Another report finds nearly half of all healthcare systems planning to opt out of Medicare Advantage plans because of issues caused by prior authorization requirements

Prior-authorization is common and neither healthcare providers (including clinical laboratories) nor Medicare Advantage (MA) health plans are happy with the basic process. Thus, labs—which often must get prior-authorization for molecular diagnostics and genetic tests—may learn from a recent KFF study of denial rates and successful appeals.

“While prior authorization has long been used to contain spending and prevent people from receiving unnecessary or low-value services, it also has been [the] subject of criticism that it may create barriers to receiving necessary care,” KFF, a health policy research organization, stated in a news release.

Nearly all MA plan enrollees have to get prior authorization for high cost services such as inpatient stays, skilled nursing care, and chemotherapy. However, “some lawmakers and others have raised concerns that prior authorization requirements and processes, including the use of artificial intelligence to review requests, impose barriers and delays to receiving necessary care,” KFF reported.

“Insurers argue the process helps to manage unnecessary utilization and lower healthcare costs. But providers say prior authorization is time-consuming and delays care for patients,” Healthcare Dive reported.

“There are a ton of barriers with prior authorizations and referrals. And there’s been a really big delay in care—then we spend a lot of hours and dollars to get paid what our contracts say,” said Katie Kucera (above),Vice President and CFO, Carson Tahoe Health, Carson City, Nev., in a Becker’s Hospital CFO Report which shared the health system’s plan to end participation in UnitedHealthcare commercial and Medicare Advantage plans effective May 2025. Clinical laboratories may want to review how test denials by Medicare Advantage plans, and the time cost of the appeals process, affect the services they provide to their provider clients. (Photo copyright: Carson Tahoe Health.)

Key Findings of KFF Study

To complete its study, KFF analyzed “data submitted by Medicare Advantage insurers to CMS to examine the number of prior authorization requests, denials, and appeals for 2019 through 2022, as well as differences across Medicare Advantage insurers in 2022,” according to a KFF issue brief.

Here are key findings:

Requests for prior authorization jumped 24.3% to 46 million in 2022 from 37 million in 2019.

More than 90%, or 42.7 million requests, were approved in full.

About 7.4%, or 3.4 million, prior authorization requests were fully or partially denied by insurers in 2022, up from 5.8% in 2021, 5.6% in 2020, and 5.7% in 2019.

About 9.9% of denials were appealed in 2022, up from 7.5% in 2019, but less than 10.2% in 2020 and 10.6% in 2021.

More than 80% of appeals resulted in partial or full overturning of denials in the years studied. Still, “negative effects on a person’s health may have resulted from delay,” KFF pointed out.

KFF also found that requests for prior authorization differed among insurers. For example:

Humana experienced the most requests for prior authorization.

Among all MA plans, the share of patients who appealed denied requests was small. The low rate of appeals may reflect Medicare Advantage plan members’ uncertainty that they can question insurers’ decisions, KFF noted.

It’s a big market. Nevertheless, “between onerous authorization requirements and high denial rates, healthcare systems are frustrated with Medicare Advantage,” according to a Healthcare Financial Management Association (HFMA) survey of 135 health system Chief Financial Officers.

According to the CFOs surveyed, 19% of healthcare systems stopped accepting one or more Medicare Advantage plans in 2023, and 61% are planning or considering ending participation in one or more plans within two years.

“Nearly half of health systems are considering dropping Medicare Advantage plans,” Becker’s reported.

Federal lawmakers acted, introducing three bills to help improve timeliness, transparency, and criteria used in prior authorization decision making. Starting in 2023, KFF reported, the federal Centers for Medicare and Medicaid Services (CMS) published final rules on the bills:

Rule One (effective June 5, 2023), “clarifies the criteria that may be used by Medicare Advantage plans in establishing prior authorization policies and the duration for which a prior authorization is valid. Specifically, the rule states that prior authorization may only be used to confirm a diagnosis and/or ensure that the requested service is medically necessary and that private insurers must follow the same criteria used by traditional Medicare. That is, Medicare Advantage prior authorization requirements cannot result in coverage that is more restrictive than traditional Medicare.”

