Two national studies find pathologists bill out-of-network more frequently than other hospital-based specialties, and one study links that behavior to insurer reimbursement rates

Surprise bills for out-of-network services continue to be an important issue for healthcare consumers. Now comes a recently-released report from the Health Care Cost Institute (HCCI) claiming that pathologists are the specialists that most often bill for out-of-network hospital charges.

The HCCI study examined the prevalence and frequency of out-of-network billing among six specialties. The sample used for the report included 13.8 million healthcare visits to over 35 thousand hospital-based healthcare providers that occurred in 2017. The types of visits examined for the report were:

emergency medicine,

pathology,

radiology,

anesthesiology,

behavioral health, and

cardiovascular services.

The researchers calculated the percentage of out-of-network claims for both inpatient and outpatient visits to each type of the six specialties.

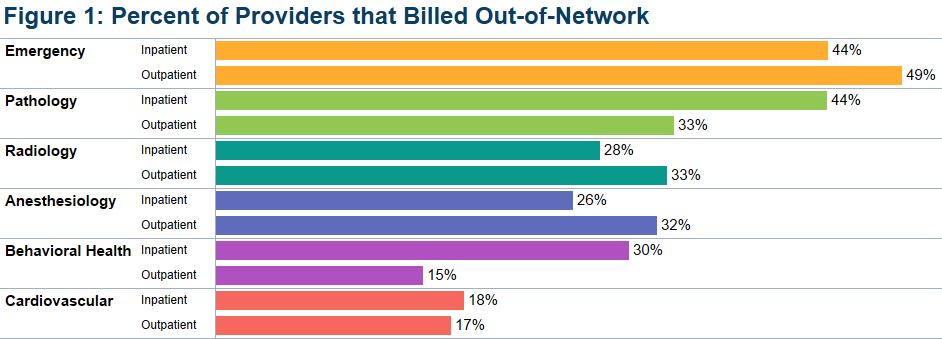

The study found that, overall, less than half of the specialties billed out-of-network for services obtained at in-network facilities. Providers with at least one out-of-network claim associated with an in-network outpatient visit ranged from 15% for behavioral health to 49% for emergency medicine.

Pathologists’ Out-of-Network Billing

Among the pathologists surveyed, HCCI found 33% had at least one out-of-network claim for an in-network outpatient visit. Providers with at least one out-of-network claim associated with an in-network inpatient visit ranged from 18% for cardiovascular services to 44% for both emergency and pathology services.

HCCI researchers also examined how often individual providers in the six specialties billed out-of-network at least one time and found that the majority billed out of network less than 10% of the time. However, this varied among the specialties with 36% of pathologists who billed out-of-network for inpatient visits, and 20% of pathologists who billed out-of-network for outpatient visits, did so more than 90% of the time.

The graphic above, taken from the latest HCCI report, shows “the share of providers who billed out-of-network at least once for inpatient and outpatient visits” and illustrates the percentage of out-of-network billings by pathologists compared to other hospital-based healthcare specialties. (Graphic copyright: Health Care Cost Institute.)

Pathologists Top List of Out-of-Network Specialists in Previous HCCI report

Last November, HCCI released a similar report that examined the commonality of out-of-network billing for the same six specialties plus surgical services that took place in 2017. Based on their collected data, they also estimated the amount of surprise bills that patients could expect to receive for those services.

That report found that nationally:

16.5% of visits with emergency room services had an out-of-network claim from an emergency medicine specialist.

12.9% of visits with lab/pathology services had an out-of-network claim from a pathologist.

8.3% of visits with anesthesiology services had an out-of-network claim from an anesthesiologist.

6.7% of visits with behavioral health services had an out-of-network claim from a behavioral health provider.

4.2% of visits with radiology services had an out-of-network claim from a radiologist.

2.1% of visits with surgical services had an out-of-network claim from a surgeon.

2.0% of visits with cardiovascular services had an out-of-network claim from a cardiovascular specialist.

Surgical Services the Most Expensive Out-of-Network Bill

This study also found broad variation in charges between types of services and healthcare settings. The researchers determined that the potential surprise bills for surgical visits due to out-of-network claims were of the greatest magnitude. HCCI estimated that the average potential surprise bill associated with an inpatient surgery was $22,248, while the potential surprise bill associated with an outpatient surgery was $8,493.

