are still pretty good, but the writing is on the wall for hospital operators,” he told Modern Healthcare. This will impact clinical laboratories owned by hospitals and health systems as well. Photo copyright: Long Beach Business Journal.)

Most experts place the blame for slumping patient admissions on HDHPs. Such plans, which are paired with a tax-advantaged health savings account, have enabled employers to shift initial medical costs to workers in exchange for lower monthly health insurance premiums. Nearly 20.2 million Americans were enrolled in HDHPs in 2016, up from 15.4 million in 2013 and far above the roughly one million plans in existence in 2005, the AHIP surveys revealed. HDHPs were first authorized by Congress in 2003.

Consumers Delaying or Opting Out of Healthcare

Faced with higher out-of-pocket medical costs, consumers are opting to postpone or forgo elective surgeries and procedures, which in turn is placing pressure on healthcare systems’ operating revenues.

According to Healthcare Dive, Community Health Systems experienced a 12% drop in operating revenue in the first nine months of fiscal year 2017, while HCA Healthcare and Tenet Healthcare dropped 6.7% and 3.8%, respectively.

J. Eric Evans, President of Hospital Operations, Tenet Healthcare (NYSE:THC), a 77-hospital chain, told Modern Healthcare, today’s consumers are spending their healthcare dollars differently.

“The more elective procedures, things like orthopedics, we see the softness,” Evans told Modern Healthcare. “So, we think that does play into the story of deductibles rising and changing behaviors.”

The challenges for not-for-profit hospital systems are no different. Modern Healthcare noted that the 14-hospital Indiana University Health system reported a 46% drop in operating income in the third quarter of FY 2017 on a year-over-year admission decline of 2%.

Healthcare Systems Rethinking Their Business Strategies

“Health systems en masse are reacting to shifting dynamics in healthcare utilization by throwing money and resources to lower cost settings, such as urgent care centers and freestanding emergency departments,” Healthcare Dive noted. Dark Daily has reported on this trend. (See, “From Micro-hospitals to Mobile ERs: New Models of Healthcare Create Challenges and Opportunities for Pathologists and Medical Laboratories,” May 26, 2017.) Health systems also are selling unprofitable hospitals and laying off or eliminating positions to cut costs. Tenet Healthcare, for example, is laying off 2,000 workers while selling eight of its US hospitals and all of its nine United Kingdom facilities, Modern Healthcare reported in January.

“We are seeing and are working with health systems to take out pretty significant amounts of cost out of their operations, both clinical and nonclinical, and setting targets like 15-20%, which is a transformative change,” Igor Belokrinitsky, Vice President and Partner at Strategy&, PricewaterhouseCoopers’ strategy consulting group, told Healthcare Dive in a 2017 interview.

Lower hospital in-patient volume means less clinical laboratory test orders. This, in turn, will result in increases in the average cost per inpatient test. Anatomic pathology groups and medical laboratory leaders who work in or service hospitals may wish to take proactive steps to boost test referrals from outpatient and outreach settings as a way to help keep down the lab’s average cost per test.