Rule Two (effective April 8, 2024), is “intended to improve the use of electronic prior authorization processes, as well as the timeliness and transparency of decisions, and applies to Medicare Advantage and certain other insurers. Specifically, it shortens the standard time frame for insurers to respond to prior authorization requests from 14 to seven calendar days starting in January 2026 and standardizes the electronic exchange of information by specifying the prior authorization information that must be included in application programming interfaces starting in January 2027.”

Rule Three (effective June 3, 2024), requires “Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors starting with plan year 2025.”

KFF’s report details how prior authorization affects patient care and how healthcare providers struggle to get paid for services rendered by Medicare Advantage plans amid the rise of value-based reimbursements.

Clinical laboratory leaders may want to analyze their test denials and appeals rates as well and, in partnership with finance colleagues, consider whether to continue contracts with Medicare Advantage health plans.

Price shopping for clinical laboratories and other healthcare services and surgical procedures creates a ‘healthy competitive environment,’ an Optum executive noted

One example, SmartShopper by Vitals (now known as Sapphire Digital) of Lyndhurst, N.J., is a pre-paid employer- or health plan-based program that lets people use mobile phone apps and go online using their computers to check prices and quality ratings for healthcare service providers in their area. The program may also incentivize members to prices shop by offering up to $500 per service for choosing lower-cost providers.

“Today, there is no reason consumers shouldn’t know the price of routine, non-emergency care,” said Heyward Donigan, former President and CEO of Vitals who is now CEO of Rite Aid (NYSE:RAD), in a news release. “Putting consumers in the driver’s seat for making informed healthcare decisions will create a competitive healthcare marketplace that ultimately lowers costs for everyone.”

Does Price Shopping Create a ‘Healthy Competitive Environment’?

Individuals whose health plans or employers have signed up

for SmartShopper can use it to seek out the best prices for routine exams,

preventative exams, imaging scans, and to schedule surgeries. The program’s

provider data is compared by cost and quality based on nationally recognized

metrics and patient reviews.

Some of the largest health insurers in the country, such as Anthem and Highmark, provide price

shopping tools to their clients.

“Up to 7% of overall healthcare spent could be reduced through price transparency tools like SmartShopper,” Becca Lococo, PhD, Vice President, Customer Experience at Optum, told Modern Healthcare. This can create a really healthy competitive environment in an industry where costs are already rising.”

Employers Save Big with Price Shopping

Large companies can reap substantial savings when they

provide their employees with price shopping tools. Employer savings can range

from $1,810 for a round of physical therapy to $80 for a mammogram. Patients,

on average, save $606 for each procedure with SmartShopper, reported Modern

Healthcare.

“Even just one person shopping can make a difference for

that employer in terms of the claims they’d be paying out at the end,” Steve Crist, Vice

President, Commercial Health Plan, Blue

Cross Blue Shield of North Carolina, told Modern Healthcare. “Even

though the employer is paying the incentive, the cost savings more than make up

for it. The ROI on this program is very strong.”

The Vitals SmartShopper Book of Business Report 2017 notes that, between 2014 and 2017, the tool saved employers $40 million and paid out $4.6 million in cash rewards to individual consumers. In 2016 alone, SmartShopper saved employers $15 million and paid out $1.8 million in cash incentives with the average incentive check totaling $85.

The Vitals report also listed the top 10 procedures and the

three-year total cost savings for employers that used SmartShopper. The list

includes clinical laboratory testing as the fifth largest source of savings for

employers that used price-transparency tools as part of their health benefits

programs:

SmartShopper has a configurable list of more than 200

medical procedures and services included in the tool. Sapphire Digital

(formerly Vitals) uses claims data and collaborates with clients to develop the

ideal combination of services to maximize savings for their customers.

“We don’t have to boil the ocean to produce a sizeable reduction in healthcare costs for our employer clients,” said Heyward Donigan, former President and CEO of Vitals and now CEO of Rite-Aid, in the Vitals report. “Focusing on routine, shoppable procedures that are relevant to the demographics of a client’s workforce generates significant savings.” (Photo copyright: Wall Street Journal.)