Out-of-Network Surprise Billing Varies Widely Depending on Location

The data was further broken down by state. For pathology services, the percentage of visits with out-of-network services in 2017 ranged from 0.3% in Minnesota to 75.3% in Kansas. HCCI researchers estimated the potential surprise bill for out-of-network pathology claims for inpatient services ranged from $14 in Louisiana to $167 in Delaware. The estimated surprise bill for out-of-network outpatient pathology services ranged from $23 in Louisiana to $218 in Wyoming.

Pathologists Also Top Out-of-Network Biller in Yale University Study

A Yale University study into surprise billing released in December and published in the journal Health Affairs found similar results, Modern Healthcare reported. This study examined surprise out-of-network bills incurred by patients who sought care at in-network hospitals for four types of specialists that are not chosen by patients:

pathologists,

anesthesiologists,

radiologists, and

assistant surgeons.

Zack Cooper, PhD (above), is an associate professor of public health at the Yale School of Public Health and one of the study’s authors. He noted in Yale News, “When physicians whom patients do not choose and cannot avoid bill out of network, it exposes people to unexpected and expensive medical bills and undercuts the functioning of US healthcare markets,” adding, “Moreover, the ability to bill out of network allows specialists to negotiate inflated in-network rates, which are passed on to consumers in the form of higher insurance premiums.” (Photo copyright: Yale School of Public Health.)

For the Yale study, the researchers examined employer-sponsored insurance claims from a major commercial insurer for healthcare visits that occurred at in-network hospitals in 2015. They found that 12.3% of cases involving a pathologist were billed out-of-network, which was the highest percentage of the four specialties analyzed. By contrast, 11.8% of anesthesiologists, 11.3% of assistant surgeons, and 5.6% of radiologists billed out-of-network for their services.

The Yale study also found that “the ability of these four specialties to send patients out-of-network bills allowed them to negotiate high in-network payments from insurers, which leads to higher insurance premiums for individuals.”

The Yale study researchers determined that were these specialists unable to bill out-of-network, the particular healthcare plan would save 3.4% of their expenditures or about $40 billion per year, Modern Healthcare reported.

Surprise bills for out-of-network services burden both patients and providers. Insurers want beneficiaries to have access to hospitals and services, but providers in many specialties do not want to contract with those insurers due to low reimbursements.

This disconnect results in providers staying out-of-network and patients receiving surprise bills for out-of-network services even though the hospital was in-network. And pathologists are at the top of the list.

Anatomic pathologists across the country will want to track how government and private payers respond to these findings by amending coverage and reimbursement guidelines in ways that may be unfavorable to the pathology profession.

In another example of giving consumers more direct access to medical laboratory tests, Walmart believes that convenience and lower prices can help it capture market share

Retail giants continue to add healthcare services—including medical laboratory testing—to their wares. It’s a trend that pressures hospital systems, clinical laboratories, pathology groups, and primary care providers to compete for customers. And, while in most instances competition is good, many local and rural healthcare providers cannot reduce their costs enough to be competitive and stay in business.

This is true at Walmart (NYSE:WMT), which recently opened its second “Health Center” in Georgia and announced prices for general healthcare services 30% to 50% below what medical providers typically charge, reported Modern Healthcare.

The services offered at the new Walmart Health Center in Calhoun, a suburb of Atlanta, include:

Primary care

Dental

Counseling

Clinical laboratory testing

X-rays

Health screening

Optometry

Hearing

Fitness and nutrition

Health insurance education and enrollment

A Walmart news release states, “This state-of-the-art facility provides quality, affordable and accessible healthcare for members of the Calhoun community so they can get the right care at the right time … in one facility at affordable, transparent pricing regardless of a patient’s insurance status.”

The fact that Walmart posts “Labs” on the Health Center’s outdoor sign may indicate the retail giant considers easy access to clinical laboratory testing a selling point that will draw customers.