Price Shopping for Surgery

In 2018, before changing its name to Sapphire Digital, Vitals sold its consumer services division to WebMD. The sale enabled Vitals to focus on enhancing and developing its price transparency tools. The company then launched Medical Expertise Guide (MEG), which uses advanced analytics to create “proprietary Composite Quality Scores for surgeons and facilities to help consumers find the best surgeon and facility combination for their surgery, at a predictable cost,” according to Sapphire Digital’s website.

“MEG brings consumers information, powered by data and

analytics and supported by personalized service, to help them make quality

healthcare decisions with confidence,” said Donigan, in a news

release. “MEG guides employees to the best care, while helping employers

manage the overall cost-effectiveness of their healthcare program.”

Examples presented in the news release of the “savings per case”

for people using MEG include:

In October 2016, Dark Daily reported on another example of using healthcare transparency tools from Castlight Health. That tool enables Safeway employees to check clinical laboratory prices on their smartphones or computers before selecting where to have tests performed. At that time, Safeway and its employees were able to reduce spending on clinical laboratory tests by 32% in only 24 months by selecting the labs with the lowest prices.

The examples presented above are evidence that price

transparency is gaining a foothold in healthcare. These are early

demonstrations that price shopping tools do help consumers make more informed

decisions when choosing hospitals, physicians, or clinical laboratories. The

trend is for ever-growing numbers of consumers to rely on pricing transparency

tools when selecting their medical care.

Pathologists and clinical laboratories should not ignore

this trend, as it could affect business workflow and revenue streams.

By negotiating directly with healthcare providers, employers cut health insurers out of the loop, at least for certain specified healthcare conditions and surgeries

It’s a new trend in how employers provide healthcare benefits for their employees. In order to save money, a growing number of employers are going to low-cost hospitals, physicians, and other providers to contract directly for their services. This may be the opening that allows some clinical laboratories to approach larger employers in their region and negotiate pricing and contract terms without the need to involve a health insurer.

What’s motivating more employers to reach out and contract directly with low-cost healthcare providers is the realization that their health insurance plan typically pays much more than Medicare to hospitals, physicians, clinical laboratories, and other ancillary providers. This fact is supported by a study conducted by the Rand Corporation that found “large employers generally lack useful information about the prices they are paying for healthcare services,” and that of the 1,600 hospitals in 25 states that Rand surveyed, “employer-sponsored health plans paid hospitals an average of 241% of what Medicare would have paid for the same inpatient and outpatient services in 2017,” which is up from 236% of Medicare in 2015, Modern Healthcare reported.

Thus, to better control the skyrocketing cost of healthcare,

and the health benefits plan they offer their employees, employers are

increasingly turning to self-coverage and implementing company benefits plans

that reward employees for price shopping and for selecting the lowest costs

healthcare services.

This trend is another reason why clinical laboratory leaders should be tracking changes in federal price transparency requirements, along with the increased consumer interest in accessing healthcare prices in advance of service.

Employers Negotiate Directly for Healthcare Services

Innovative employer plans to decrease healthcare costs

include:

Contracting directly with medical providers,

Opening primary care clinics within their

corporate facilities,

Referring employees to contracted providers for certain

procedures, and

Creating bundled-payment deals with select

providers.

Modern Healthcare reports that both public and

private employers in five states (Colorado, Connecticut, Michigan, Montana,

Texas, and Wisconsin) are “considering or launching group purchasing

initiatives with narrow- or tiered-network plans, onsite primary-care clinics,

and contracts with advanced primary-care providers,” as well as “direct-contracting

with providers, such as referring employees to designated centers of excellence

for some procedures and conditions under bundled-payment deals with warrantied

results.”

Cheryl DeMars, CEO of The Alliance, a Wisconsin healthcare purchasing cooperative, says there is a movement afoot. “I’m seeing a level of boldness on the part of our members that I haven’t seen before in my 27 years here,” she told Modern Healthcare.