“By offering clinical laboratory testing in support of primary care and urgent care, Walmart may be able to lower prices for lab tests in any market that it enters,” said Robert Michel, Editor-in-Chief of Dark Daily and its sister publication The Dark Report, and President of The Dark Intelligence Group.

The sign above on the exterior of Walmart Health Centers lists the services offered. By advertising “Labs” Walmart is confirming that growing numbers of consumers want to order their own lab tests and that the availability of lab tests gives its medical clinic a competitive advantage. (Photo copyright: Modern Healthcare.)

Healthcare Transparency and Lower Prices

The 1,500 square-foot free-standing Walmart Health Centers offer more services than the in-store Care Clinics installed in other Walmarts throughout Georgia, South Carolina, and Texas. For its healthcare services, Walmart established partnerships with “on-the-ground” health providers to offer affordable services.

“We have taken advantage of every lever that we can to bring the price of doing all of this down more than any hospital or group practice could humanly do. Our goal, just like in the stores, is to get the prices as low as we can,” Sean Slovenski, Senior Vice President and President of Walmart Health and Wellness, told Bloomberg Businessweek.

Some of the clinical laboratory prices prominently posted in the building and noted on the Health Center online price list include:

Meanwhile, the average cost to visit a primary care doctor is $106, according to Health Care Cost Institute data cited by Business Insider, which noted that Walmart’s rates “could be a steep mountain for traditional providers to climb.”

However, Rob Schreiner, Executive Vice President of WellStar Health System in Northern Georgia told Modern Healthcare that “Walmart will offer a cheaper alternative for working-class families who may not have health insurance and may not have an established relationship with a primary care provider.”

Convenient Access to Quality Healthcare Services a Major Draw

At a freestanding Walmart Health Center, people can park near the entrance and walk a few steps to the entrance, rather than traversing aisles to a Care Clinic inside a Walmart Supercenter. And for many customers, finding a Walmart Health Center may not be as complicated or stressful as visiting doctors’ offices.

That seems to be Walmart’s goal—not simply using the Health Centers to increase traffic in its stores, Slovenski said. “We are trying to solve problems for our customers. We already have the volume,” he told Forbes. “We have the locations and the right people. We are creating a supercenter for basic healthcare services.”

Walmart’s arrangement with local healthcare providers differs from traditional primary care clinics staffed by doctors who are practice owners, or who are employed by nearby hospitals and health systems.

“The whole design of the clinic is curious to most of the doctors here [in Dallas, Ga.],” Jeffrey Tharp, MD, Chief Medicine Division Officer, WellStar Medical Group, told Modern Healthcare. “We are advocating integration into our network, for instance with patients who need a cardiologist coming from Walmart to WellStar.”

Clinical laboratory leaders may want to explore partnerships with Walmart and other retailers that are developing healthcare centers to deliver primary care services in places where masses of people shop for everyday items. Especially given that these big-box retailers remain open during healthcare crises like the COVID-19 pandemic.

When patients use telehealth, how do they choose medical laboratories for lab test orders their virtual doctors have authorized?

Doctors On Demand is expanding the nation’s primary care services by launching a virtual care telehealth platform for health insurers and employers. This fits into a growing nationwide trend toward increased use of remote and virtual doctor’s visits. But how should clinical laboratories and anatomic pathology groups prepare for fulfilling virtual doctors’ lab test orders in ways consistent with current scope-of-practice laws?

The rise of virtual care is made possible by innovations in digital

and telecommunication technology. Driven by studies showing more patients are

opting out of conventional primary care visits that take too much time or are

too far away, the healthcare industry is responding by bringing medical

services—including pathology and clinical laboratory—closer to patients through

retail settings and urgent care clinics.

Many pathologists and clinical laboratory managers are unaware of how swiftly patients are becoming comfortable with getting their primary care needs met by other types of caregivers, including virtually. Recently, the Health Care Cost Institute (HCCI) published data showing that visits to primary care physicians declined 18% from 2012 to 2016 among adults under 65 who had employer-sponsored insurance. However, during these same years, visits with nurse practitioners and physician’s assistants increased by 129%!

Another way that providers are making it easier for patients to access healthcare is through the Internet.