“Almost 100 million employees covered through self-insured plans not only represents a staggeringly large market for healthcare cost containment, it is an extraordinary opportunity for America to meaningfully reduce our national healthcare bill,” Kirk Fallbacher (above), President and CEO of Advanced Medical Pricing Solutions (AMPS) told Healthcare Finance News. (Photo copyright: NextGenRBP.com)

Self-insured Employers can Reduce the Nation’s Healthcare

Bill, says KFF

A 2018 US Census Bureau report states that more than 181 million people in the US were enrolled in employer-sponsored health plans in 2017, and that the estimated average premium for employer-sponsored family coverage increased at an annual rate of 4.5% from 2008 to 2019.

That increase was approximately twice the rate of overall

inflation and growth in average hourly earnings during the same time period, according

to the report, which also states that the surge in premiums was driven by price

increases for medical services and that use of most healthcare services among

employees has actually been declining.

For US employers, “the steep increase in their healthcare

cost crowds out financial resources that could be used for employee wage

increases, capital investments, and other spending priorities, such as

retirement plans,” the report notes.

However, an estimated 94 million of the 156 million workers in the US—approximately 61%—are currently covered under a self-insured medical plan through their employer, the KFF Employer Health Benefits 2019 Annual Survey states.

Healthcare.gov defines the self-insured health insurance plan as a “type of plan usually present in larger companies where the employer itself collects premiums from enrollees and takes on the responsibility of paying employees’ and dependents’ medical claims. These employers can contract for insurance services such as enrollment, claims processing, and provider networks with a third-party administrator, or they can be self-administered.”

“It doesn’t signal the end of the insurance industry,” he

said. “On the cost side of the equation, the PPO approach is beginning to come

to an end. The costs are outstripping inflation and wages.”

Moving to self-insurance is another part of the current trend for price transparency in the healthcare industry and may offer opportunities for clinical laboratories to increase profits. Clinical laboratories and anatomic pathology groups might want to contact the Human Resources Departments of local major employers to educate them on the costs and quality value of their labs. Such a proactive and innovative move could encourage employers to include those labs in the provider networks of their self-insured health benefit plans.

Clinical laboratory leaders are aware that reference pricing is a tool employers and health insurer can use to reduce the wide variation different providers charge for the same clinical service. In 2016 our sister publication, The Dark Report, devoted an entire issue to the subject of reference pricing. (See TDR, “The Newest Threat to Lab Revenues: Reference Pricing in Healthcare,” September 6, 2016.)

The Dark Report wrote about the reference pricing pilot conducted by Safeway, the grocery chain, in collaboration with Anthem, Inc. (NYSE:ANTM), the large health insurance company. The reference pricing program had these elements:

When Safeway employees and their beneficiaries chose a lab that priced its tests below the 60th percentile, the patient qualified for the health plan’s benefits. But if the patient chose a lab with test prices above the 60th percentile, that patient was responsible for the full cost of the test.

Safeway employees and their beneficiaries were given a real-time price checking tool that they could access by web browser and smart phone. This app, developed by Castlight Health, Inc., of San Francisco, showed the prices each lab in the Safeway/Anthem network charged for the same lab test, along with the percentile price of that test.

As reported in JAMA Internal Medicine, Safeway introduced reference pricing into its health insurance design for 15,000 employees in 2011. Three years later, the company and its employees were spending 32% less for clinical laboratory tests and saved $2.57 million during the years 2011 to 2013.

The reference pricing program at Safeway, which focused

primarily on clinical laboratory testing, succeeded because of the large

variability in how different labs price the same tests. For example, as TDR

reported:

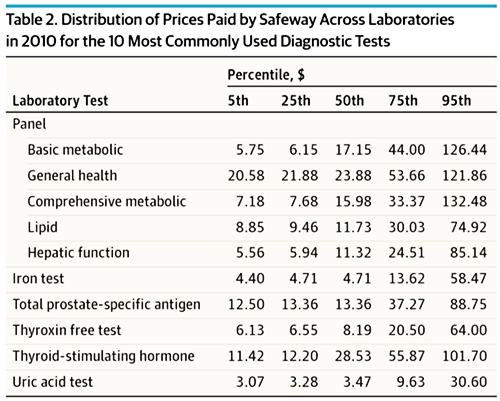

For a basic metabolic panel, which was the most

commonly prescribed test, prices among different labs ranged from $5.75 to

$126.44; and

Prices for a lipid panel ranged from $8.85 to

$74.92.