Doctor On Demand, a San Francisco-based virtual care provider, is targeting insurers and employers with its Synapse telehealth platform, which integrates into existing health plan networks and enables virtual primary care, according to a news release.

“Through our fully integrated technology platform, we’re putting the patient first and introducing continuity of care not previously available through virtual care solutions,” said Hill Ferguson, CEO of Doctor On Demand in a statement announcing the launch of Synapse on the Humana (NYSE:HUM) health plan network. (Photo copyright: The Business Journals.)

How Synapse Works

Humana is using Synapse in its new On Hand virtual primary

care plan, the news release states. Humana said its members have no copay for

the virtual doctor visits and $5 copays for standard medical laboratory tests

and prescriptions. Synapse’s “smart referrals” function sends referrals to

in-network clinical laboratories, imaging providers, and pharmacies, Healthcare

Dive reported.

“Humana has a deep footprint, and this is a payer looking to create a virtual primary care network as a way to contain cost and thinking about how care is coordinated and delivered,” Josh Berlin, a Principal and Healthcare Co-Practice Leader with advisory firm Citrin Cooperman, told FierceHealthcare.

Changing Primary Care Relationships

Another insurer advancing telehealth is Oscar Health, which offers its own Doctor on Call telehealth platform. The New York City-based health plan reported in a year-end review that 82% of its members had set up a profile that gave them access to a concierge care team and 24/7 telemedicine services, including clinical laboratory test results.

During 2018, Oscar’s concierge teams addressed 1.2 million

questions from 77% of its members, the insurer said.

The graphic above, taken from research conducted by the Health Care Cost Institute (HCCI), shows that while virtual primary care has been expanding, conventional visits to primary care physicians fell 18% from 2012 to 2016 among adults under 65 who had employer-sponsored insurance. Simultaneously, visits with nurse practitioners and physician’s assistants increased by 129%! This indicates a shift in how patients view access to primary care physicians and may explain why telehealth is becoming an attractive option. How will clinical laboratories fit into this new healthcare paradigm? (Photo copyright: HCCI.)

Becker’s Hospital Review reports that telehealth usage by Oscar’s members is five times higher than the average for the healthcare industry.

Will Clinical Laboratories Receive Virtual Referrals?

In a way, it has never been easier for patients to see a

primary care doctor or research symptoms. Additionally, the Internet makes it

possible for patients to self-diagnose, though not always to the benefit of

healthcare providers or the patients.

So, how should clinical laboratories respond to this growing expansion of virtual care doctors? Experts advise lab leaders to reach out to health plans soon and determine their inclusion in virtual healthcare networks. Labs also may benefit by making test scheduling and reporting accessible and convenient to insurance company members and consumers choosing telehealth.

During his keynote presentation at the 24th Annual Executive War College in May, Ted Schwab, a Los Angeles area Healthcare Strategist and Entrepreneur, said, “If you use Google in the United States to check symptoms, you’ll find 350 different electronic applications that will give you medical advice—meaning you’ll get a diagnosis over the Internet. These applications are winding their way somewhere through the regulatory process. (See Schwab’s expanded comments on this trend in, “Strategist Explains Key Trends in Healthcare’s Transformation,” The Dark Report, October 14, 2019.)

Schwab advises that in this “time of change” it’s critical

for labs to take proactive measures. “What we know today is that

providers—including clinical laboratories and pathology groups—who do nothing

will get trampled. However, those providers that do something proactively will

most likely be the winners as healthcare continues to transform.”

Journalists, researchers, and a growing number of consumers now recognize the often huge variability in the prices different medical laboratories charge for the same lab tests

One step at a time, the Medicare program, private health insurers, and employers are putting policies in place that require providers—including clinical laboratories and pathology groups—to allow patients and consumers to see the prices they charge for their medical services. Recent studies into test price transparency in hospitals and health networks have garnered the attention of journalists, researchers, and patients. These groups are now aware of enormous variations in pricing among providers within the same regions and even within health networks.

Now that hospitals’ medical laboratory test prices are

required to be easily accessible to patients, researchers are beginning to compile

test prices across different hospitals and in different states to document and

publicize the wide variation in what different hospital labs charge for the

same medical laboratory tests.