The graphic above, taken from the Safeway/Anthem observational study of “changes in laboratory pricing and selection by employees … before and after a reference pricing policy for laboratory services,” illustrates the wide range of prices Safeway paid for the 10 most common clinical laboratory tests. (Graphic copyright: American Medical Association/JAMA Internal Medicine.)

Typically, a reference pricing arrangement is done to lower

costs, decrease disparities in pricing for similar medical services, and make

health plans more attractive to employers. This is why state health plans are

looking at implementing reference price reimbursement models as a way to reduce

healthcare costs for state employees and other beneficiaries.

North Carolina Providers Respond Negatively to State Reference

Pricing Plan

North Carolina’s State Health Plan encountered resistance

from the state’s medical community when it attempted to implement a similar

reference-price reimbursement model.

The state’s health plan covers more than 727,000

beneficiaries, including teachers, state employees, retired employees, and

their dependents. It is overseen by the State Treasurer and administered by BlueCross

BlueShield of North Carolina (Blue Cross NC).

In October 2018, North Carolina’s state health plan board of

trustees unanimously approved the Clear

Pricing Project, a reference-pricing program championed by State Treasurer Dale Folwell. A 2019 Blue

Cross NC State Health Plan Network Master Reimbursement Exhibit document

states, beginning in 2020, most hospitals would get 160% of the Medicare rate

for inpatient services and 230% for outpatient services; rural providers would

get more.

Pricing for medical lab and pathology services also was set

at 160% of the Medicare rate. The document states, “Except for services

identified by Medicare as CLIA Excluded or CLIA Waiver,

In-Office Laboratory Service fees will be limited to those services for which

you have provided Blue Cross and Blue Shield of North Carolina with evidence of

CLIA

certification.”

North Carolina’s healthcare providers had no choice but to

agree to the pricing to be included in the state’s provider network, but they

were not happy about the arrangement.

NCHA Warns Hundreds of Providers Could Be Pushed Out of

Network

Hospitals countered with a public relations and lobbying

campaign through the North Carolina Healthcare

Association (NCHA). Soon after Folwell’s announcement, the NCHA issued a

statement claiming that his plan “could force hundreds of providers out of

the State Health Plan network or out of business.” The NCHA estimated the

potential losses to hospitals and health systems at “upwards of $400 million.”

In the statement, NCHA President Steve

Lawler said, “We believe the treasurer is not being transparent about what

this proposal will do to state health plan members and their families.”

As an alternative, the NCHA proposed that the state examine

value-based approaches such as “case management, outcomes-based payment models,

and member education as ways to manage costs.”

The organization established a web page explaining its opposition

to the state’s plan and pushed for legislation that would delay its

implementation. House

Bill 184, which sought to delay implementation of the state’s healthcare

reimbursement plan, passed the state House of Representatives in April, before

stalling in the Senate in May, North

Carolina Health News reported.

Many providers simply refused to sign the necessary

contracts, Modern

Healthcare reported, even after Folwell agreed to increase the average

rate to 196%. In August, he relented and announced that for 2020, the provider

network will consist of the North Carolina State Health Plan Network—28,000

providers that had signed on to the Clear Pricing Project—plus the Blue Options

PPO Network, which includes providers that had not agreed to the new pricing.

That makes for a total of more than 68,000 providers, states

a news

release from the treasurer’s office. After the change was announced,

providers in the State Health Plan Network were permitted to revert to the Blue

Options PPO Network rates.

States may approach implementing reference pricing in

different ways, which will likely lead to a distinct disparity in outcomes. Nevertheless,

whatever approach is used, medical laboratories and pathology groups will want

to understand how reference pricing works and how it may be implemented in

their states.