Journalists are jumping on the price transparency bandwagon

too. That’s because readers show strong interest in stories that cover the

extreme range of low to high prices providers will charge for the same lab

test. This news coverage provides patients with a bit more clarity than

hospitals and other providers might prefer.

Shocking Variations in Price of Healthcare

Services, including Medical Laboratory Tests

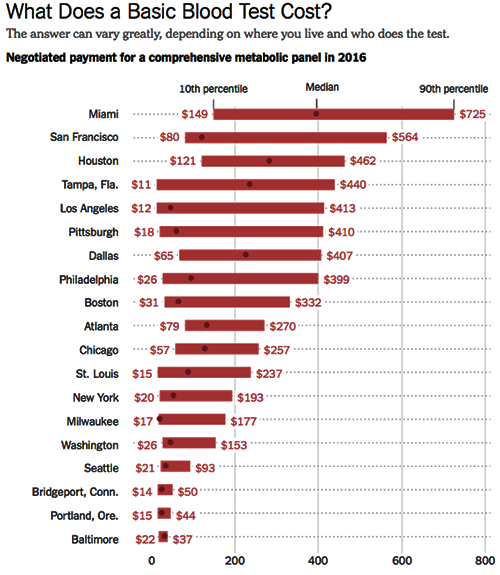

The Health Care Cost Institute (HCCI) in conjunction with the Robert Wood Johnson Foundation (RWJF), examines price levels of various procedures and medical laboratory tests at healthcare institutions across the United States in the first release of a series called Healthy Marketplace Index. According to the HCCI website, “a common blood test in Beaumont, Texas ($443) costs nearly 25 times more than the same test in Toledo, Ohio ($18).”

In April, the New

York Times (NYT) made the wide variation

in how clinical laboratories price their tests the subject of an article titled,

“They Want It to Be Secret: How a Common Blood Test Can Cost $11 or Almost

$1,000.” The article discusses the HCCI findings.

The coverage by these two well-known entities is increasing the

public’s awareness of the broad variations in pricing at clinical laboratories

around the country.

Aside from the large differences in medical laboratory test

prices in different regions, the HCCI found that there are sometimes huge price

variations within a single metro area for the same lab tests. “In just one

market—Tampa, Fla.—the most expensive blood test costs 40 times as much as the

least expensive one,” the NYT notes.

In other industries, those kinds of price discrepancies are

not common. The NYT made a comparatively outrageous example using

ketchup, saying, “A bottle of Heinz ketchup in the most expensive store in a

given market could cost six times as much as it would in the least expensive

store,” adding, however, that most bottles of ketchup tend to cost about the

same.

The graphic above is taken from the New York Times article on test price discrepancies in healthcare. The range of prices for the medical lab test known as a comprehensive metabolic panel are for metropolitan areas only. The data is sourced from the Health Care Cost Institute study. It’s easy to see why patients would be confused by clinical laboratory pricing that varies so widely. (Graphic copyright. The New York Times.)

The CMS mandate designed to make the prices of medical services accessible to healthcare consumers has, in many ways, made things more confusing. For example, most hospitals simply made their chargemaster available to consumers. Chargemasters can be confusing, even to industry professionals, and are filled with codes that make no sense to the average consumer and patient.

“This policy is a tiny step forward but falls far short of what’s needed. The posted prices are fanciful, inflated, difficult to decode and inconsistent, so it’s hard to see how an average person would find them useful,” Jeanne Pinder, Founder and Chief Executive of Clear Health Costs, a consumer health research organization, told the NYT in an article on how hospitals are complying with the mandate to publish prices.

In addition to the pricing information being difficult for

consumers to parse, it also may lead them to believe they would need to pay

much more for a given procedure than they would actually be billed, resulting

in patients opting to not get care they actually need.

Why Having a Strategy Is Critically

Important for Clinical Laboratories

Clinical laboratories are in a particularly precarious position in all of this pricing confusion. For one thing, most hospital-based medical laboratories don’t have a way to communicate directly with consumers, so they don’t have a way to explain their pricing. Additionally, articles and studies such as those in the NYT and from the HCCI, which describe drastic price variations for the same tests, tend to cast clinical laboratories in a somewhat sinister light.

To prepare for this, medical laboratory personnel should be

trained in how to address customer requests for pricing and how to explain

variations in test prices among labs, before such requests become problematic. Lab

staff should be able to explain how patients can find out the cost of a given

test, and what choices they have regarding specific tests.

In 2016, Dark Daily’s sister-publication, The Dark Report (TDR), dedicated an entire issue to the impact of reference pricing on the clinical laboratory industry. In that issue, TDR reported on how American supermarket chain Safeway helped guide their employees to lower-priced clinical laboratories for lab tests, resulting in $2.7 million savings for the company in just 24 months. Safeway simply implemented reference pricing; the company analyzed lab test prices of 285 tests for all of the labs in its network, and then set the maximum amount it would pay for any given test at the 60th percentile.

If a Safeway employee selected a medical laboratory with prices less than the 60th percentile, the normal benefits and co-pays applied. But if a Safeway employee went to clinical laboratories that charged more than the 60th percentile level, they were required to pay both their deductible and the amount above Safeway’s maximum.

Safeway’s strategy revealed wide variation in testing

prices, just as the HCCI report found. This means that employers can be added

to the list of those who are paying much closer attention to medical laboratory

test pricing than they have in the past. These are developments that should

motivate forward-looking pathologists and clinical laboratory executives to act

sooner rather than later to craft an effective strategy for responding to consumer

and patient requests for lab test price transparency.

Clinical laboratories that service both settings could be impacted as new CMS proposed rule attempts to align Medicare’s payment policies for outpatient and in-patient settings

Hospital outpatient revenue is catching up to inpatient

revenue, according to data released from the American

Hospital Association (AHA). This increase is part of a growing trend to

reduce healthcare costs by treating patients outside of hospital settings. It’s

a trend that is supported by the White House and Medicare and continues to

impact clinical

laboratories, which serve both hospital inpatient and outpatient customers.

The AHA published this study data in its annual Hospital Statistics, 2019Edition. The data comes from a 2017 survey of 5,262

US hospitals. The report includes data about utilization, revenue, expenses,

and other indicators for 2017, as well as historical data.

The AHA statistics on outpatient revenue suggest providers

nationwide are working to keep people out of more expensive hospital settings. Hospitals,

like medical

laboratories, appear to be succeeding at developing outpatient and outreach

services that generate needed operating revenue.

This aligns with Medicare’s push to make healthcare more accessible through outpatient settings, such as urgent care clinics and physician’s offices. A growing trend Dark Daily has covered extensively.

Outpatient Revenue

Climbs

In its coverage of

the AHA’s study, Modern Healthcare reported that 2017

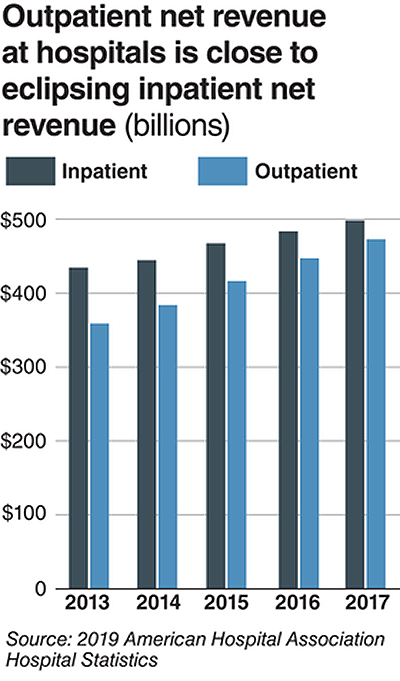

hospital net inpatient revenue was $498 billion and net outpatient revenue was

$472 billion.

The Becker’s Hospital CFO Report notes that

gross inpatient revenue in 2017 was $92.7 billion higher than gross outpatient

revenue. But in 2016, gross inpatient revenue was much further ahead—$129.5

billion more than gross outpatient revenue. The “divide” between inpatient and

outpatient revenue is narrowing, Becker’s reports.