Armed with that understanding, they may want to pursue a

proactive strategy of aligning the prices of their lab tests to be at the 50th percentile

or lower to avoid being the highest-priced labs in their communities and

regions.

Following the raid, the company’s co-founders resigned

from the board of directors

Microbiome testing company, uBiome, a biotechnology developer that offers at-home direct-to-consumer (DTC) test kits to health-conscious individuals who wish to learn more about the bacteria in their gut, or who want to have their microbiome genetically sequenced, has recently come under investigation by insurance companies and state regulators that are looking into the company’s business practices.

CNBC

reported that the Federal Bureau of

Investigation (FBI) raided the company’s San Francisco headquarters in

April following allegations of insurance fraud and questionable billing

practices. The alleged offenses, according to CNBC, included claims that

uBiome routinely billed patients for tests multiple times without consent.

Becker’s

Hospital Review wrote that, “Billing documents obtained by The Wall Street

Journal and described in a June 24 report further illustrate uBiome’s

allegedly improper billing and prescribing practices. For example, the

documents reportedly show that the startup would bill insurers for a lab test

of 12 to 25 gastrointestinal pathogens, despite the fact that its tests only

included information for about five pathogens.”

Company Insider Allegations Trigger FBI Raid

In its article, CNBC stated that “company insiders”

alleged it was “common practice” for uBiome to bill patients’ insurance

companies multiple times for the same test.

“The company also pressured its doctors to approve tests

with minimal oversight, according to insiders and internal documents seen by CNBC.

The practices were in service of an aggressive growth plan that focused on

increasing the number of billable tests served,” CNBC wrote.

FierceBiotech reported that, “According to previous

reports, the large insurers Anthem, Aetna, and Regence BlueCross BlueShield

have been examining the company’s billing practices for its physician-ordered

tests—as has the California Department of Insurance—with probes focusing on

possible financial connections between uBiome and the doctors ordering the

tests, as well as rumors of double-billing for tests using the same sample.”

Becker’s Hospital Review revealed that when the FBI

raided uBiome they seized employee computers. And that, following the raid,

uBiome had announced it would temporarily suspend clinical operations and not

release reports, process samples, or bill health insurance for their services.

The company also announced layoffs and that it would stop

selling SmartJane and SmartGut test kits, Becker’s reported.

uBiome Assumes New Leadership

Following the FBI raid, uBiome placed its co-founders Jessica

Richman (CEO) and Zac

Apte (CTO) on administrative leave while conducting an internal

investigation (both have since resigned from the company’s board of directors).

The company’s board of directors then named general counsel, John Rakow, to be interim CEO,

FierceBiotech

reported.

John Rakow (center) is shown above with uBiome co-founders Jessica Richman (lower left) and Zac Apte (lower right). In a company statement, Rakow stressed that he believed in the company’s products and ability to survive the scandal. His belief may be based on evidence. Researchers have been developing tests based on the human microbiome for everything from weight loss to predicting age to diagnosing cancer. Such tests are becoming increasingly popular. Dark Daily has reported on this trend in multiple e-briefings. (Photo copyrights: LinkedIn/uBiome.)

After serving two months as the interim CEO, Rakow resigned

from the position. The interim leadership of uBiome was then handed over to

three directors from Goldin

Associates, a New York City-based consulting firm, FierceBiotech

reported. They include:

SmartFlu: a nasal microbiome swab that detects bacteria and viruses associated with the flu, the common cold, and bacterial infections.

What Went Wrong?

Richman and Apte founded uBiome in 2012 with the intent of

marketing a new test that would prove a link between peoples’ microbiome and their

overall health. The two founders initially raised more than $100 million from

venture capitalists, and, according to PitchBook,

uBiome was last valued at around $600 million, Forbes

reported.

Nevertheless, as a company, uBiome’s future is uncertain. Of

greater concern to clinical laboratory leaders is whether at-home microbiology

self-test kits will become a viable, safe alternative to tests traditionally performed

by qualified personnel in controlled laboratory environments.