The graphic above illustrates the shrinking gap between hospital inpatient and outpatient revenues. “Outpatient revenue will ultimately eclipse inpatient revenue,” Chuck Alsdurf, Director of Healthcare Finance Policy and Operational Initiatives at the Healthcare Financial Management Association (HFMA), told Modern Healthcare. (Graphic copyright: Modern Healthcare/AHA.)

The Becker’s

report also stated:

Admissions increased by less than 1% to 34.3

million in 2017, up from 34 million in 2016;

Inpatient days were flat at 186.2 million;

Outpatient visits rose by 1.2% to 766 million in

2017; and,

Outpatient revenue increased 5.7% between 2016

and 2017.

Similar Study Offers Additional

Insight into 2018 Outpatient Revenue

A benchmarking report by Crowe,

a public accounting, consulting, and technology firm, which analyzed data from

622 hospitals for the period January through September of 2017 and 2018, showed

the following, as reported by RevCycleIntelligence:

Inpatient volume was up 0.6% in 2018 and gross

revenue per case grew by 5.3%;

Outpatient services rose 2.4% in 2018 and gross

revenue per case was up 7.1%.

Physicians’ Offices

Have Lower Prices for Some Hospital Outpatient Services

Everything, however, is relative. When certain healthcare

services traditionally rendered in physician’s offices are rendered, instead,

in hospital outpatient settings, the numbers tell a different story.

In fact, according to the Health

Care Cost Institute (HCCI), the price for services was “always higher” when

performed in an outpatient setting, as compared to doctor’s offices.

HCCI analyzed services at outpatient facilities as well as

those appropriate to freestanding physician offices. They found the following

differences in 2017 prices:

Diagnostic and screening ultrasound: $241 in

physician’s office—$650 in hospital outpatient setting;

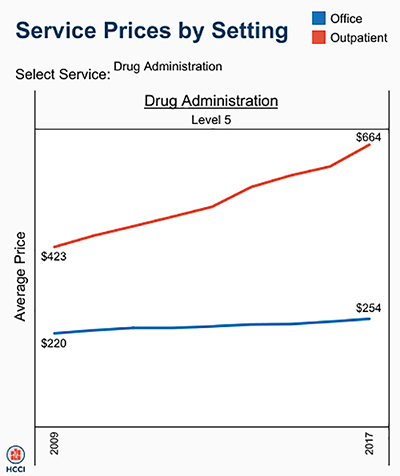

Level 5 drug administration: $254 in office—$664

in hospital outpatient setting;

Upper airway endoscopy: $527 in office—$2,679 in

hospital outpatient setting.

One example where hospital outpatient settings provide similar services at increased costs is in drug administration, as the graphic above illustrates. “The difference was higher than I expected. With some services, the price is two or three times higher when rendered in the outpatient setting,” Julie Reiff, HCCI researcher and report author, told Fierce Healthcare. (Graphic copyright: HCCI.)

Medicare Proposed

Rule Would Change How Hospital Outpatient Clinics Get Paid

Meanwhile, the Centers for

Medicare and Medicaid Services (CMS) has released its final rule (CMS-1695-FC),

which make changes to Medicare’s hospital outpatient prospective payment and

ambulatory surgical center payment systems and quality reporting programs.

In a news

release, CMS stated that it “is moving toward site neutral payments for

clinic visits (which are essentially check-ups with a clinician). Clinic visits

are the most common service billed under the OPPS [Medicare’s Hospital

Outpatient Prospective Payment System). Currently, CMS often pays more for

the same type of clinic visit in the hospital outpatient setting than in the

physician office setting.”

“CMS is also proposing to close a potential loophole through

which providers are billing patients more for visits in hospital outpatient

departments when they create new service lines,” the news release states.

Hospitals are fighting the policy change through a lawsuit, Fierce Healthcare reported.

In summary, clinical laboratories based in hospitals and

health systems are in the outpatient as well as inpatient business. Medical laboratory

tests contribute to growth in outpatient revenue, and physician offices compete

with clinical laboratories for some outpatient tests and procedures. Thus, a new

site-neutral CMS payment policy could affect the payments hospitals receive for

clinic visits by Medicare patients.